The World's Largest Semiconductor Cluster Needs 15GW: Samsung, SK Hynix, and the Power They Don't Have

40% of Yongin's 15GW has no confirmed source. The official plan faces three structural obstacles.

DEEP DIVE | Image: Samsung Electronics via Korea.net

Opening

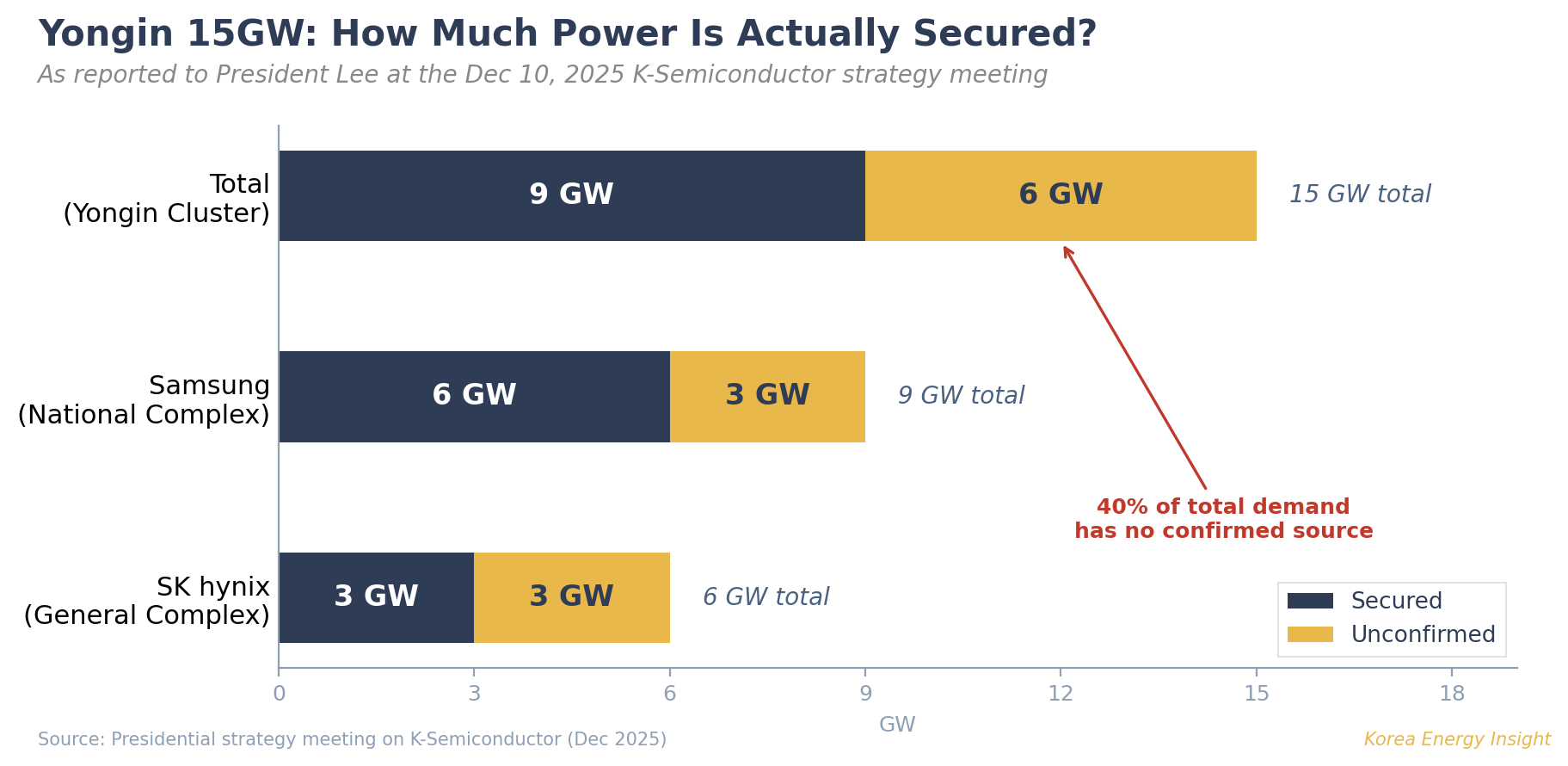

At a December 10, 2025 presidential strategy meeting on K-Semiconductor, Samsung reported that 6GW of the national industrial complex’s 9GW power requirement had been secured — but the remaining 3GW had no confirmed supply plan. SK hynix reported that only half of its 6GW had been arranged. Across both sites, 40% of the power needed to run the world’s largest semiconductor mega-cluster has no identified source.

