Zero-Price Power: What SMP at 0 Won Means for Every Generator in Korea

Korea's wholesale electricity price hit zero — and the system stayed stable, but only with growing operator intervention. Here's why that matters, and why it won't stay comfortable for long.

DEEP DIVE

The Zero That Wasn’t Supposed to Happen

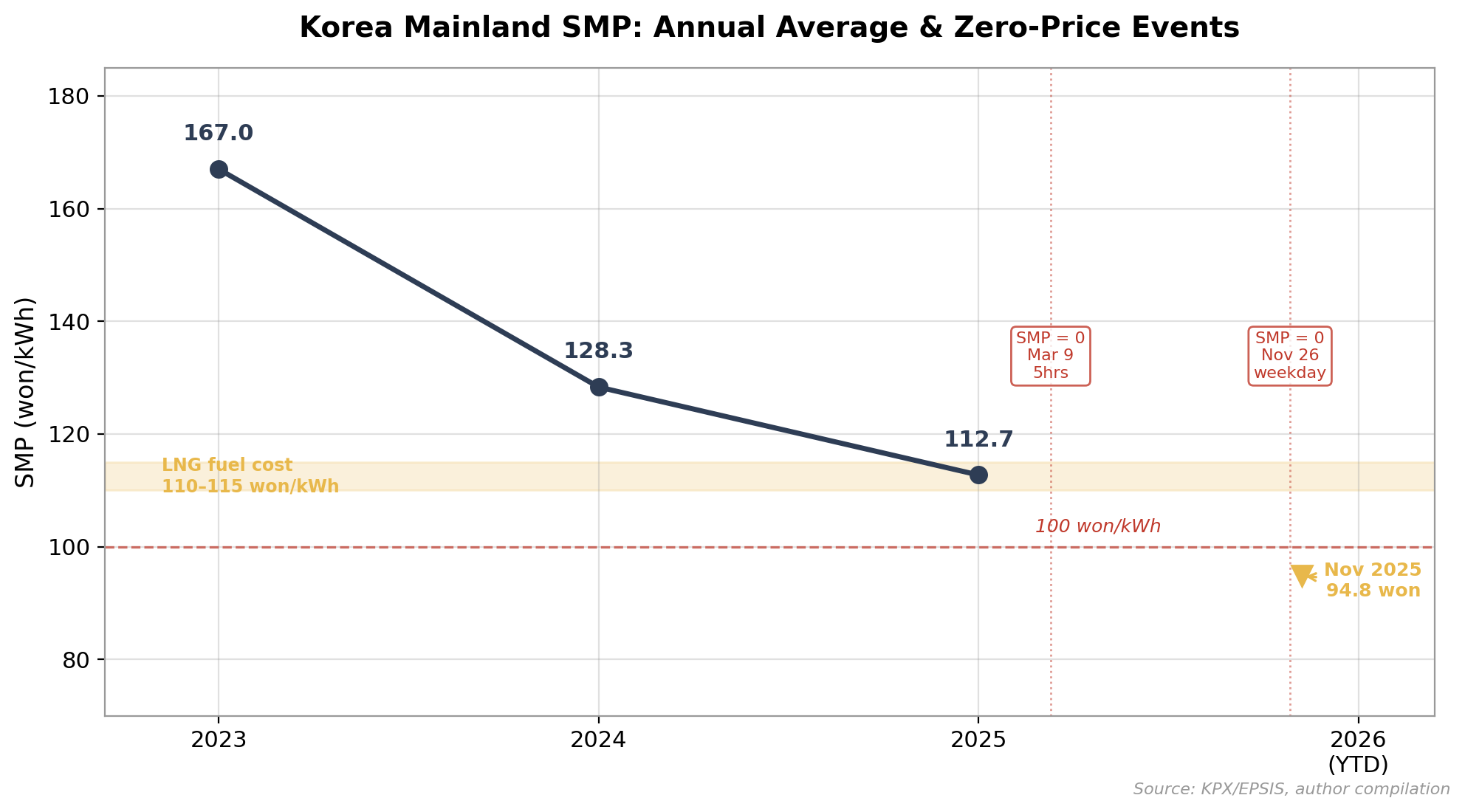

On March 9, 2025, Korea’s System Marginal Price (SMP) dropped to 0 won/kWh at 11:00 and stayed there for five consecutive hours. SMP is the single clearing price of Korea’s cost-based wholesale pool — one number that determines revenue for every generator on the grid. It was a Sunday in early spring, not a holiday. Demand sat around 42–43 GW. Solar PV output reached roughly 20 GW, covering 35.4% of total generation at its 13:00 peak (Electimes).

That alone would have been notable. But the trend did not stop at weekends. By November 26, 2025 — a Wednesday — SMP hit zero again during the midday hour. Demand that day was 61,199 MW, well above any seasonal trough. The cause was not low demand alone. Baseload nuclear output, solar PV peaking through the lunch hours, and CHP plants locked into district heating obligations all pushed generation above what the market could absorb. The CHP piece is Korea-specific: the regulatory framework treats heat-supply commitments as must-run obligations, a structure rarely seen elsewhere (Digital News). Grid constraints and self-scheduling commitments kept other units online as well, forming a compound floor under generation output even as the price signal said “stop.”

