The Storage Pivot: How Korea Turned a Money-Losing Battery Market into a 15-Year Infrastructure Asset

SK On went from zero to 50%. LFP pricing and foreign capital did the rest.

MARKET SIGNAL

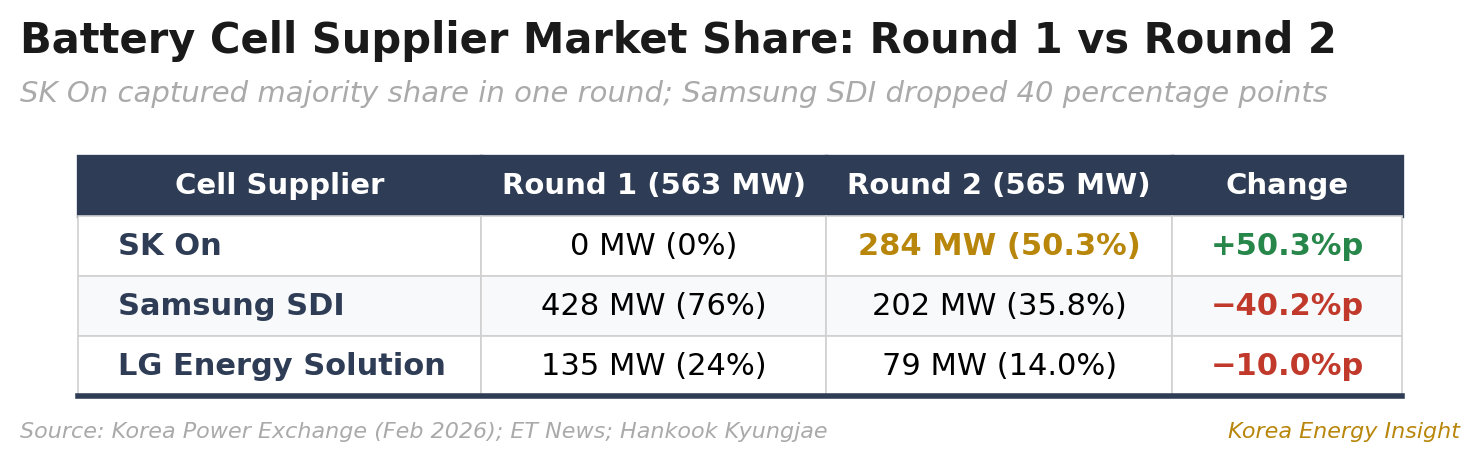

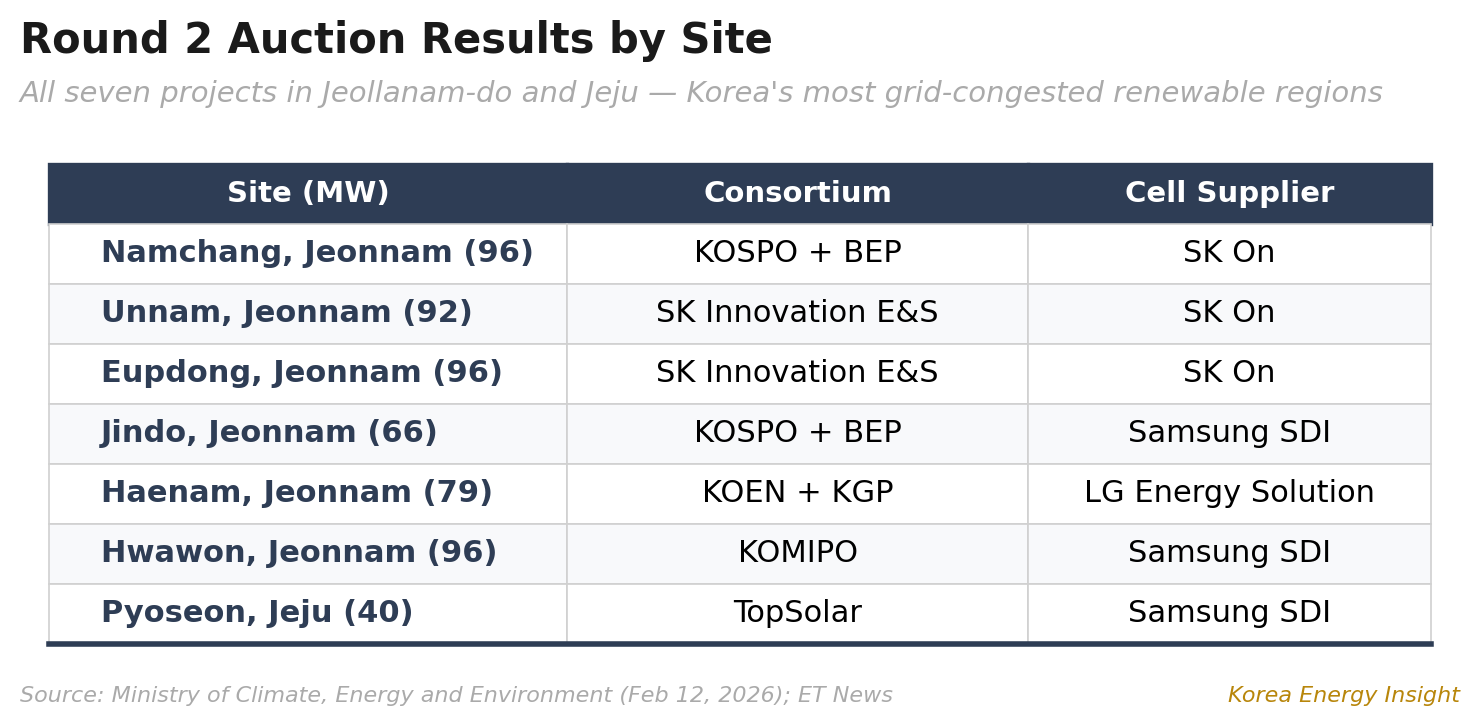

In February, Korea announced preferred bidders for up to 565 MW across seven ESS central contract projects — six in Jeollanam-do and one in Jeju (Ministry of Climate, Energy and Environment, February 12, 2026). The result upended the battery industry’s pecking order. SK On — which failed to win a single megawatt in the first round — captured 284 MW, or 50.3% of the total. Samsung SDI dropped from 76% to 35.8%. LG Energy Solution fell from 24% to 14% (ET News).

This was more than a procurement result. Korea has created a market where grid-scale BESS can be financed like contracted infrastructure — and KKR and BlackRock have noticed.

Why standalone storage didn’t work — and what changed

Standalone grid-scale BESS has struggled commercially in Korea for a straightforward reason. The gap between charging costs and the system marginal price (SMP) at discharge has been too narrow — or in some periods, inverted — for a pure arbitrage model to generate positive returns. No amount of operational optimization can fix an arbitrage that does not exist.