These are not casual estimates. They are the power requirements the companies themselves presented to the government. Samsung and SK hynix together need 15GW to operate the fabs, clean rooms, and process steam systems planned for Yongin’s two industrial complexes — equivalent to ten large nuclear reactors. The cluster represents announced investment plans totaling up to $660 billion (KRW 960 trillion; all USD conversions at approximately KRW 1,450/USD). SK hynix broke ground on its first fab in February 2025 and targets equipment installation by the first half of 2027. Samsung’s national complex aims for initial fab operations by 2030.

By any measure, the Yongin semiconductor cluster is arguably the largest single industrial project in Korean history. The power supply plan behind it is not yet built to match.

Global Context

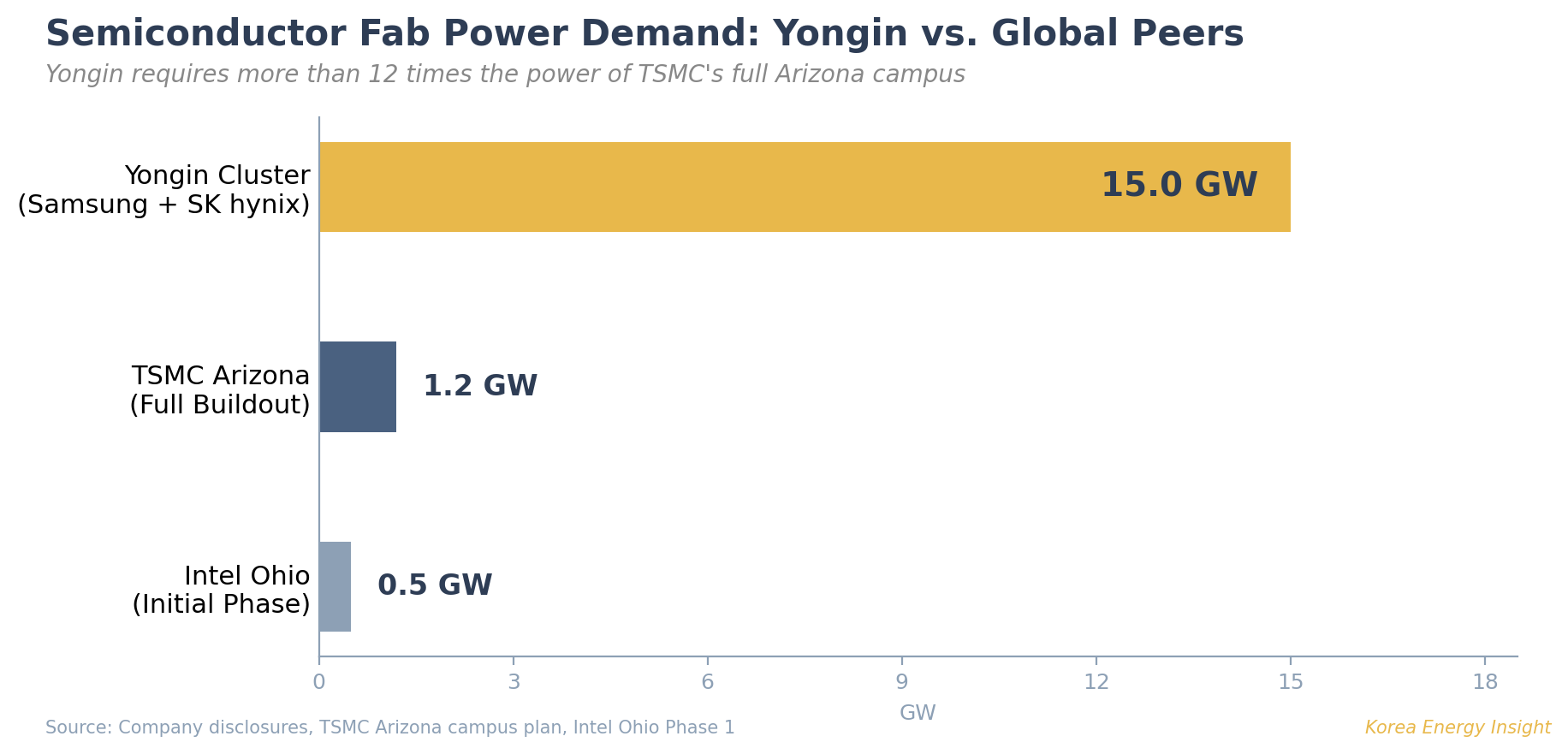

Advanced fabs consume enormous quantities of electricity, and no country’s grid was designed for them. TSMC’s Arizona campus — six fabs, two packaging facilities, and an R&D center — will draw