I count at least 26 confirmed mainland zero-price hours between January 2025 and mid-March 2026 — all during daytime — based on official daily minima and time-stamped reports (EPSIS, Electimes, KPX notices). The actual total is likely higher. Twenty-six hours across fifteen months is not, by itself, a crisis. In my decade of valuing combined-cycle gas plants at SK E&S, SMP at zero was never a scenario we modeled. The question now is not what happened — but how fast this number grows. This is not a story about one strange pricing event. It is a repricing event for every generation asset in Korea.

A Floor, Not a Pit

International readers will hear “zero price” and think of Germany or Spain — markets where wholesale prices go negative. In 2025 alone, Germany’s day-ahead market recorded 573 hours of negative pricing (Bundesnetzagentur). Spain logged 527 zero-price hours and another 196 hours below zero in 2024.

Korea’s wholesale market operates under a different architecture. The cost-based pool (CBP) does not allow generators to submit strategic bids. Under the power market operating rules, SMP is set as the highest effective price among price-setting eligible generators. When no eligible unit carries a positive effective price, mainland SMP bottoms at 0 won/kWh. In practice, this happens when zero-variable-cost sources — nuclear, solar, wind — are the only units needed to meet demand. There is no negative-pricing mechanism on the mainland. Jeju Island operates as a separate electricity market with its own SMP; it runs a renewable auction pilot that permits sub-zero bids, but the mainland pool has a hard floor at zero (Power Market Operating Rules).

The same structural pressure that produces negative prices in Europe — renewable output exceeding demand during off-peak hours — manifests differently in Korea. Instead of prices falling to –50 or –100 EUR/MWh, the pressure compresses into prolonged zero-price windows. The relevant metric for Korea is not the depth of the price drop but the duration at zero.

Why This Is Structural

Two forces are converging, and neither is cyclical.

