Samsung and SK Hynix Need Power Now: Who Will Build the Plants for the World's Largest Chip Cluster?

The fastest-moving power projects are not on the government's plan. They are inside the cluster.

DEEP DIVE | Image: Samsung Electronics via Korea.net

Opening

In Part 1, KEI laid out the bottlenecks: undesignated LNG sites, delayed transmission, and a KEPCO balance sheet that cannot fund the buildout alone. The infrastructure will eventually arrive. The unresolved question is which assets arrive first and who owns them.

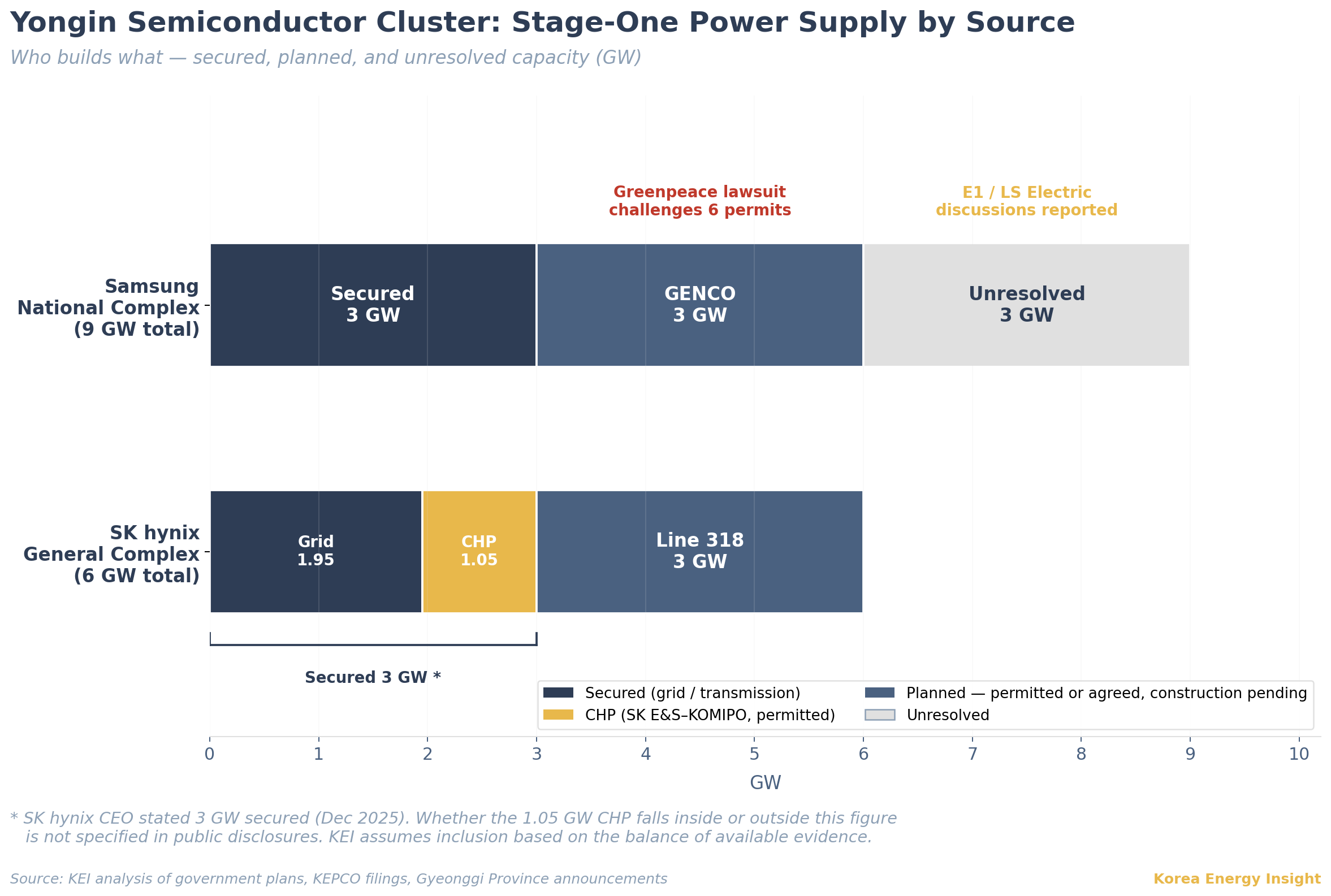

This issue examines the models already in motion: permitted CHP plants, self-consumption generation, regional tariff redesign, and on a longer horizon, industrial nuclear. The official three-stage plan still stands. But SK Innovation E&S (formerly SK E&S) and Korea Midland Power (KOMIPO) are already building a CHP inside the cluster, Samsung is in discussions with E1 and LS Electric, and the tariff regime is being redesigned to price in metropolitan power consumption. The sharpest divide is between the two companies at the center of the cluster: one already has an in-house energy operator, and the other is still looking for a partner.

