Hormuz Won't Shut Down Korea's Factories — But the Price Shock Is Real

4.2% of generation is exposed. KEPCO's balance sheet absorbs the rest.

DEEP DIVE

Samsung and SK Hynix produce over 70% of the world’s DRAM and more than half its NAND flash. Korean shipyards built 28% of global tonnage in 2024, including most of the world’s LNG carriers. Korean defence contractors are now the second-largest arms supplier to NATO member states after the United States. If Korea’s factories shut down, it is not a Korean problem. It is a global supply chain problem.

That is the premise behind a persistent narrative: a Hormuz Strait blockade cuts Korea’s LNG supply, power generation collapses, and manufacturing lines go dark. Korea imported 46.7 million tonnes of LNG in 2025, and Qatar alone supplied 14.9% of it. But each link in that chain breaks under scrutiny. Korea’s power system has multi-GW reserve margins even at summer peak. Nuclear capacity is expanding, not contracting. And a large share of coal generation sits deliberately idle under air quality regulations — available to restart in an emergency. The risk from Hormuz is not a blackout. The risk is a price shock that feeds through every megawatt-hour Korea generates — because LNG sets the wholesale price more than 80% of the time.

What Hormuz Actually Means for Korea’s LNG

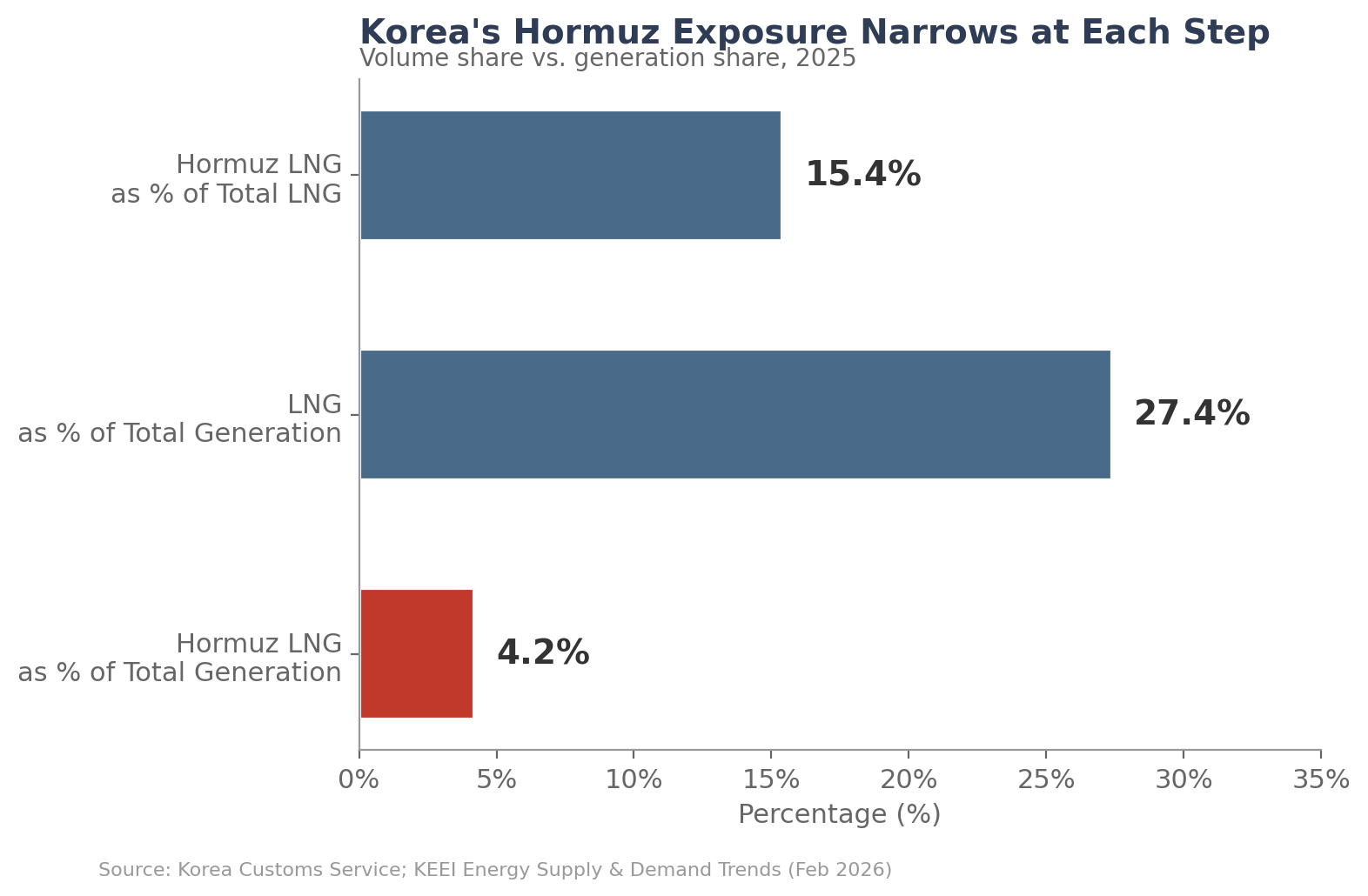

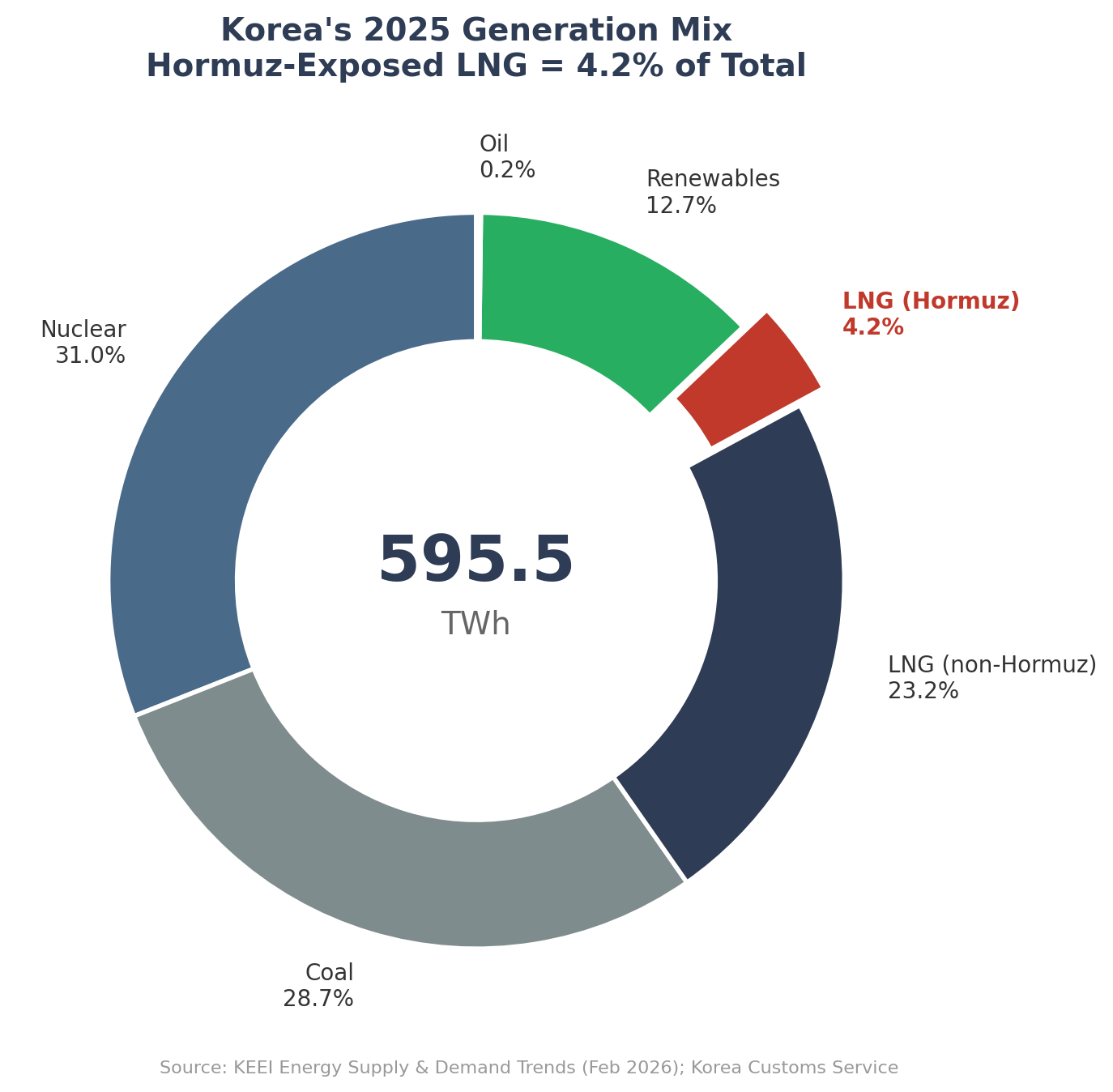

Korea’s 2025 LNG imports totalled 46.7 million tonnes (Korea Customs Service). Of that, 7.2 million tonnes — Qatar and UAE combined — transited the Hormuz Strait. That is 15.4% of Korea’s LNG supply. Not trivial. But the claim that this exposure translates into a generation shortfall requires a second step: converting volume into electricity. LNG accounted for 27.4% of Korea’s 595.5 TWh of generation in 2025 (Korea Energy Economics Institute(KEEI), Energy Supply and Demand Trends, February 2026). Hormuz-exposed LNG’s share of total