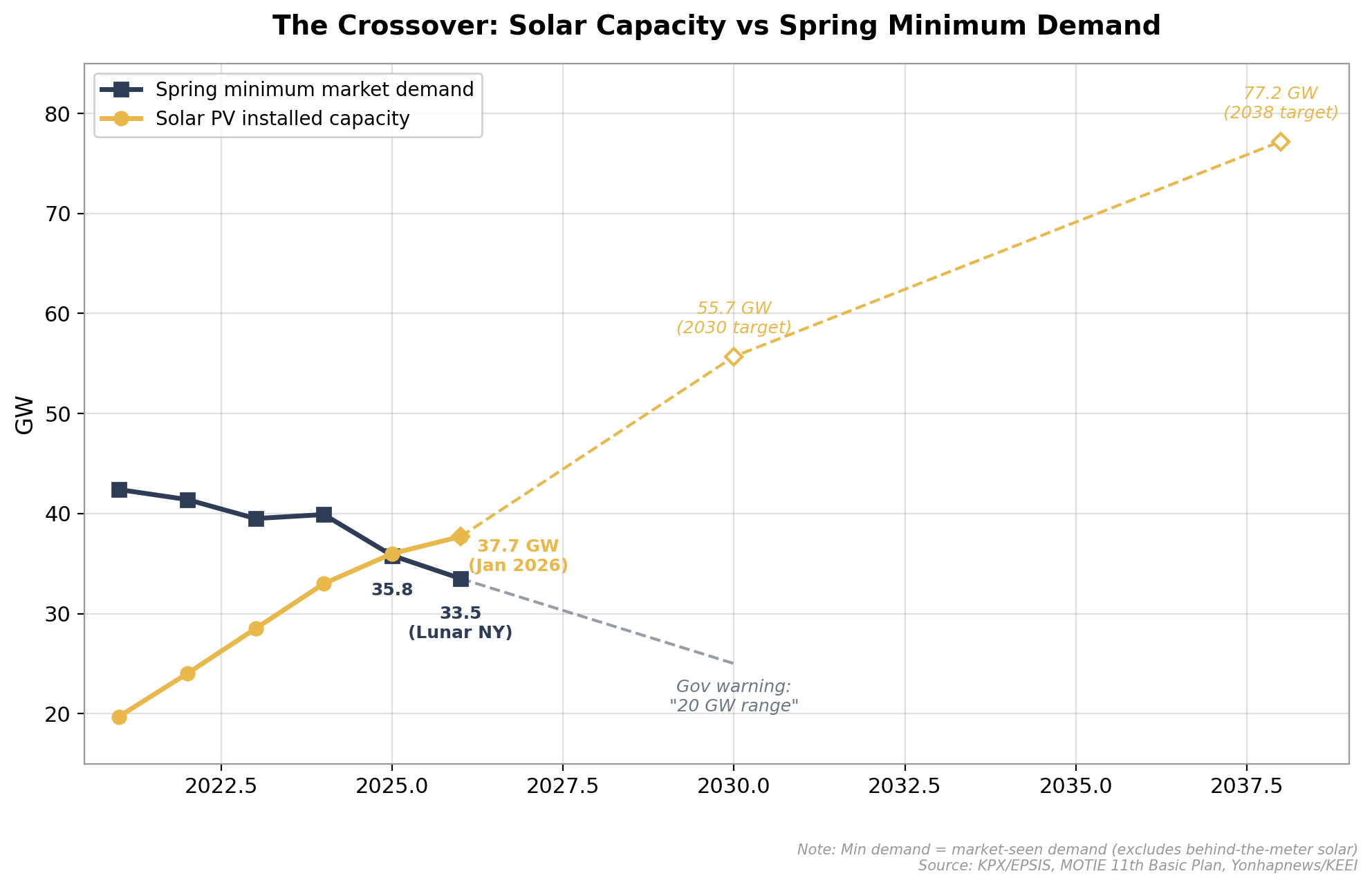

The numerator is growing. The 11th Basic Plan for Electricity Supply and Demand (제11차 전력수급기본계획), confirmed in February 2025, targets solar PV capacity at 55.7 GW by 2030 and 77.2 GW by 2038, with wind rising from 3 GW to 18.3 GW and then 40.7 GW over the same horizon. As of January 2026, installed solar PV already stood at 37.7 GW — meaning another 18 GW arrives by 2030 and a further 39 GW by 2038 (MOTIE). Each gigawatt added pushes midday generation closer to the point where no thermal plant is needed to balance supply.