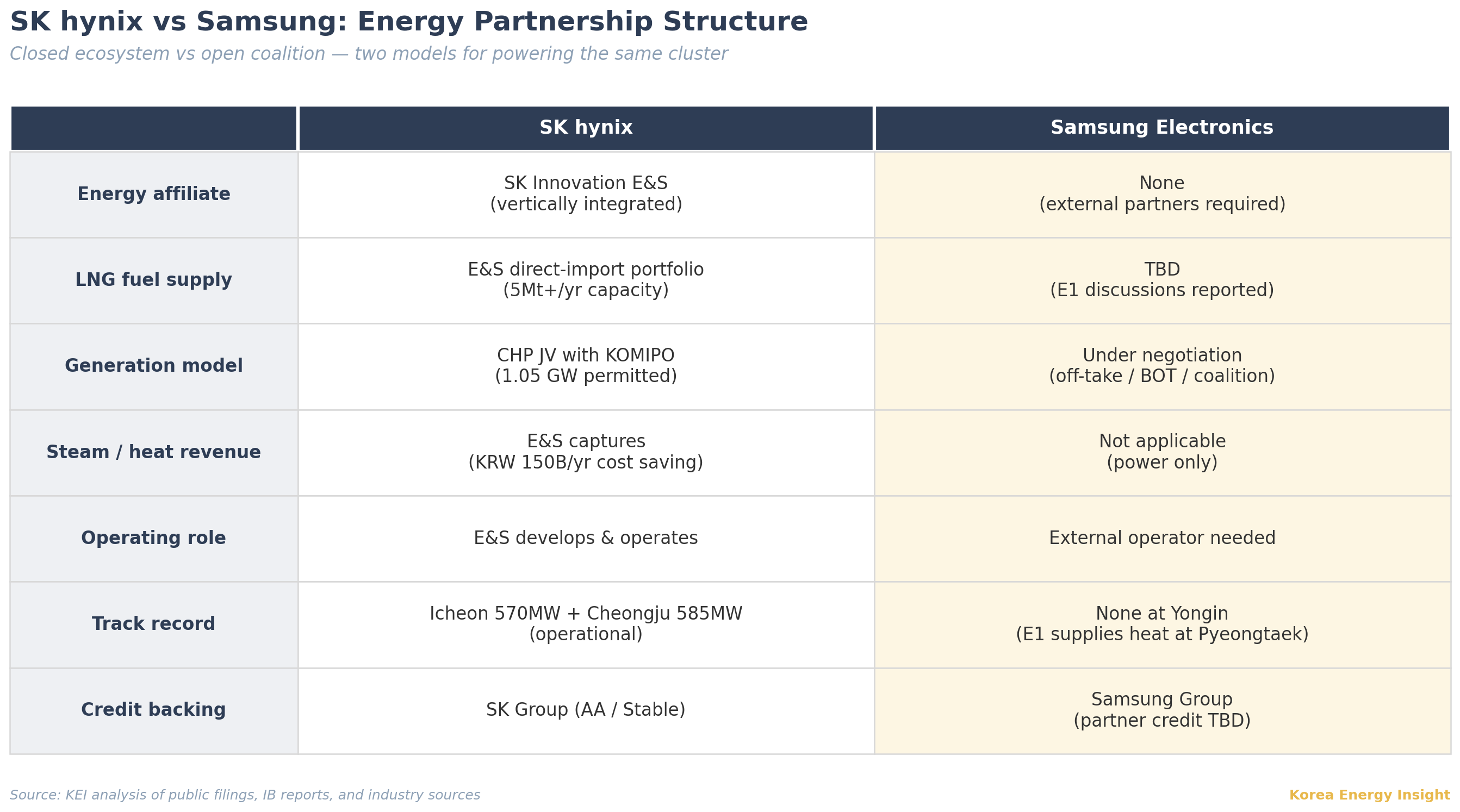

The SK Innovation E&S–KOMIPO CHP: a model in motion

SK Innovation E&S (formerly SK E&S) and Korea Midland Power (KOMIPO) received MOTIE’s final approval in August 2024 for a 1.05GW LNG combined heat and power (CHP) plant inside the Yongin cluster. The project is structured as a joint-venture SPC. Construction is expected to begin in 2026, though the original completion target has shifted and the final timeline remains subject to turbine procurement and financing closure. Electricity will be sold to KEPCO through the Korea Power Exchange (KPX) — a centrally dispatched generator. Process steam will be supplied directly to SK hynix’s first four fabs, with reported annual delivery capacity of 16 million tons. SK hynix has cited annual production cost savings of up to $103 million (KRW 150 billion; all USD conversions at approximately KRW 1,450/USD), cutting heat costs roughly 15% versus standalone boilers.

The JV works because it separates two very different revenue streams. KOMIPO, as the generation subsidiary, is positioned to manage wholesale power revenue and its SMP-linked volatility. SK Innovation E&S earns from the stable side: process steam supply to SK hynix’s fabs and direct-import LNG fuel sales from its own portfolio. Semiconductor fabs run year-round with flat thermal demand, unlike residential district heating that peaks in winter. The heat and gas revenues are smaller than wholesale power but far more predictable. SK Innovation E&S is Korea’s largest private LNG operator, with annual supply capacity exceeding 5 million tons and roughly 5GW of existing generation. Management has told investors the Yongin project will push the portfolio past 8GW and 10 million tons of LNG.