generation: 4.2%. A full Hormuz blockade — a scenario that did not materialize even during the 1980–88 Iran–Iraq War — would put 4.2% of Korea’s power output at risk. The remaining 95.8% of Korea’s generation does not depend on Hormuz-exposed LNG. It comes from nuclear (31.0%), coal (28.7%), non-Hormuz LNG, renewables (12.7%), and a negligible oil component.

The exposure narrows further when the fuel procurement structure is disaggregated. Korea’s private LNG industry association reported that of 22.9 million tonnes of LNG consumed for power generation in 2025, 67.7% flowed through KOGAS (Korea Gas Corporation) and 32.3% was procured through direct imports (Korea Private LNG Industry Association, 2025 Direct Import Report). KOGAS’s Middle East sourcing share was 24.3%. But direct importers — who supplied 7.4 million tonnes to power plants — sourced only 2.7% from the Middle East. Their supply came from Oceania (41%), Southeast Asia (39%), and North America (11%). Korea’s physical LNG supply base is more diversified than the headline Qatar figure implies. That does not prove which procurement bucket set SMP in each hour — KOGAS-supplied generators, not direct importers, are typically the marginal units. But it does mean the physical supply disruption risk from Hormuz is narrower than the 15.4% figure suggests.

The Shutdown Chain Breaks at Every Link

The “Hormuz blockade → factory shutdown” narrative rests on three sequential assumptions: LNG supply drops, power generation falls short, and the grid cannot meet industrial demand. None of those steps holds up once you look at the system data.

Volume. KPX (Korea Power Exchange) data for March 3–12, 2026 shows the system maintained 9.6 to 18.5 GW of reserve capacity at any given hour — the instantaneous gap between available generation and peak demand. Reserve margins ranged from 12.5% to 29.3% (KPX Daily Supply and Demand Report). Even the tightest day, March 9, carried 9.6 GW of