approximately 1.2GW at full buildout. Intel’s Ohio complex is designed for up to 500MW in its initial phase. Yongin dwarfs both: 15GW is more than twelve times TSMC Arizona’s load.

The bigger difference is who ends up paying for the power infrastructure.

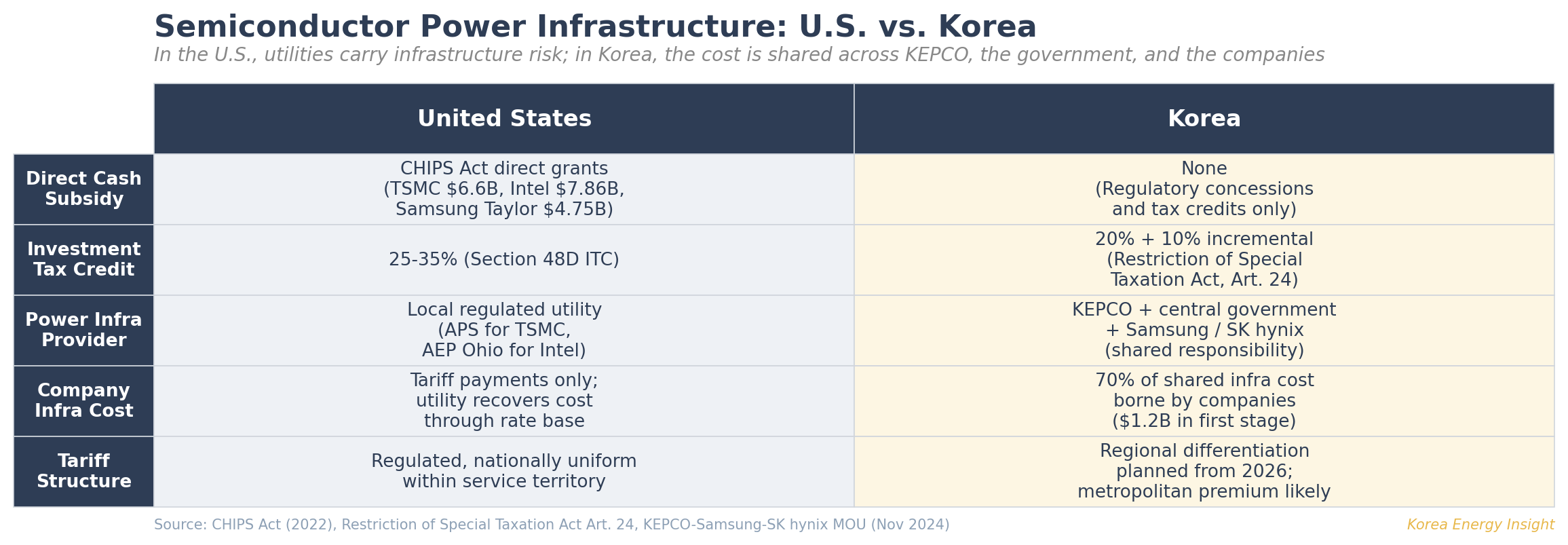

In the United States, the federal government writes checks. TSMC received $6.6 billion in direct CHIPS Act subsidies. Intel received $7.86 billion. Samsung’s Taylor, Texas facility was awarded $4.75 billion. On top of the cash, Section 48D of the U.S. tax code provides a 25% Advanced Manufacturing Investment Tax Credit, rising to 35% for property placed in service after 2025. The power infrastructure itself is handled by the local utility — Arizona Public Service (APS) serves TSMC under a regulated tariff framework, builds the substations, plans the generation, and layers in the transmission capacity. For Intel’s Ohio fab, AEP Ohio invested approximately $95 million in a dedicated substation. The semiconductor company pays a tariff; the utility does the heavy lifting.