Metropolitan Seoul’s southern grid is structurally tight. A 1.05GW generator sitting inside a major industrial load center will likely dispatch regardless of day-ahead market outcomes — the system operator needs the local capacity for grid stability. By Korean new-build standards, that combination should put the project near the top of the bankability spectrum.

This is the third iteration of the same playbook. SK Innovation E&S already built and operates two LNG CHP units (570MW at Icheon and 585MW at Cheongju, totaling $1.16 billion (KRW 1.68 trillion)), supplying power and steam to adjacent SK hynix fabs. The unstated catalyst: Samsung’s Pyeongtaek fab had suffered a 30-minute blackout causing $34 million (KRW 50 billion) in losses, and the transmission line for the Pyeongtaek expansion had been stalled by resident opposition for five years. The same drivers apply to Yongin with greater force: transmission risk, cost advantage, and process reliability.

What the SK model means for deal flow

The SK side of the Yongin cluster is a closed ecosystem — SK Innovation E&S captures the gas supply, steam revenue, and operating role internally. But the financing is not closed. This CHP is only one piece of a much larger pipeline. Recent Korean LNG project financings are typically leveraged around 75–80% external capital, with construction costs ranging from $410–620 million (KRW 0.6–0.9 trillion) per 500MW for standard combined-cycle plants and higher for integrated CHP with steam infrastructure. Across the cluster, the total PF pipeline runs into the trillions of won. The KEPCO generation subsidiaries carry AAA credit ratings; recent GENCO bond issues have cleared at spreads of KTB+5bp at the short end to roughly KTB+45bp further out. SK Innovation E&S–KOMIPO adds another bankable tranche with SK Group credit (AA/Stable) behind it. For infrastructure debt investors, Yongin is emerging as one of the largest prospective sources of Korean energy-sector deal flow.