spare capacity. That is six to seven large LNG combined cycle units sitting idle. At summer peak — the system’s most constrained period — the picture holds. Peak demand reached 96.0 GW in summer 2025 with 9.1 GW of reserve (9.4% margin). Peak demand hit 97.1 GW in summer 2024 with 8.2 GW of reserve (8.5%). MOTIE (The Ministry of Trade, Industry and Energy) projected that even under an upper-bound demand scenario of 97.8 GW, the system would hold 8.8 GW of reserve plus 8.7 GW of emergency resources. Korea is not running a knife-edge power system, even at peak.

Baseload reinforcement. Nuclear capacity is growing. Shin Hanul Unit 2 (1.4 GW) entered commercial operation in 2024, increasing Korea’s nuclear fleet to 27.2 GW. Nuclear utilization reached 87% that year (KPX). Saeul Unit 3 (1.4 GW) received its operating license in December 2025 and is scheduled for commercial operation by August 2026. The supply base is expanding — an additional 2.8 GW of nuclear capacity in two years.

Coal buffer (winter and spring). Korea maintains 32.6 GW of public coal generation capacity across 53 units (KPX, Central Dispatch Generator Status, year-end 2024). The Ministry of Environment runs the 7th Fine Dust Seasonal Management Program (제7차 미세먼지 계절관리제) from December through March — the heating season. It caps approximately 15 coal units at 80% output on weekdays and shuts down up to 29 units on weekends. The weekday cap alone suppresses an estimated 1.8 GW of output — roughly 2.6% of recent March peak demand of 71–72 GW. The weekend shutdowns represent a far larger policy-held reserve: up to 17.8 GW of nameplate capacity deliberately kept offline for air quality, not because the grid does not need it. The Ministry’s own March 2026 press guidance states explicitly that coal generation will be operated flexibly if LNG supply disruptions occur. This is not speculative. It is a government-declared contingency measure already in the policy framework.

