Hormuz Crisis: Korea's Power Bill Is About to Get Worse

Korea is no longer the low-cost manufacturing base many models still assume.

MARKET SIGNAL

QatarEnergy’s force majeure has pulled a major share of global LNG supply offline. The less visible question is what happens to Korea’s electricity tariff structure six months from now.

On March 2, Iran’s Islamic Revolutionary Guard Corps (IRGC) declared the Strait of Hormuz closed to commercial shipping. Nine days in, the Ras Laffan terminal — the world’s largest LNG liquefaction complex — remains shut, and QatarEnergy declared force majeure on March 7. The Japan Korea Marker (JKM), Asia’s LNG spot benchmark, hit $15.71/MMBtu as of March 8 (S&P Global Platts), with the Asia-Atlantic spot spread at its widest since the 2022 European energy crisis. The bottleneck is not production capacity. It is shipping distance and terminal availability.

For Korea, short-term supply is manageable — but at a higher cost. Korea Gas Corporation (KOGAS) holds long-term contract volumes with Qatar, and these cargoes transit the Strait of Hormuz, meaning alternative supply must be sourced. Backup spot procurement from the US and Australia is available but expensive. Korea’s LNG inventories entering spring are adequate — heating demand is falling, and summer cooling load hasn’t started.

The real problem arrives in Q3–Q4 2026.

LNG spot prices in March will not hit Korea’s wholesale electricity market immediately. The landed wholesale price of LNG in Korea reflects the current market with a 4–6 month lag — the time it takes from spot contract execution through shipping, arrival, and unloading before the new price feeds into fuel cost calculations. When it does, the System Marginal Price (SMP), Korea’s wholesale electricity price, will rise. This is not a forecast — it is mechanics. In Korea’s cost-based pool, LNG-fired generation set the marginal price 88.7% of the time as of February 2025 (KPX Monthly SMP Statistics). Higher LNG fuel costs feed directly into higher SMP. The wholesale cost of electricity that Korea Electric Power Corporation (KEPCO) must pay to generators goes up accordingly.

KEPCO’s room to pass this cost through is nearly exhausted. Since 2022, KEPCO has kept residential tariffs frozen while raising industrial tariffs seven times to recover accumulated losses. Industrial electricity prices rose from $0.076/kWh (105.5 won/kWh) in 2021 to $0.132/kWh (181.9 won/kWh) by end-2025 — an increase of roughly 80% in four years (KEPCO tariff data, industrial category ≥300kW; MOTIE tariff adjustment announcements 2022–2025).

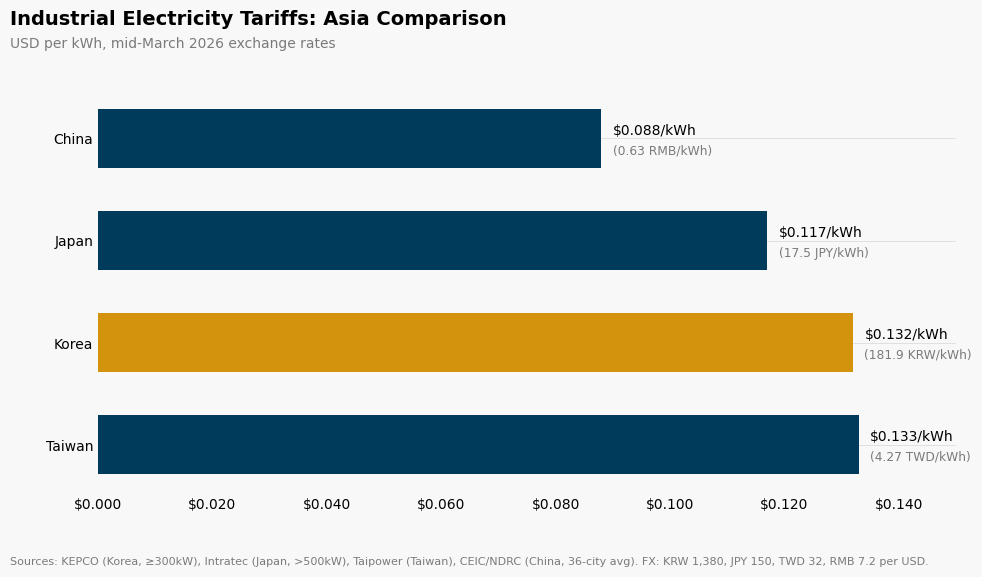

Using mid-March 2026 exchange rates (KRW 1,380, JPY 150, TWD 32, RMB 7.2 per USD) and published industrial tariff benchmarks, Korea’s industrial rate now stands at approximately $0.132/kWh — virtually identical to Taiwan’s $0.133/kWh (Taipower, NT$4.27/kWh), which Taipower has held steady precisely to protect its semiconductor and electronics manufacturers. Korea is now more expensive than Japan’s industrial rate of roughly $0.117/kWh (Intratec, >500kW) and carries a 50% premium over China’s $0.088/kWh (CEIC/NDRC, 36-city average, 35kV+, ~0.63 RMB/kWh). Four years ago, Korea’s low industrial electricity price was a selling point for foreign manufacturers. That advantage is gone.