The permit pathway — and the lawsuit threatening it

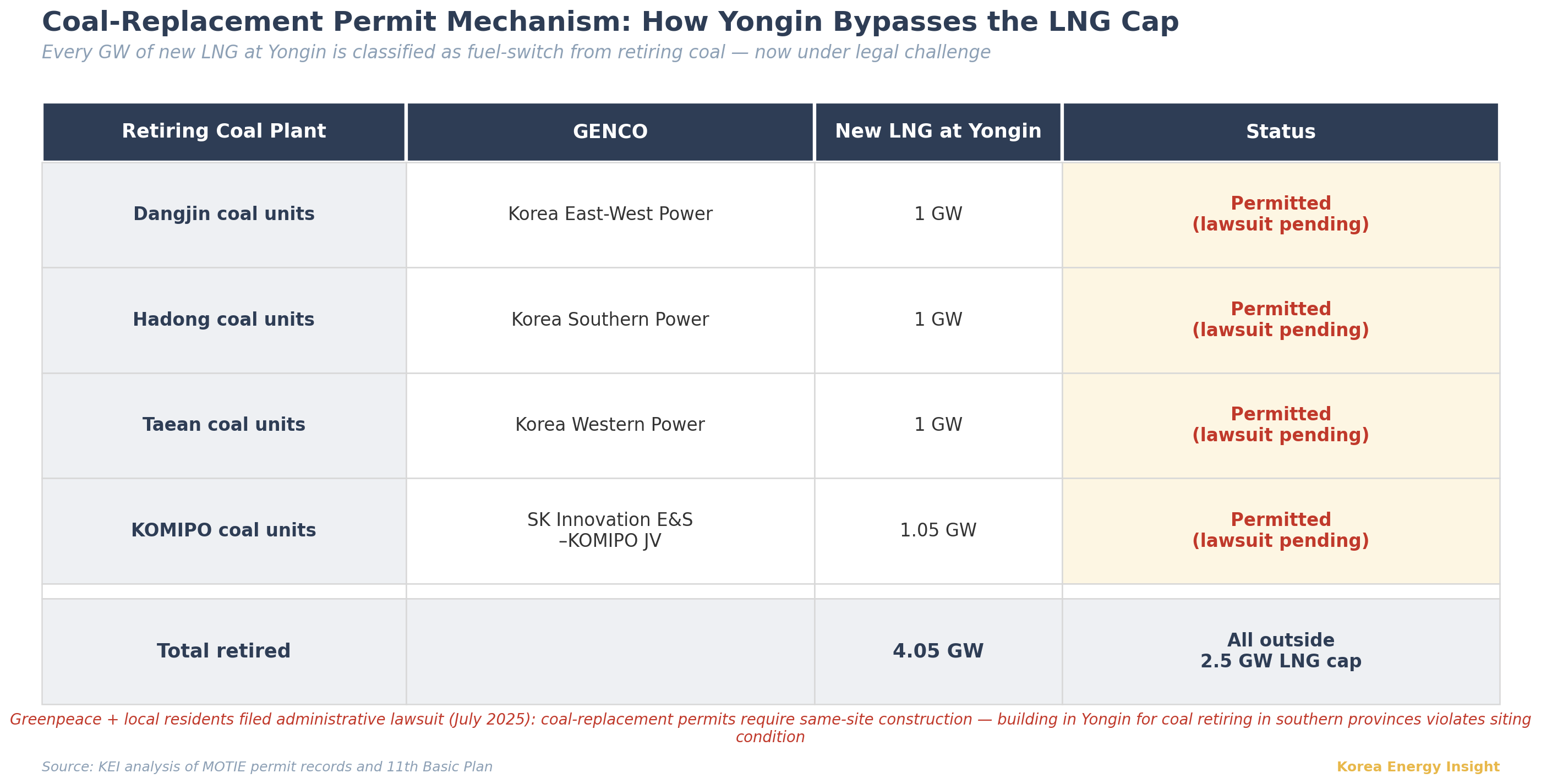

SK Innovation E&S initially applied for 1.2GW of new LNG capacity on its own. The application did not proceed in its original form — MOTIE determined that a net addition to the LNG fleet was unacceptable under carbon-neutrality constraints. The approved project was restructured to replace KOMIPO’s retiring coal units, classifying it as a fuel switch rather than a net addition. The same mechanism applies to the national complex’s 3GW: Korea East-West Power, Korea Southern Power, and Korea Western Power each secured permits for 1GW of LNG by retiring coal units at plants in Dangjin, Hadong, and Taean. Every gigawatt of new LNG generation planned for Yongin is a coal replacement. Market participants understand this classification to place the projects outside the 11th Basic Plan’s 2.5GW cap on net-new LNG through 2038.

That classification is now under legal challenge. In July 2025, Greenpeace and local residents filed an administrative lawsuit seeking to overturn the six permits, arguing that coal-replacement permits require the new plant to be built at the same location as the retiring unit. Building replacement capacity in Yongin for coal plants retiring in the southern provinces, they contend, violates the siting condition. The lawsuit is ongoing.

The mechanism worked for Yongin, but it is finite. Korea’s stock of retirable coal shrinks with each replacement. Future semiconductor clusters, battery complexes, or data center campuses that need firm on-site generation will find fewer coal units available to offset against. Yongin consumed one of the last large tranches of this regulatory workaround. And even what it consumed is contested. The risk is binary: either the permits hold and construction proceeds, or the legal basis for Yongin’s stage-one power plan unravels.

What Samsung doesn't have

