The Grid Stability Bill: What Spain's Blackout Means for Korea's Power Assets

Renewables will keep scaling. The harder question is what the grid needs to absorb them — and who pays.

DEEP DIVE

On March 20, ENTSO-E (European Network of Transmission System Operators for Electricity) published its final report on the April 2025 Iberian blackout — 472 pages, 49 experts, 11 months of investigation. The event that knocked 31 GW offline in seconds was not caused by a lack of generation, a cyberattack, or insufficient inertia. It was caused by something the grid was not designed to handle: a cascading overvoltage collapse in a system where the rules had not caught up with the generation mix.

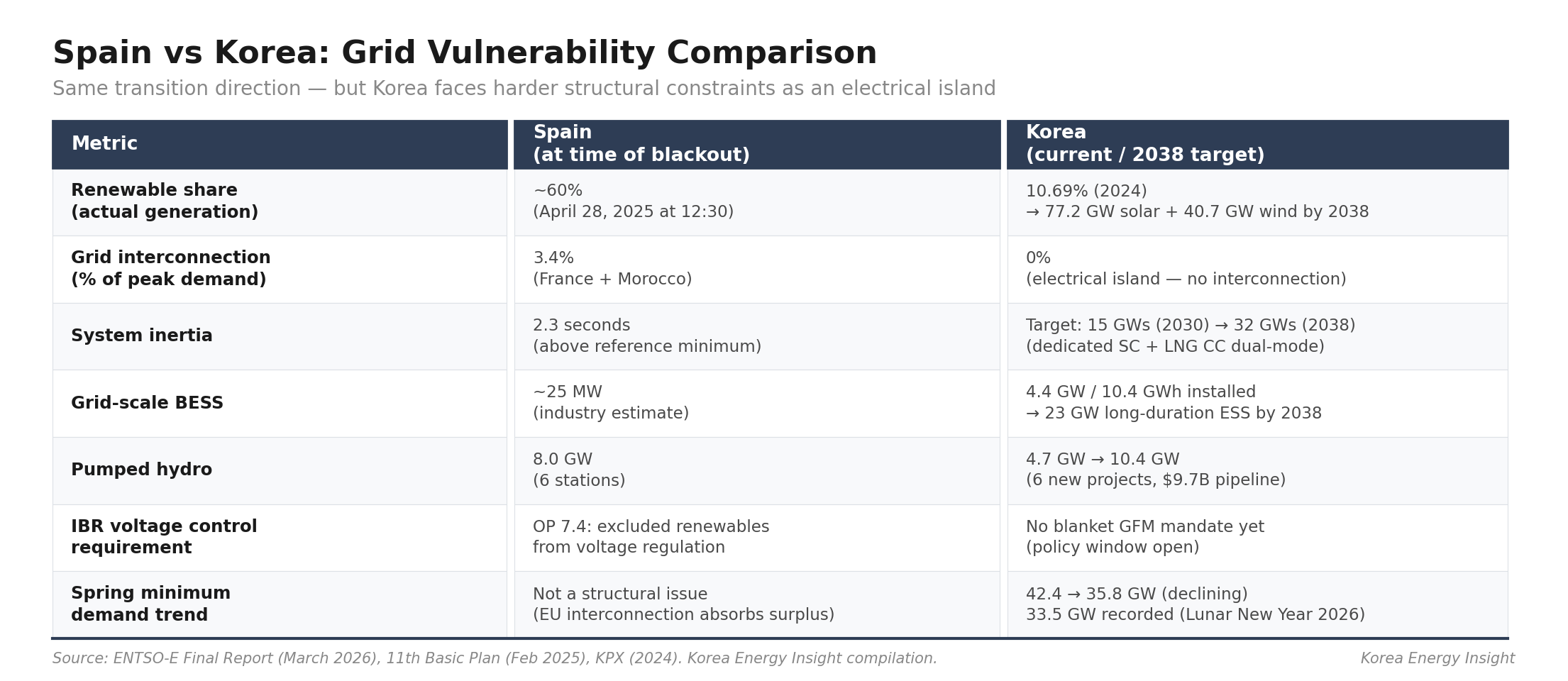

At 12:30 on April 28, 2025, solar was supplying roughly 60% of Spain’s electricity — 18,068 MW out of 25,184 MW of operating demand. System inertia measured 2.3 seconds, above the reference minimum. Within three minutes, a sequence of overvoltage trips — 355 MW, then 727 MW, then 928 MW — cascaded across the network. By 12:33:19, the Iberian Peninsula had lost synchronism with the rest of Europe. By 12:33:21, interconnections with France and Morocco were severed. Continental Spain and Portugal went dark for up to 16 hours. It was the worst blackout in Europe in over two decades — and, per ENTSO-E, the first in the Continental European synchronous area caused by overvoltage cascading rather than a generation shortfall.

The Political Framing and the Engineering Diagnosis

The report’s official position is that renewables did not cause the blackout. Spain’s prime minister called claims to the contrary “lies.” The ENTSO-E panel chairman described it as a “perfect storm of multiple factors.” These statements are technically accurate. They are also incomplete.

The engineering diagnosis in the same report tells a more specific story. At the time of the event, 80% of Spain’s solar fleet operated with grid-following inverters running at fixed power factor — meaning they could not participate in dynamic voltage control. Spain’s grid operating procedure, known as OP 7.4, allowed only conventional synchronous generators to provide voltage regulation. Renewables and batteries were excluded by rule. When voltage began to rise, the inverter-based resources that were generating most of the country’s electricity had no mechanism to help stabilize it. Instead, their protective settings tripped them offline, which pushed voltage higher, which tripped more generators — a self-reinforcing collapse that the grid operator’s monitoring systems did not flag until it was too late.