Structural overcapacity (year-round). The seasonal coal buffer addresses the winter scenario. But the summer scenario has its own answer: by August 2026, Saeul Unit 3 adds 1.4 GW of new nuclear baseload — capacity that arrives precisely in time for summer peak. More broadly, Korea’s power system carries material reserve buffers and faces transition-era surplus risk across parts of the fleet. The 11th Basic Plan for Electricity Supply and Demand (제11차 전력수급기본계획) explicitly addresses the risk of stranded assets among fossil fuel generators as renewable and nuclear capacity expands. Policymakers are managing a transition from overcapacity, not scarcity. That is not what a grid on the edge of blackout looks like.

Stack these layers: 8–9 GW of standing reserve at peak, 2.8 GW of new nuclear entering the fleet, 1.8 GW of immediately recoverable coal output during winter, and a structural generation surplus that has the government planning fossil plant retirements rather than additions. A 4.2% generation exposure to Hormuz does not produce a blackout in this system. It does not come close.

The Real Transmission Channel: Price

Hormuz matters for Korea — not through volume, but through price. And here the exposure is far broader than 15.4%.

The reason is structural: how Asian LNG is priced. The majority of Korea’s long-term LNG supply contracts — both KOGAS procurement and direct imports — use an oil-indexed pricing formula. The delivered price of each LNG cargo is calculated as a slope coefficient multiplied by a crude oil benchmark (typically JCC, the Japan Crude Cocktail, or Brent), plus a constant. The slope typically falls between 10% and 15% of the oil price, with a time lag of three to six months between the oil price movement and the LNG delivery price adjustment. This is not unique to Korea — it is the standard pricing structure for long-term LNG contracts across Asia. Spot cargoes may price differently, but term volumes — which make up the bulk of Korea’s supply — are exposed to oil price movements.

The implication is direct. When a Hormuz crisis pushes crude oil above $100/barrel, the price increase feeds through to the majority of LNG Korea imports — regardless of where it was loaded. Australian LNG from Gladstone, US LNG from Sabine Pass, Malaysian LNG from Bintulu — term contracts reprice upward through the same oil-linked formula. The physical volume at risk is 15.4%. The price impact is system-wide.