Market-seen demand — the denominator — is shrinking. Korea’s minimum market demand during spring — the season when heating loads vanish and air conditioning has not started — has fallen from 42.4 GW in 2021 to 35.8 GW in 2025. During the Lunar New Year holiday in January 2026, it touched 33.5 GW. The government has warned that spring troughs could fall into the 20-GW range within several years (Yonhap News; cited in Korea Energy Economics Institute). The primary cause is behind-the-meter solar PV on distribution networks displacing what the market sees as demand. Actual electricity consumption has not declined proportionally — the generation is happening, but it is invisible to the wholesale market.

And that invisibility itself is a problem. Of Korea’s 37.7 GW of installed solar, Korea Power Exchange (KPX) directly meters only 11.1 GW — 29% of the total. Another 13.2 GW is tracked through KEPCO’s distribution metering. The remaining 13.4 GW — more than a third — sits behind the meter in small-scale and self-consumption installations where real-time visibility is limited (Korea Policy Briefing). When a third of the supply pushing prices to zero is not directly measured by the system operator, modeling the trajectory becomes an exercise in informed estimation, not precision.

The early warning signals are already visible. Jeju Island recorded 56 days of renewable curtailment in 2024 (KPX). On the mainland, KPX issued curtailment forecasts in February and April 2025 — events that were rare even two years ago. Annual average SMP has fallen from 167.0 won/kWh in 2023 to 128.3 in 2024 to 112.7 in 2025, with the November 2025 monthly average dropping to 94.8 won (KPX). Part of this decline reflects lower global LNG prices — and a Hormuz-related price spike could reverse the fuel-cost component (see Issue #1, Issue #2). But the structural floor created by renewable expansion does not reverse with fuel prices. Even if LNG costs double, spring afternoons will still produce zero-price hours.