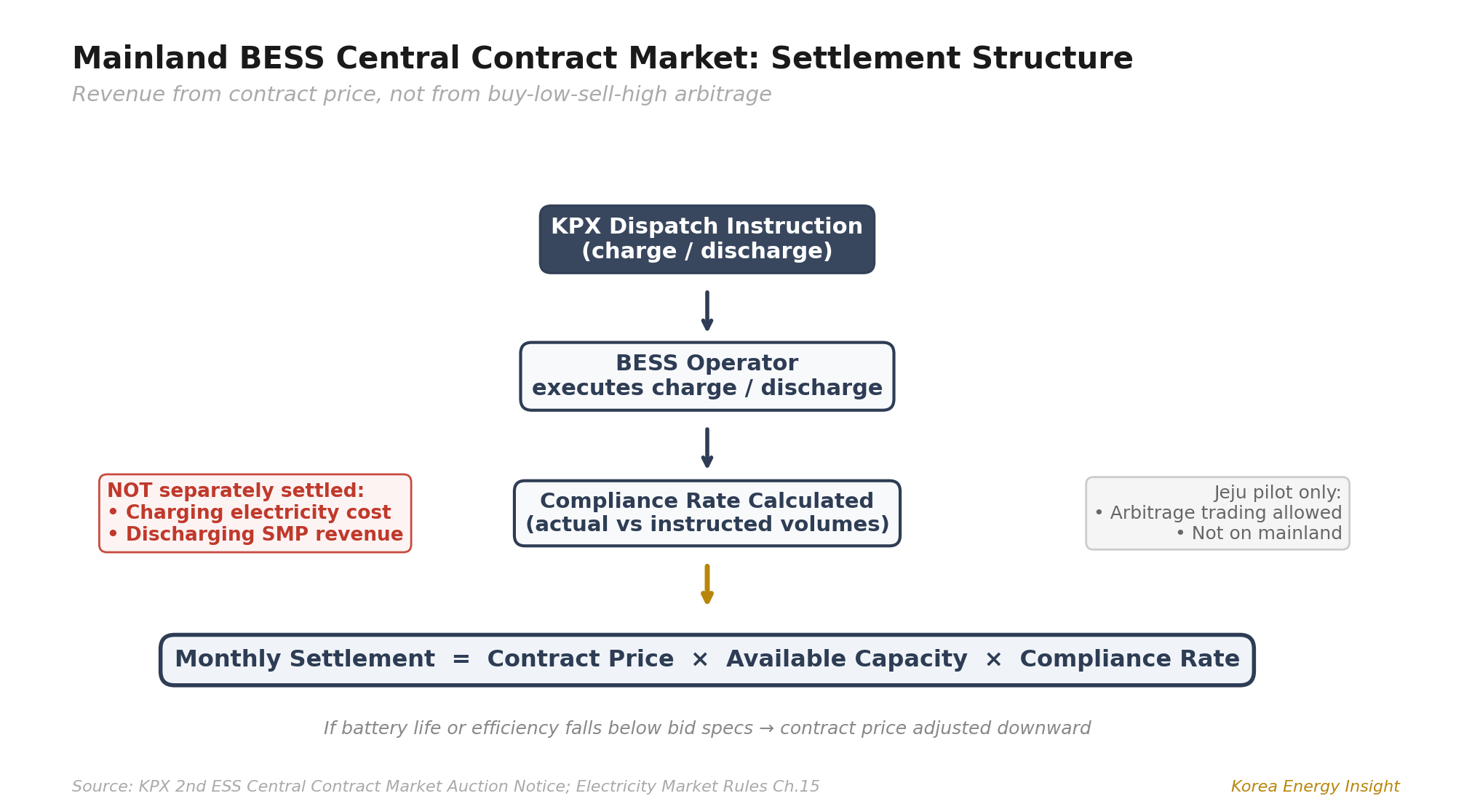

The ESS central contract market, established under Chapter 15 of the Electricity Market Rules (전력시장운영규칙), changed the revenue structure. Winning bidders receive a fixed contract price for 15 years. Monthly settlement follows a formula: contract price × available capacity × compliance rate. The bid price itself is defined as total project cost — excluding charging electricity costs — converted into a unit fixed cost per available capacity over the contract period (KPX 2nd auction public notice).

The critical design choice: on the mainland, charging costs and discharging revenues are not separately settled. The operator does not buy charging electricity at a market rate or sell discharged power at SMP. Instead, it receives the contract payment in exchange for following KPX’s dispatch instructions. The compliance rate tracks how accurately the operator executes those charge and discharge commands. Miss the dispatch window, and the monthly payout shrinks proportionally. If guaranteed battery life or operating efficiency falls below bid specifications, KPX’s central contract market committee can adjust the contract price itself.