Spain also operated its 400 kV grid with a normal voltage ceiling of 435 kV — 15 kV higher than the European standard of 420 kV. With protective disconnection set at 440 kV, the operating margin was just 5 kV — leaving very limited headroom for normal operating variation. One regulator’s technical shorthand: relabeling higher voltage as “normal” does not lower the voltage.

The political framing reassures. The engineering diagnosis tells you where the money needs to go. Renewable expansion is both inevitable and justified — decarbonization targets, energy security concerns from LNG supply chain risks to the Hormuz chokepoint, and declining generation costs all point in one direction. The question is not whether renewables will scale. The question is whether the grid infrastructure and market design are scaling with them. In Spain, they were not. The grid stability bill came due, and no one had budgeted for it. Korea is pursuing the same transition on harder terms — faster renewable targets, shrinking spring demand, and zero interconnection.

Korea’s Structural Exposure

Spain’s exact failure mode — overvoltage cascading at 60% renewable penetration — should not be mechanically transplanted to Korea. The point is not identical topology, but identical stress direction: higher IBR (inverter-based resource) share, fewer synchronous machines online, tighter voltage and frequency management requirements.

The 11th Basic Plan for Electricity Supply and Demand (제11차 전력수급기본계획), confirmed in February 2025, targets 77.2 GW of solar and 40.7 GW of wind by 2038 — up from 27.1 GW and 2.3 GW today. Renewable generation accounted for 10.69% of actual output in 2024, according to Korea Power Exchange (KPX). Spain was at roughly 60% when its grid collapsed. Korea is not there yet. But the structural vulnerability is already present, because Korea has something Spain did not: zero interconnection.

Spain’s Iberian grid connects to France and Morocco at 3.4% of peak demand — well below the EU’s 10–15% target, but enough to have limited the damage if the cascade had developed more slowly. Korea connects to nothing. It is an electrical island. When a grid event occurs, there is no neighboring system to absorb the shock. Every megawatt of stabilization must come from domestic resources.

This is not a theoretical concern. Korea already experiences the early symptoms of the same dynamic that brought down Spain’s grid. KEI’s tally of KPX market data shows 26 confirmed hours of zero SMP (system marginal price) between January 2025 and March 2026 — all during daytime solar peaks. Spring minimum demand has dropped from 42.4 GW to 35.8 GW, with the 2026 Lunar New Year recording 33.5 GW. As the renewable share grows and net demand shrinks, the number of synchronous generators online at any given moment will decline. With them goes the system’s natural source of inertia, voltage support, and fault current.