If the Hormuz blockade pushes SMP higher in Q3, KEPCO faces a narrow set of options. Residential tariffs remain politically untouchable. Industrial tariffs have already absorbed most of the adjustment burden. Another industrial hike is the path of least resistance — but it would push Korea further above Japan and closer to the price levels that Korean manufacturers have long argued make domestic production uncompetitive against Chinese rivals.

The pattern is familiar. In 2022, LNG price surges pushed SMP above $0.145/kWh (200 won/kWh). The government deployed the SMP cap as a policy tool to limit KEPCO’s wholesale cost exposure, but it was not enough. Tariffs stayed frozen for nine months. KEPCO absorbed the residual gap. Between 2021 and 2023, KEPCO’s cumulative operating losses reached approximately $31 billion (43 trillion won, per KEPCO Annual Reports).

KEPCO’s balance sheet has not recovered enough to absorb another external fuel shock. Total debt still exceeds $145 billion (200 trillion won). The utility returned to profit in 2025 with operating income of $9.8 billion (13.5 trillion won), but $3.1 billion (4.3 trillion won) of that — roughly a third — goes to interest alone, at a daily rate of $8.6 million (11.9 billion won per day). Any further rise in LNG-linked wholesale costs narrows KEPCO’s room to absorb the gap internally or delay tariff adjustments for long (KEPCO financial statements and 2025 earnings announcement).

For manufacturers with Korean operations, the operating cost assumption needs to be revisited. Most industrial users built their 2026 budgets assuming a tariff freeze at around $0.134/kWh (185.5 won/kWh) — a reasonable assumption given KEPCO’s pattern of holding rates steady once political resistance builds. If the Hormuz crisis forces another industrial hike, that budget line breaks. Korea’s industrial tariff advantage over Japan and Taiwan — a standard line in investment pitch decks as recently as 2022 — no longer exists, and the gap is moving in the wrong direction.

Korea’s industry and energy ministry has three options, and none of them work. Raise industrial tariffs again, and the manufacturing competitiveness argument — the same argument the ministry uses to justify Korea’s entire industrial energy policy — erodes further. Start raising residential tariffs, and the political cost is immediate. Reintroduce the SMP cap, and the wholesale market distortion returns. Each path carries a cost — and the ministry knows it. The last time KEPCO’s balance sheet broke, over $72 billion (100 trillion won) in AAA-rated bonds hit the market in a single year, distorting Korea’s entire corporate bond market. That memory constrains every option on the table. None of them solve the underlying problem: KEPCO’s tariff structure was not designed to absorb repeated external fuel shocks while simultaneously recovering from the last one.

Watch KOGAS’s spot procurement costs through April. If the blockade extends beyond three weeks, the Q3 SMP impact becomes unavoidable. The most likely outcome: industrial tariffs absorb another round. The question is how much more they can absorb before manufacturers start shifting capacity to countries where the power bill is half the price.

Base case: Blockade resolves within 4 weeks. LNG spot prices ease by May. Q3 SMP rises modestly but stays below $0.109/kWh (150 won/kWh). KEPCO absorbs without a tariff hike. Industrial competitiveness gap widens but stays manageable.

What I’m watching: KOGAS spot procurement costs through April. JKM vs Title Transfer Facility (TTF) spread as a proxy for Asian panic buying. Any KEPCO bond issuance announcements in Q2.

What would change my mind: Blockade extends past 6 weeks, or a second supply disruption (Sabine Pass outage, Australian maintenance overlap) compounds the shortage. In that scenario, SMP pressure intensifies enough to force either a tariff hike or SMP cap reintroduction before Q4.

This is the first issue of Korea Energy Insight. Subscribe for future issues that connect Korea’s energy policy to prices, project economics, and industrial competitiveness.

Next month’s Deep Dive will examine how Korea’s LNG capacity auction design interacts with this new fuel cost environment — and why the bidding incentives may produce even more distorted outcomes than the market expects.