In other words, this is closer to an availability contract than a pure arbitrage trade.

Charging and discharging still happen — and they drive real costs through round-trip losses, battery degradation, and augmentation needs. But those costs sit on the expense side of the project finance model, not as a separate revenue line. The business model for mainland BESS is “fixed contract payment minus performance and degradation risk,” not “buy low, sell high.”

Industry estimates place the first-round contract price in the upper 20s to low 30s won per kWh. At that level, with LFP-based CAPEX now lower than the NCA-era benchmark, the return profile is attractive enough to clear the investment thresholds of global infrastructure funds. Separately, Jeju’s second-round pilot introduced arbitrage trading for the first time — allowing BESS operators to buy and sell electricity at market prices — but this mechanism does not apply to the mainland market.

For investors, the attraction is straightforward. Revenue is fixed, while most of the remaining risk is operational. The remaining variables — dispatch compliance, battery degradation, augmentation timing, operating efficiency — are performance risks, not market risks. And performance risks can be contractually shifted. An SPC that wraps EPC completion guarantees, OEM warranties on cell life and efficiency, and O&M availability commitments into back-to-back contracts can push most operational risk below the equity layer. That makes the project look more like contracted infrastructure than a trading asset, though execution risk still matters.

The LFP pivot

The first auction in mid-2025 was Samsung SDI’s sweep. Its nickel-cobalt-aluminum (NCA) cells captured 76% of the 563 MW, with LG Energy Solution taking the rest on LFP from its Nanjing facility. SK On won nothing.

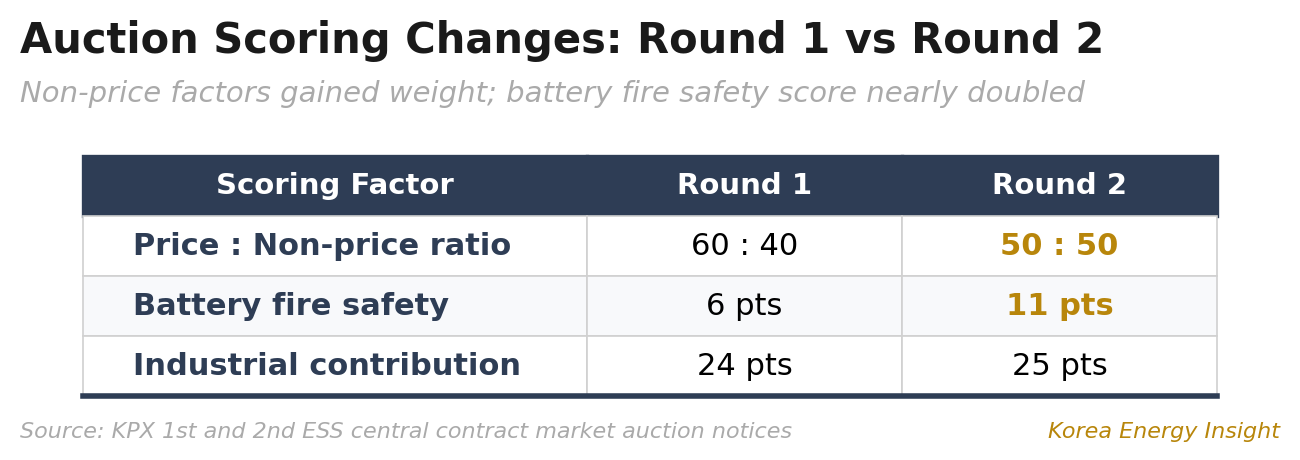

Two things changed for the second round. KPX shifted the price-to-non-price scoring ratio from 60:40 to 50:50 and nearly doubled the battery fire safety score from 6 to 11 points (KPX 1st and 2nd auction notices). But the more decisive factor was chemistry. SK On and LG Energy Solution both entered with LFP cells — materially cheaper on raw materials than NCA — and in an auction where price still accounts for half the score, that cost advantage translated directly into winning bids.