Korea took a different path. There is no CHIPS Act equivalent — no federal cash award to Samsung or SK hynix for building in Yongin. Korea’s National Strategic Technology investment tax credit for semiconductors is 20% for large and mid-sized firms, with an additional 10% on incremental investment above the prior three-year average (조세특례제한법 제24조; those higher rates were legislated in March 2025). The Semiconductor Special Act (반도체산업 경쟁력 강화 및 지원에 관한 특별법), promulgated in February 2026 with an August 2026 effective date, is not a CHIPS-style direct grant statute — but it is more than a coordination framework. It establishes a presidential committee, a master plan, a special account, and a legal basis for infrastructure support including power, water, and roads.

What Korea offered instead of cash was something the U.S. did not need to provide: permission. The Yongin cluster sits in the Seoul metropolitan area, where large-scale industrial development had been restricted under national land-use regulations. The government relaxed metropolitan-area development restrictions, raised floor-area ratios from 350% to 490% under the National High-Tech Strategic Industry Act, and fast-tracked permitting — which is why SK hynix expanded its investment plan from $84 billion (KRW 122 trillion) to $414 billion (KRW 600 trillion). Access to talent, suppliers, and logistics in the metropolitan area was itself the most valuable concession.

Regulatory clearance solved the siting question. It did not solve the power question.

Korea Situation

The official plan and its three bottlenecks

The government’s power supply framework for Yongin operates at two levels. For the broader Yongin cluster, KEPCO plans 14 new 345kV transmission routes totaling 1,153 kilometers, connecting the Honam and East Coast generation regions to the metropolitan south. For Samsung’s national industrial complex specifically, three KEPCO generation subsidiaries — Korea East-West Power (EWP), Korea Southern Power (KOSPO), and Korea Western Power (KOWEPO) — will each build a 1GW LNG plant inside the complex, replacing retiring coal units at Dangjin, Hadong, and Taean respectively. Construction is slated to begin in December 2027, with a target of 3GW of firm generation by 2030. Additional supply from long-distance transmission and later-stage generation is planned through 2044.

None of these layers is moving smoothly.

The three LNG plants do not yet have confirmed sites. The 11th Basic Plan for Electricity Supply and Demand (confirmed February 2025) includes the 3GW of LNG generation for the national complex. However, public materials do not yet identify specific parcels within the complex where the plants will be built. Greenpeace Korea filed a separate administrative lawsuit against the LNG generation permits in July 2025; the first hearing was held in November 2025, and as of March 2026 the case remains pending. Under the Electric Utility Act’s implementing rules, generation permit applications require documented proof of site acquisition and layout plans (전기사업법 시행규칙 별표 1의2). Without confirmed sites, construction cannot legally begin.

More than half of all transmission projects are delayed. According to data KEPCO submitted to the National Assembly in October 2025, 30 of 54 transmission and substation projects included in the 11th Basic Plan (55%) are either delayed or expected to be delayed. For transmission lines alone, 14 of 29 projects (48%) are behind schedule. The causes are structural: resident opposition, compensation disputes, prolonged environmental assessment, and site acquisition difficulties. The track record reinforces the point — the Bukdangjin–Sintangjeong corridor took twelve years to complete; the Donghae Coast–Singapyeong line has been pushed back twice; the Dangjin Thermal–Sinsongsan line slipped by three years. All of these routes run toward the Seoul metropolitan area — the same destination as the Yongin cluster’s planned transmission links. Korea enacted the National Core Power Grid Expansion Special Act in March 2025, but the law cannot override the social conflicts that produce the delays.