The Investment Korea Is Already Making — and What Is Missing

Korea’s policy response goes further than the headline “10.69% renewable share” suggests. The 11th Basic Plan does not just set generation targets — it explicitly quantifies the grid stability investment required to support them.

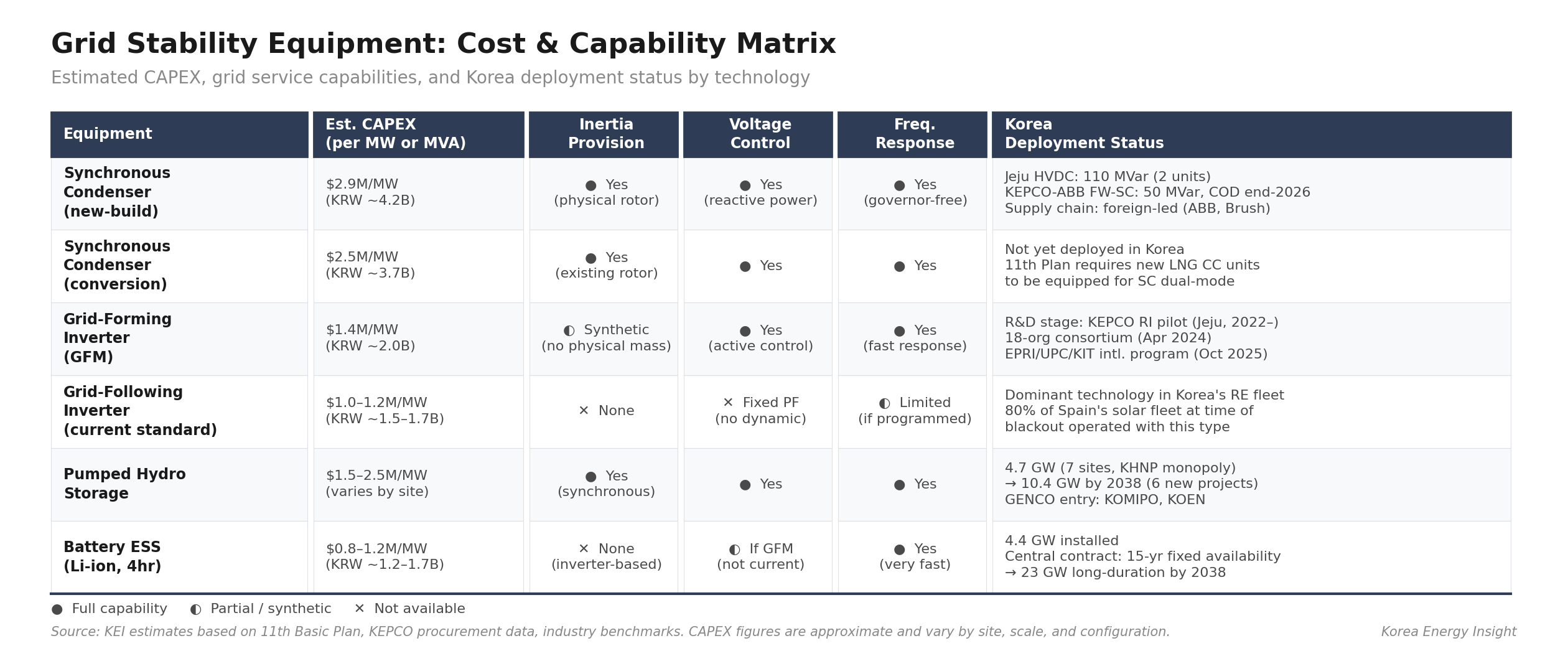

For inertia, the plan sets cumulative requirements of 15 GWs by 2030, 27 GWs by 2035, and 32 GWs by 2038 — expressed in gigawatt-seconds, not in machine counts. It specifies two delivery mechanisms: dedicated synchronous condensers and, notably, new LNG combined-cycle units equipped for dual-mode synchronous condenser operation. The exact language is “동기조상기 겸용운전 성능 구비” — equipped with synchronous condenser cooperation capability. This is a policy signal that new gas-fired assets in Korea are not just peaking plants. They are being designed as grid-forming infrastructure.