What SMP at Zero Changes

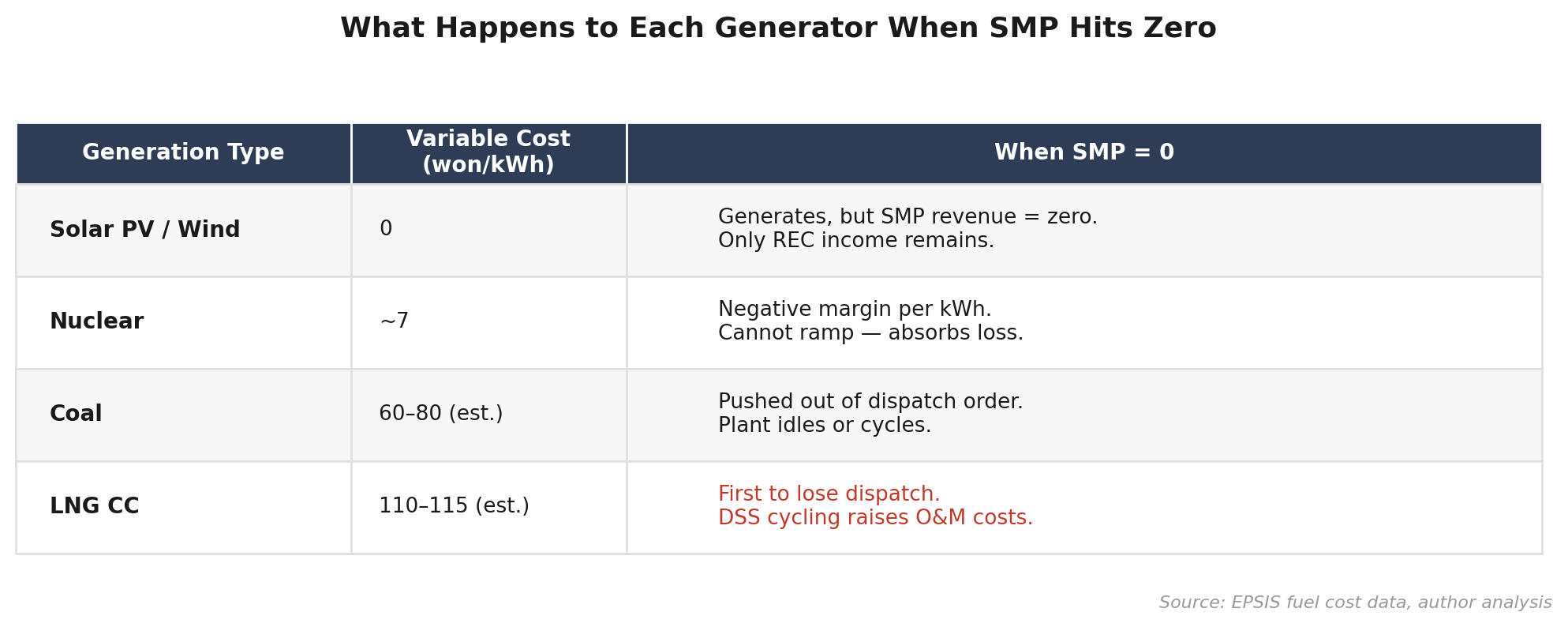

Every generator’s financial model needs a new variable. Zero-price hours were not part of standard project economics in Korea. They are now. For solar and wind operators, SMP revenue vanishes during the hours they generate most. The Renewable Energy Certificate (REC) spot market — trading around 70,000–72,000 won per certificate — provides a buffer, but the combined SMP-plus-REC revenue has already fallen from roughly 240 won/kWh in 2023 to the mid-180s in 2025 (KPX, NUMIT). For offshore wind projects carrying investment costs several times higher than onshore solar, the erosion of SMP-based revenue undermines the financing assumptions at the core of their project economics. As projects such as Nakwol (364 MW) move into partial operation and others like Anma (532 MW) advance toward commissioning, zero-price risk could begin to extend beyond pure solar hours into evening and nighttime, because coastal winds peak in winter and spring regardless of the sun.

Nuclear plants face a different problem. With variable costs around 7 won/kWh, a zero SMP means negative margins on every unit of output. Reactors cannot start and stop daily — ramping a pressurized water reactor takes days, not hours. During zero-price windows, nuclear units likely continued operating under self-scheduling or grid-constraint designations, absorbing the loss. For coal and LNG, the impact is sharpest. LNG fuel cost alone — estimated at 110–115 won/kWh on the EPSIS reference basis, which is believed to exclude generators on direct-import or KOGAS individual-rate contracts — already exceeds the prevailing SMP in many hours. LNG combined-cycle plants are being pushed out of the dispatch order during daytime. If zero-price hours become structural, daily start-stop (DSS) cycling becomes the default operating pattern, accelerating hot-section fatigue, shortening maintenance intervals, and raising operating costs.

The path into the Korean market is narrowing — for every fuel type.

For renewables, sustained zero-price SMP undermines the returns that justify new investment, particularly for capital-intensive offshore wind. The looming transition from the current RPS system to a government-run long-term fixed-price auction adds regulatory uncertainty on top of market uncertainty.

Nuclear investment continues as national strategic policy, but plant-level economics and operational burden are growing. Reactors that cannot flex face widening periods of below-cost dispatch — a drag on returns that compounds over a 60-year asset life.

For gas, the door is nearly shut. MOTIE treats new standalone LNG combined-cycle plants as stranded-asset risks; generation business permits are effectively unavailable.

The only remaining entry route for gas-fired generation is CHP — and even that path is constrained. The 11th Basic Plan caps new CHP capacity at 2.2 GW through 2032, separate from coal-replacement conversions that proceed under the existing CP mechanism through joint ventures with generation subsidiaries. At roughly 500 MW per Korean-scale CHP unit, 2.2 GW means about four plants. The 2024 pilot auction already absorbed 0.9 GW, leaving room for two to three more units at most. Industry estimates suggest winning bids came in at least 15% below the RCP — compressing margins before the first shovel breaks ground. New CHP entrants face a triple squeeze: they must demonstrate heat demand under the District Energy Act , compete in a capacity auction at discounted rates, and operate into a wholesale market where SMP may be zero during their peak generation hours.