KEPCO’s balance sheet constrains everything else. The 11th Long-Term Transmission and Substation Plan requires $50.2 billion (KRW 72.8 trillion) in grid investment through 2038 — 29% more than the previous plan. KEPCO’s total debt exceeds $138 billion (KRW 200 trillion). Annual interest payments alone approach $2.8 billion (KRW 4 trillion). The company accumulated approximately $30 billion (KRW 43 trillion) in operating losses over 2021–2023 before returning to operating profit in 2025 at $9.3 billion (KRW 13.5 trillion) — but that surplus covers a fraction of what the grid buildout demands. KEPCO says it will fund investment through “management efficiency, cost reduction, and appropriate electricity tariff operation.” That language signals upward pressure on tariffs — but Korea’s political economy has historically constrained KEPCO’s ability to raise prices. Electricity tariff adjustments require government approval and carry significant political cost; KEPCO’s stated intentions and actual tariff outcomes have often diverged.

President Lee has floated an alternative: a public participation fund (국민펀드) that would channel private savings into transmission infrastructure, offering guaranteed returns backed by grid usage fees. At a March 2026 cabinet meeting, Lee called grid investment “the safest investment there is” and questioned why KEPCO should take on more debt when the public could be invited to co-invest. The concept is politically appealing — it would ease KEPCO’s balance sheet while giving citizens a stake in national infrastructure. But as of early 2026, neither the fund structure, return mechanism, nor legal framework has been defined. The MCEE’s deputy minister acknowledged that “how to invest and how much still requires further deliberation.” It remains an idea, not a program.

The cost question

In November 2024, KEPCO, Samsung, and SK hynix signed a memorandum of understanding on the first-stage power infrastructure. Total first-stage transmission costs — lines connecting the public grid to the cluster plus substations inside it — are estimated at $2.6 billion (KRW 3.71 trillion). Of the $1.7 billion (KRW 2.4 trillion) in shared-infrastructure costs for the national and general complexes combined, the public side covers roughly 30% — $480 million (KRW 700 billion). Samsung and SK hynix bear 70% — $1.2 billion (KRW 1.7 trillion). The government separately pledged to absorb a “significant portion” of $1.2 billion (KRW 1.8 trillion) in underground cable conversion costs.

Both companies pushed back publicly. Their position, reported in Korean media: the United States, Japan, and China provide large-scale subsidies to attract semiconductor investment, while Korea asks companies to pay for transmission infrastructure. The eventual deal expanded public-funded common-use grid lines and reduced corporate dedicated-line obligations, cutting the companies’ costs by more than $700 million (KRW 1 trillion) from the initial estimate. The fundamental structure remains: Korean semiconductor companies co-fund power infrastructure in a way that TSMC and Intel do not.

Implications

The real gap with the U.S. is not subsidies — it is infrastructure risk

Korea’s 20% semiconductor investment tax credit compares with the U.S. CHIPS Act’s 25–35% ITC. The percentage gap matters less than the way each system allocates risk. In the United States, power infrastructure risk sits with the regulated utility. APS builds the substations, plans the generation, recovers costs through rate base — and the semiconductor company’s exposure is limited to a tariff. In Korea, infrastructure risk is distributed across KEPCO, the central government, and the companies themselves. When risk sits with multiple actors under different constraints — KEPCO under debt pressure, the government under political constraints on tariffs and land use, and corporations negotiating their share — the schedule depends less on engineering than on getting KEPCO, the government, and the companies to agree on who pays. That is why 55% of transmission projects are delayed.

Where Korean manufacturers build is about to cost differently

Industrial tariffs have risen 76% in under three years (from 105.5 won/kWh in early 2022 to 185.5 won/kWh by late 2024). KEPCO’s grid investment plan creates further upward pressure — though Korea’s political constraints on tariff-setting mean the pace and magnitude of any increase remain uncertain. What is more predictable is the direction: the Distributed Energy Activation Special Act (분산에너지 활성화 특별법, Article 45) authorizes regionally differentiated retail tariffs, and the government has indicated it will present the detailed design within 2026.