For storage, Korea has already operationalized the energy storage system (ESS) central contract market — a 15-year fixed-price availability structure that converts battery storage from a failed arbitrage play into an infrastructure asset (KEI Issue #6. The 11th Basic Plan targets 23 GW of long-duration ESS by 2038. Pumped hydro is planned to more than double, from 4.7 GW to 10.4 GW, with a pipeline of six new projects worth an estimated $9.7 billion (KRW 14 trillion; all USD conversions at approximately KRW 1,450/USD). The April 2025 amendment to the Power Market Operating Rules improved pumped hydro economics by an estimated $368 million (KRW 533 billion) per year across the existing 16-unit fleet, according to Korea Hydro & Nuclear Power’s (KHNP) back-calculation of 2020–2024 operating data — combining excess-plan energy settlement reform ($330 million / KRW 478 billion from reduced pumping costs) with a new settlement for under-frequency load shedding service ($38 million / KRW 55 billion in maintenance payments).

Yet the gap between target and installed base is wide. Korea’s only publicly verifiable operating synchronous condensers are two 55 MVar units at the Jeju high-voltage direct current (HVDC) converter station — 110 MVar total, on an island, for a system that needs 32 GWs of inertia by 2038. The sole new project is a Korea Electric Power Corporation (KEPCO)–ABB flywheel synchronous condenser in Jeju: 50 MVar, 500 MW-s of inertia, contract value of $19 million (KRW 28 billion), targeted for commissioning by end-2026. The supply chain remains foreign-led — ABB for the new unit, legacy British Brush generators for the existing ones. Korean firms are visible in localization and demonstration efforts, not yet in commercial-scale deployment.

For grid-forming inverters, the picture is earlier-stage still. Korea’s power research institute began grid-forming (GFM) technology development in 2022, with a Jeju pilot. A national industry consortium of 18 organizations launched in April 2024. An international R&D program with the Electric Power Research Institute (EPRI), Universitat Politècnica de Catalunya (UPC), and Karlsruhe Institute of Technology (KIT) started in October 2025. But no country has yet imposed a blanket nationwide GFM mandate — though every major market is moving toward stricter IBR voltage-support requirements. Australia has a voluntary specification and is in active rule development. The US baseline under the Federal Energy Regulatory Commission’s (FERC) Order 827 requires IBR voltage regulation but not full grid-forming capability. The EU is formalizing GFM requirements under its revised network code. Spain updated its OP 7.4 in June 2025, after the blackout. Korea still has a policy window. Spain’s experience suggests that window will not stay open indefinitely.

What This Means for Asset Valuation

The investment implications split four ways, all tied to the same underlying cost: the grid stability spending that accompanies every gigawatt of new renewable capacity.

First, renewable project economics will absorb higher CAPEX. As grid-forming requirements, voltage control obligations, and curtailment-compensation mechanisms tighten, the cost of connecting inverter-based resources to the grid will rise. Developers modeling Korean projects should already be stress-testing for rising grid-connection costs. The regulatory trajectory is moving toward stricter IBR requirements — the only question is timing. The CAPEX premium for grid-forming over grid-following inverters is currently estimated at roughly $1.4 million/MW (KRW ~2 billion) versus up to $2.9 million/MW (KRW ~4.2 billion) for synchronous condensers — but the premium will narrow as scale and competition increase.