SK hynix has SK Innovation E&S. Samsung Electronics does not have an equivalent. That gap has nothing to do with chip technology. SK Innovation E&S brings LNG supply, generation capacity, and district energy operating experience under one corporate umbrella — a vertically integrated energy affiliate that can build, fuel, and operate power plants for its sister company’s fabs.

Samsung C&T can build power plants (it constructed the Barakah nuclear complex in the UAE), but it does not operate them. Samsung SDI makes batteries; Samsung Engineering builds chemical plants. None of these fills the role that SK Innovation E&S fills for SK hynix. Samsung’s power solution at the national industrial complex will require external partnerships: KEPCO generation subsidiaries, independent power producers, or new entrants.

The long-term option Samsung is designing elsewhere

Samsung does not have an energy operator, but it has been building something else. Samsung C&T, the de facto holding company and largest shareholder of Samsung Electronics, has positioned itself across three SMR projects in Romania, Sweden, and Estonia, spanning two reactor designs (NuScale and GE Hitachi BWRX-300) with target dates ranging from 2032 to 2035. KEI analyzed the broader pattern in Issue #5: Korean companies are buying equity across multiple Western SMR designs as EPC positioning plays, not technology wagers. Samsung C&T fits that pattern, with one distinction. The Swedish project (an SMR campus co-located with data centers where power flows through direct PPAs) is the closest existing template to what on-site nuclear at a semiconductor complex might look like.

No law explicitly prohibits behind-the-meter nuclear generation in Korea, but no regulatory category for it exists either. A self-consumption reactor owned by a semiconductor manufacturer fits nowhere in the current licensing framework. Even if the political will materializes, establishing a new pathway through the Nuclear Safety and Security Commission and amending the Electric Utility Act would consume years. SMR is not a near-term answer; the timeline stretches a decade or more.