The result reshuffled the order. SK On took 284 MW (50.3%) by supplying LFP cells to three consortiums, reversing a complete shutout in the first round. Samsung SDI held 202 MW with NCA — a defensive success given the rule changes, with its Ulsan LFP line expected to enter production in Q4 2026. LG Energy Solution’s 79 MW was the weakest result despite the most global LFP experience; the absence of domestic LFP production likely hurt it under the 25-point industrial contribution score. Its Ochang plant, targeting ESS-grade LFP from 2027, will determine whether this gap closes (ET News; MoneyToday; LG Energy Solution).

The capital structure behind the batteries

Every winning consortium must form a special purpose company (SPC) to execute the project. Several of those SPCs carry foreign infrastructure capital at their core.

KKR-backed Korea Gigaplatform (KGP) partnered with Korea South-East Power (KOEN) for the 79 MW Haenam project. Bright Energy Partners (BEP), with BlackRock as financial investor, partnered with Korea Southern Power for 162 MW across two Jeollanam-do sites (E2 News, January 2026).

The setup is lopsided. The financing layer is open to foreign capital, but the scoring system strongly favors Korean supply chains. The auction does not formally ban foreign cell supply, but awards 25 points to domestic industrial contribution and requires origin documentation for cathode, anode, separator, electrolyte, PCS, and BMS — a scoring structure that makes non-Korean supply chains uncompetitive in practice (KPX 2nd auction notice). For infrastructure funds, that is a familiar profile: long-term contracted revenue in a stable OECD market.

In the global ESS battery market, the top seven Chinese manufacturers accounted for 83.3% of shipments in 2025. Samsung SDI and LG Energy Solution together held roughly 4% (SNE Research, January 2026). Korea’s central contract market is one of the few venues where Korean battery makers can build LFP operating track records before competing with CATL and BYD on open ground.

Because there are few realistic alternatives, battery suppliers end up taking on more performance risk than they might otherwise accept. To make the SPC financeable, the battery OEM must provide thick performance guarantees — cell capacity, degradation curves, round-trip efficiency, augmentation commitments. The auction notice itself requires manufacturers to submit guaranteed life, operating efficiency, and equipment procurement details at the bid stage, with ongoing compliance monitoring after commercial operation (KPX 2nd auction notice). In practice, the battery maker ends up controlling not just cell supply but system-level performance. For companies chasing volume in a depressed EV market, accepting that risk is the price of staying in the game.

Base case

The government has signaled a third auction within 2026 (Ministry of Climate, Energy and Environment, February 2026), with a cumulative target of 2.22 GW by 2029 under the 11th Basic Plan’s goal of 23 GW in long-duration ESS by 2038 (11th Basic Plan, amended March 2025). Jeollanam-do will remain the primary location — the region operates approximately 10–11 GW of renewable capacity with additional capacity in the permitting pipeline, and solar curtailment reached 44 days in the first half of 2025 alone (Newsworks, September 2025). SK On’s LFP pricing advantage is likely to hold in the near term. Samsung SDI’s LFP entry in late 2026 and LG Energy Solution’s Ochang line in 2027 should narrow the gap over time.

What I’m watching

Whether the third auction maintains the 50:50 scoring ratio or tilts further toward non-price factors. How fast SK On’s Seosan LFP line reaches volume production. Whether LG Energy Solution accelerates its Ochang timeline to capture domestic content points before the third round.

What would change my mind

A reversion to 60:40 price weighting would re-entrench the lowest-cost bidder regardless of domestic content. A sharp further decline in Chinese LFP cell prices could pressure the implicit domestic supply chain barrier — if CATL or BYD were to build in Korea, the domestic competitive picture would look very different.

If this analysis is useful for your team’s Asia energy or battery storage strategy, consider forwarding it to a colleague.