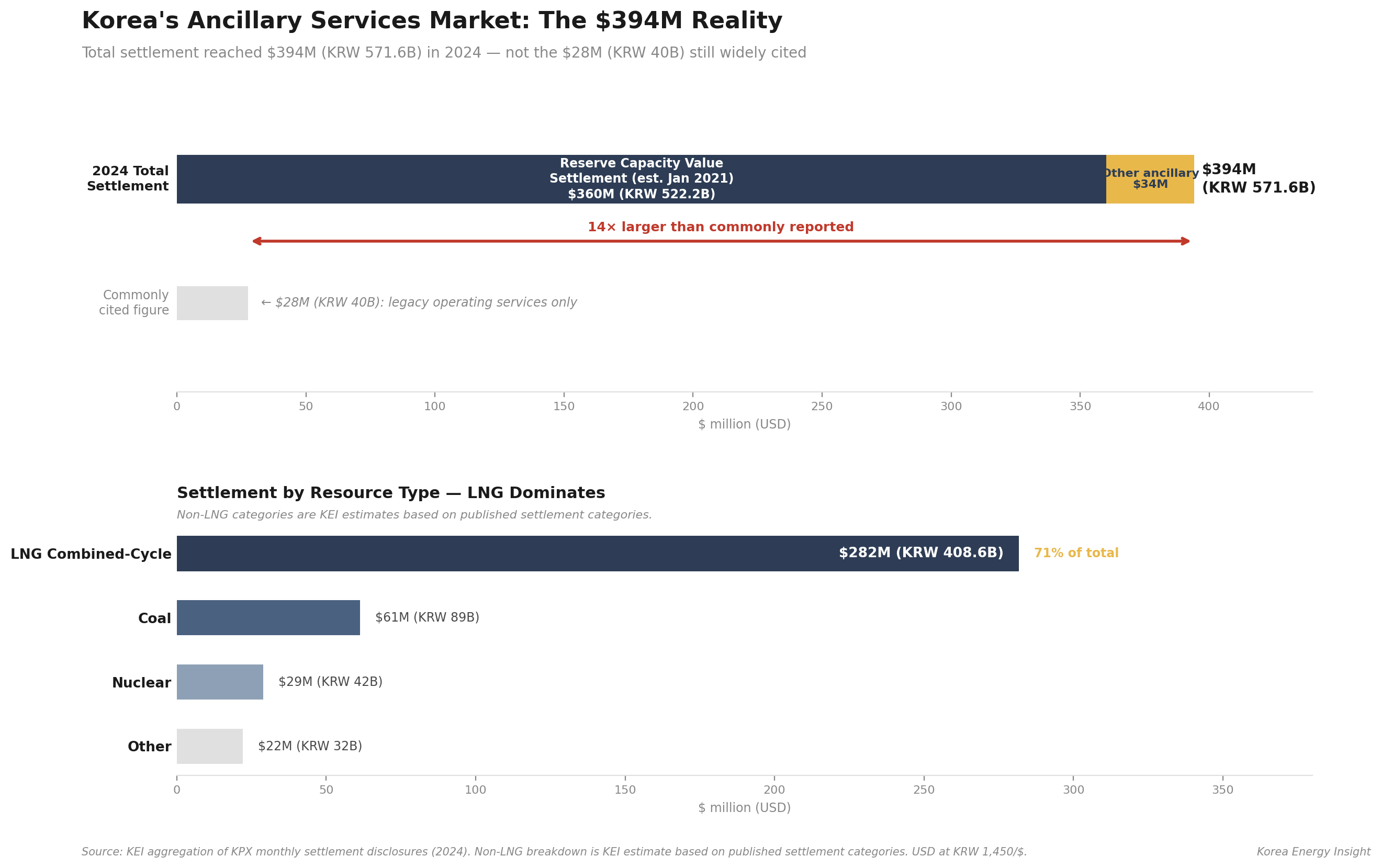

The ancillary services market is the least visible but most immediate channel. Based on KEI’s aggregation of KPX monthly settlement disclosures, Korea’s total ancillary service settlement in 2024 reached $394 million (KRW 571.6 billion) — not the $28 million (KRW 40 billion) figure still cited in some market overviews. The difference is the reserve capacity value settlement, introduced in January 2021, which accounted for $360 million (KRW 522.2 billion) alone. This settlement primarily recognized the value of services that generators were already providing — automatic generation control (AGC) and governor-free (GF) frequency response. As the ancillary services framework matures, more diverse services are expected to be defined, priced, and procured separately. LNG combined-cycle plants received $282 million (KRW 408.6 billion) of the total — making them the single largest beneficiary of Korea’s ancillary services regime. From my years in policy and project development, there is a catch that is not immediately visible: the capacity payment formula already deducts expected ancillary income from the reference capacity price. The net revenue picture is more complex than a simple addition of new income streams.