What the Samsung gap means for investors

SK Innovation E&S captures the gas supply, steam revenue, and operating role for the SK side of the cluster. Samsung has no equivalent, and is not standing still. In February 2026, industry sources reported that Samsung Electronics had begun discussions with E1 and LS Electric on an LNG CHP arrangement for the national complex, with E1 building and operating the plant and LS Electric supplying power equipment. E1 already supplies heat to Samsung’s Pyeongtaek semiconductor campus through a plant it acquired in 2024. No partnership has been formalized, and a planned meeting between the three companies’ top executives was postponed. But the contours are visible: Samsung is piecing together a coalition — one company for fuel, another for equipment, a third for grid integration. Where SK’s model is a closed loop, Samsung’s is a patchwork, and that patchwork has more entry points for outside investors.

Whoever partners with Samsung enters a relationship with one of the world’s largest semiconductor manufacturers as the anchor off-taker. That kind of deal does not come around often. And the partnership extends beyond LNG: Samsung needs 24/7 baseload power that is increasingly carbon-free under RE100 commitments and supply-chain pressure from Apple and Microsoft. LNG solves the first requirement. It does not solve the second. Samsung’s construction arm is investing in industrial nuclear EPC while its semiconductor arm faces a growing power deficit at Yongin. The group clearly sees where baseload power is heading. But no Korean regulatory pathway exists to get an SMR licensed for behind-the-meter industrial use, and building one could take a decade. Whoever Samsung partners with now for LNG will have an inside track when the decarbonization requirements eventually force a technology shift.

The regional pricing signal

The Distributed Energy Activation Special Act (분산에너지 활성화 특별법), effective since June 2024, authorizes regionally differentiated electricity tariffs. In early 2026, MCEE began commissioning research on wholesale market implementation, with results expected within the year. The likely framework splits the country into three zones: Seoul metropolitan area, non-metropolitan regions, and Jeju. Regions with high power self-sufficiency pay less. Gyeonggi Province (self-sufficiency rate: 62%) falls on the expensive side.

President Lee Jae-myung has repeatedly signaled the direction, most pointedly at a January 2026 press conference: “They say they will build nuclear plants and gas plants in Yongin — but how many can you actually build?” He did not endorse on-site nuclear. But the problem as he framed it points toward a conclusion he left unstated: Yongin cannot move, transmission faces social resistance, and LNG alone is insufficient. Power generation must move closer to consumption, and consuming power in the metropolitan area will carry a premium.

If LNG and CHP plants are actually built inside the cluster, though, they push Gyeonggi’s self-sufficiency ratio upward, which under the differentiation framework means a smaller tariff premium or, in the most favorable scenario, a net reduction relative to today’s uniform rate. Every megawatt of on-site generation that comes online does double duty: it secures supply reliability and it suppresses the OPEX impact of the very tariff regime designed to penalize metropolitan consumption. Companies that invest in on-site generation at Yongin are buying more than power. They are buying protection against a structural cost increase that competitors in other metropolitan locations will absorb in full.

The clean-power gap

Samsung Electronics joined RE100 in September 2022, targeting 100% renewable electricity by 2050. Its DS (semiconductor) division stands at 24.8% renewable sourcing. Korea-specific fab data is not disclosed. Major customers including Apple and Microsoft require carbon-free manufacturing supply chains by 2030, with concrete intermediate targets already in effect. None of those commitments have been formally withdrawn. But the global memory shortage appears to have neutralized them in practice. With HBM demand consuming wafer capacity through at least 2028 and conventional DRAM prices tripling since late 2024, the conversation around supplier clean-power compliance has gone quiet. No major customer is in a position to pressure a semiconductor supplier it cannot replace. The clean-power gap is real, but it is dormant for now — as long as chips remain scarce, no customer will condition procurement on carbon sourcing.