KEPCO sits on the other side of this equation. When SMP was surging in 2022, Korea Electric Power Corporation (KEPCO) absorbed the gap between soaring wholesale costs and politically frozen retail tariffs — accumulating over 43 trillion won in operating losses across 2021–2023 (Issue #2). Now the mechanism runs in reverse. SMP declines reduce KEPCO’s power purchase costs. In 2025, KEPCO reported operating profit of 13.5 trillion won, with private-generator procurement costs falling by 607.2 billion won year-on-year, explicitly attributed to lower SMP (KEPCO earnings release). The average purchase price dropped to 132.4 won/kWh against a selling price of 170.4 won/kWh. The sovereign shock absorber is refilling — at the generators’ expense.

One structural shift cuts the other way: corporate PPAs become viable. As SMP falls, the contract price at which a power purchase agreement beats KEPCO’s industrial tariff drops with it. For generators, a fixed-price PPA replaces volatile spot revenue — including zero-price hours — with predictable cash flow. For corporate buyers, a PPA delivers electricity at or below the regulated tariff while satisfying RE100 commitments. Korea’s PPA market has been slow to develop in part because KEPCO’s subsidized tariffs left little room for competing offers. How small is it? Direct PPA volume in 2024 was 224,200 MWh across just 54 consumption sites — roughly 0.04% of Korea’s total electricity sales that year (KPX, EPSIS). Third-party PPAs, brokered through KEPCO, stood at 12 contracts covering 30 MW as of September 2025 (Korea Open Data Portal). The market barely exists. But the trajectory is steep: direct PPA volume grew 29-fold from 2023 to 2024, and SMP compression is closing the price gap that kept corporates on the regulated tariff. If the trend holds, the economics that make zero-price SMP painful for spot-market generators are the same economics that finally unlock Korea’s bilateral contract market.

And the pressure accelerates market reform. The longer zero-price hours persist, the harder it becomes to manage variable renewables, compensate flexible generators, and protect strategic nuclear assets within a single-price pool. Korea’s policy community is already discussing the separation of the wholesale market into distinct energy, capacity, and ancillary-service segments. SMP at zero does not break the system today. But it exposes a design that was built for a thermal-dominated grid — and the grid is no longer thermal-dominated during the hours that matter most.

Outlook

Base case. Zero-price SMP hours on the Korean mainland will grow from the current ~26-hour floor toward triple digits within two to three years as the Basic Plan’s solar and wind targets materialize and spring minimum demand continues to fall. All generation asset valuations will need to incorporate zero-price scenarios that were previously excluded.

What I’m watching. The quarterly trend in mainland zero-price hours — the pace of acceleration matters more than any single event. The speed of curtailment migration from Jeju to the mainland grid. Whether declining heating demand in shoulder seasons erodes the CHP must-run volume that has so far kept the grid stable during zero-price windows.

What would change my mind. Commissioning of the roughly 4 GW-class pumped-hydro storage now in the planning pipeline under the 10th and 11th Basic Plans. Pumped hydro offers larger capacity and longer duration than battery ESS, though it rarely enters the conversation outside grid-planning circles; if these plants arrive on schedule, they represent the single most effective absorber of midday surplus. Failing that, a large-scale battery ESS deployment mandate on the order of multiple gigawatts. A restructured time-of-use industrial tariff that shifts daytime demand upward. Or a full capacity market that compensates dispatchable generators for availability rather than output. None of these is imminent.

If this analysis is useful for your team’s Asia energy strategy, consider forwarding it to a colleague who tracks power market investments.