Third, pumped hydro and synchronous condensers represent long-duration, high-inertia assets with explicit government backing and quantified demand. The $9.7 billion (KRW 14 trillion) pumped hydro pipeline is now attracting generation companies (GENCOs) beyond the traditional monopoly operator KHNP — Korea Midland Power (KOMIPO) is pursuing Gurye (500 MW) and Bonghwa, Korea South-East Power (KOEN) is targeting Geumsan (500 MW). But the economics remain structurally challenging. Most existing stations operate at a loss — public reporting indicates roughly $69 million (KRW 100 billion) per unit per year on a historical basis — because the original nighttime-pumping model has been upended by daytime solar surplus. Units designed to pump at night now pump during the day, at higher electricity costs, with no tariff mechanism to compensate the shift. The April 2025 rule amendment helps, but does not close the gap. Industry participants indicate that only fully depreciated stations currently operate in the black.

Then there is LNG. Combined-cycle assets deserve revaluation — not because the assets have changed, but because the valuation model applied to them has not kept pace with Korea’s grid reality. The conventional approach to valuing Korean gas plants starts with SMP-based energy revenue — a metric that has been declining structurally as renewable penetration pushes wholesale prices down (KEI Issue #4). But the 11th Basic Plan now requires new LNG CC units to be equipped for synchronous condenser dual-mode operation. The ancillary services market is already paying LNG plants $282 million (KRW 408.6 billion) per year. As the renewable share grows, the grid services that synchronous gas turbines provide — inertia, voltage control, frequency response, black start — become more valuable, not less. An M&A valuation that prices a Korean LNG CC asset on energy margins alone is likely underpricing the asset. The ancillary revenue stream, the policy mandate for dual-mode capability, and the structural scarcity of synchronous resources on an island grid all create a value floor. SMP erosion alone does not capture it.

So What

The grid stability bill is not a future risk. It is a current expenditure with identifiable recipients. Korea’s ancillary services market already paid out $394 million (KRW 571.6 billion) in 2024 (KPX). The 11th Basic Plan already mandates 32 GWs of inertia, 10.4 GW of pumped hydro, and 23 GW of long-duration ESS by 2038. New LNG combined-cycle units are already required to operate as synchronous condensers. The Ministry of Trade, Industry and Energy (MOTIE) and KPX are not waiting for the next blackout. Spain showed what happens when grid rules fall behind the generation mix, and Korea is building the response before it faces the same test. The question for investors is not whether this spending will happen. The question is which assets capture the value. Renewable developers will face higher connection costs. Storage operators are already transitioning from arbitrage to infrastructure contracts. Pumped hydro and synchronous condensers are moving from government-subsidized backup to explicitly priced grid services. And LNG plants — the assets most commonly written off as stranded in a decarbonizing world — carry an option value in synchronous grid services that energy-margin-only valuations miss entirely. If any one of these investment channels fails to materialize on an island grid with no interconnection, there is no fallback.

What to Watch

Three indicators will signal whether Korea’s grid stability investment is keeping pace with its renewable ambition.

Real-time ancillary services market — mainland rollout timeline. Currently piloted in Jeju with no confirmed expansion date as of March 2026. If this market goes live on the mainland, it reprices flexibility in real time rather than through annual administered rates. That is the point at which ancillary revenue becomes a tradeable price signal — and LNG CC and fast-response storage assets get repriced first.

Jeju flywheel synchronous condenser — commissioning by end-2026. Korea’s first high-inertia unit. A test case for cost, performance, and domestic supply chain readiness that will determine whether the 32 GWs target is achievable at scale. If delivered on budget, it validates the CAPEX assumptions behind the entire synchronous condenser and pumped hydro pipeline.

LNG CC transaction with ancillary services valued as a separate line item. When a buyer prices grid services independently of energy margins, it signals that the market’s valuation framework for Korean gas assets has shifted. That transaction will mark the point where synchronous scarcity on an island grid stops being an analytical argument and starts showing up in deal pricing.

If this analysis is relevant to your team’s Asia power market strategy, consider forwarding it to colleagues evaluating grid infrastructure and generation assets in Korea.