Yongin’s stage-one power plan puts 3GW of new LNG generation at the center of a cluster whose largest customers demand clean power. Samsung has begun securing Korean renewable PPAs: 115MW solar (20-year) and 254MW tidal (10-year) with K-water, roughly 620 GWh per year. Against eventual consumption, that barely registers — and TSMC Arizona, with 100% REC matching since 2023, makes Samsung’s story harder to tell. The gap widens if LNG plants are commissioned before a credible clean-power overlay is in place. That reckoning is deferred, not cancelled. When memory supply eventually normalizes, the customers who quietly shelved their clean-power timelines will likely reinstate them. Samsung’s position at that point will reflect whatever it built, or did not build, during the reprieve. SK hynix faces the same tension on a longer timeline; it too is an RE100 member. But if the clean-power conversation eventually leads to industrial nuclear, SK is better positioned than it might appear. The SK Group is TerraPower’s second-largest shareholder, and TerraPower received the first U.S. commercial SMR construction permit from the NRC in March 2026. SK is not pursuing SMR for Yongin today. But if RE100 compliance eventually demands carbon-free baseload at scale, the group will not be starting from scratch.

What this adds up to

The coal-replacement permits that made the LNG pipeline possible are under legal challenge. The PF pipeline runs into the trillions of won, and the deal structures are still being assembled. Most of the key partnerships will be locked in before 2028 — once CHP construction starts and Samsung’s first energy contracts are signed, the positions harden. Late entrants will find less to bid on.

Base case. The six GENCO units are expected to retain their coal-replacement permits and supply the bulk of Yongin’s stage-one capacity. Their advantage is structural: only coal retirement offsets can bypass the 2.5GW cap on net-new LNG, and no private developer holds that card. Private generation is likely to fill the remainder, but in different forms. On the SK side, the CHP joint venture with KOMIPO has a clear path forward — SK Innovation E&S has its own revenue logic in steam sales and LNG fuel supply that makes the JV structure viable regardless of wholesale power market conditions. On the Samsung side, the incentive is simpler: secure reliable power. Without an in-house energy affiliate that profits from heat or fuel, Samsung appears more likely to pursue a flexible arrangement (an off-take agreement, a build-operate-transfer model, or a multi-partner coalition) than a single vertically integrated JV.

What I’m watching.

Whether the Greenpeace lawsuit produces an injunction or preliminary ruling before GENCO construction begins. A procedural delay of even 12–18 months could shift the stage-one timeline and reopen the question of who fills the gap.

The structure of Samsung’s first formalized energy partnership. The E1/LS Electric discussions suggest a multi-partner model rather than a single JV — which would open more financing tranches to outside investors than SK’s closed ecosystem does. If Samsung instead signs an exclusive JV with one GENCO, that window narrows.

What would change my mind. If Samsung’s fab investment at Yongin slows materially (Fab 1 delayed beyond 2031), the power demand timeline stretches and the urgency behind every partnership, permit, and PF structure in this article recedes. The assets would still get built. The actionable window for investors would simply move further out.

What to Watch

Greenpeace lawsuit timeline. Any preliminary ruling on the same-location siting argument before GENCO construction begins.

Samsung power partnerships. Whether the reported E1/LS Electric discussions formalize — and whether additional partners join.

Samsung Group nuclear signals. Samsung C&T’s SMR projects are framed as export EPC. If any Samsung entity begins regulatory engagement with Korea’s nuclear safety authority on domestic SMR siting, licensing, or design certification, the timeline for a different power supply model at Yongin shortens from next decade to this one.

RE100 reconciliation. The memory shortage appears to have put customer clean-power pressure on hold — no commitments have been formally withdrawn, but the conversation has gone quiet. When supply normalizes and customers regain leverage over their semiconductor suppliers, Samsung’s DS division renewable rate of 24.8% and the absence of a Korea-specific disclosure become a visible vulnerability again. The timing depends less on Samsung’s RE100 roadmap than on when the memory cycle turns.

If this analysis is useful for your team’s Korea infrastructure or semiconductor strategy, consider forwarding it to a colleague.