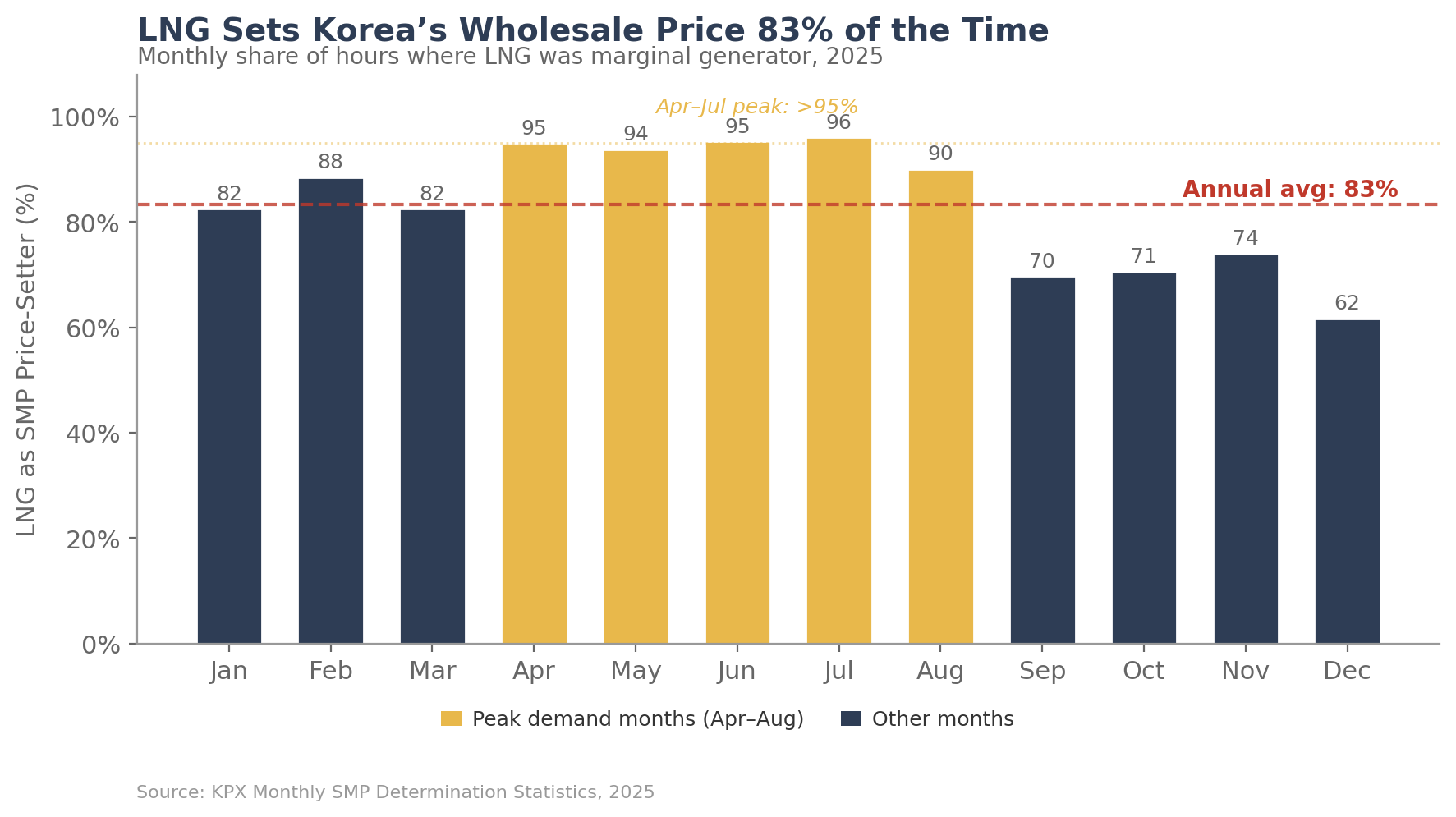

That repriced LNG cost transmits directly into Korea’s wholesale electricity price. Korea operates CBP (cost-based pool) where generators bid their variable costs and the marginal unit sets the SMP (System Marginal Price) for all dispatched generators in each hour. In 2025, LNG-fired generators set the SMP in 83% of all hours (KPX, Monthly SMP Determination Statistics). During April through July — peak demand months — that share exceeded 95%.

When LNG fuel costs rise, SMP rises across the board. The buyer on the other side is KEPCO (Korea Electric Power Corporation) — the sole purchaser in the wholesale pool. KEPCO sells to end users at politically administered tariffs that have been held below cost-recovery levels for years.

The pattern is already materializing. JKM, Asia's spot LNG benchmark, has spiked above $22/MMBtu — more than double the level two weeks ago — after QatarEnergy declared force majeure on exports. As of March 13, the government has announced a 100 trillion won ($68 billion) stabilization fund, while MOTIE is discussing greater coal and nuclear utilization alongside tariff-stabilization measures (Yonhap, Reuters). The policy response points in the same direction: the government’s priority is shielding industrial consumers from the price shock, not preventing a blackout that was never going to happen.

What to Watch

Brent crude. If prices sustain above $90/barrel for two or more quarters, expect KOGAS to revise its quarterly gas supply tariff upward. The lag between oil price movements and LNG contract repricing is typically three to six months.

KEPCO quarterly results. KEPCO’s Q2 and Q3 earnings will be the first to reflect any oil-driven SMP increase. Watch the gap between wholesale purchase cost and retail tariff revenue.

Coal seasonal management flexibility. If MOTIE exercises the coal restart contingency before the seasonal program ends on March 31, it signals that policymakers view the LNG price situation as severe enough to override air quality commitments.

Base case: Korea’s physical power supply remains secure. The system absorbs even a full Hormuz disruption scenario without load shedding. But the fiscal consequence is real, and the transmission mechanism is uniquely Korean. While textbook market logic dictates that higher wholesale costs (SMP) pass through to industrial consumers, political reality dictates otherwise.

I expect the government will not pass a war-induced LNG price shock onto the factory floors of Samsung, SK, or Hyundai. Policymakers already face intense political burden regarding baseline tariff adjustments planned for the first half of the year. Adding a geopolitical risk premium to industrial power bills to protect KEPCO’s margins is highly unlikely in the current political climate.

Therefore, KEPCO will once again act as the sovereign shock absorber. The cost gap will land squarely on KEPCO’s balance sheet, reviving the exact debt accumulation cycle seen in the 2022 crisis. The immediate threat of a Hormuz blockade is not a blackout. It is not an overnight spike in manufacturing costs for Korea’s exporters. The true vulnerability is the deepening structural deficit of Korea’s state utility, forced to absorb a global price shock with politically frozen retail tariffs.

If this analysis is useful for your team’s Asia energy strategy, consider forwarding it to a colleague evaluating Korea market exposure.