The groundwork is already being laid at the wholesale level. Korea’s wholesale electricity market has operated under a single national price (SMP) for over twenty years. The government initially planned to introduce regional wholesale pricing in the first half of 2025, but that effort stalled when critics pointed out it would expand KEPCO’s purchasing margin without passing savings to consumers. The current plan pursues wholesale and retail differentiation simultaneously — the research on the pricing design was due for completion by February 2026, with wholesale market implementation targeted within the year. Retail differentiation would follow, splitting the country into at least three zones: the Seoul metropolitan area, non-metropolitan regions, and Jeju — raising metropolitan costs relative to generation-rich regions. For Yongin, in Gyeonggi Province — whose power self-sufficiency fell from 62.4% in 2023 to 62.0% in 2024 and 59.1% in 2025 — both forces push the same way.

This is not just a semiconductor story. RE100 compliance is harder and more expensive to achieve in the Seoul metropolitan area, where local renewable generation is scarce and grid-delivered renewable electricity requires mechanisms such as Korea’s green premium tariff (녹색프리미엄) — all of which add cost. The economics are plain: metropolitan land prices make utility-scale renewable generation unviable. Yongin’s Cheoin-gu — where the semiconductor cluster sits — recorded the highest official land price increase in all of Gyeonggi Province in 2025 (4.11%), driven by the cluster itself. Virtually no solar developer can close a project on land valued at metropolitan rates. Any renewable electricity consumed at Yongin must be procured from distant regions and delivered through the grid or purchased as certificates — each adding cost layers that competitors in generation-rich locations avoid.

For any LP or institutional investor modeling a Korean manufacturing investment, location-dependent electricity tariff differentials deserve a place in sensitivity analysis. Most have not run this scenario — partly because the policy details remain undefined, partly because the very concept of regional electricity pricing in Korea was outside the frame of reference until recently. That assumption is expiring.

Companies are already responding. Hyundai Motor chose Saemangeum — a reclaimed coastal zone built behind the world’s longest seawall (33.9 km), approximately 270 kilometers south of Seoul — for its $6.1 billion (KRW 8.9 trillion) robotics factory. The site is no accident: Saemangeum is planning a 2.1GW floating solar complex, the world’s largest, with a 1.2GW first phase targeting commercial operation by 2029. Hyundai’s own investment includes a GW-scale solar facility and a hydrogen plant — an integrated clean-energy supply chain that would be physically impossible to replicate at metropolitan land prices. Lower power costs, abundant renewable generation, and infrastructure availability were among the factors.

If regional tariff differentiation is implemented as designed, the incentive to site energy-intensive operations in generation-rich regions becomes a lasting one rather than a tactical bet. Whether Hyundai’s choice turns out to be an early signal or a one-off will say a lot about how Korean manufacturing reorganizes over the next decade.

But infrastructure will arrive

This is not a crisis story. Korea’s industrial history offers no precedent for a national-scale manufacturing project failing because infrastructure did not follow. POSCO’s steel mill at Pohang — now the world’s sixth-largest steelmaker by output — was built when per capita income was below $200 and the World Bank refused to fund it. The semiconductor fabs of the 1980s were powered through a grid that was still being stabilized. For Yongin, the government is boring a 47-kilometer dedicated water pipeline from Paldang Dam through mountainous terrain — a $1.5 billion (KRW 2.2 trillion) project that will deliver 1.07 million tons per day. A 5.2-kilometer underground power tunnel for the SK hynix general complex was completed in October 2024, drilled through in just over two years.

Ask anyone who has worked on Korean industrial infrastructure and the answer is the same: the plants will be built. That has been Korea’s pattern in large industrial projects, and no one in the industry expects Yongin to break it. Fifteen gigawatts will be built one way or another. The harder question is whether Korea can keep a 15GW metropolitan semiconductor cluster running under legacy tariff assumptions and legacy cost-allocation rules. That is the deeper structural question, and Part 2 will examine the supply models already moving to answer it.

What to Watch

LNG site designation. If the three LNG plants inside the national industrial complex do not have confirmed parcels by mid-2026, the December 2027 construction start becomes unreachable — delaying the first 3GW of firm generation past 2030 and compressing the timeline against Samsung’s initial fab operations.

Regional tariff design. Article 45 of the Distributed Energy Activation Special Act authorizes regionally differentiated tariffs. The Ministry of Climate, Energy and Environment (MCEE, formerly MOTIE) has signaled it will present the design within 2026. Watch for the scope of metropolitan-area surcharges, any exemptions for strategic industries, and corporate responses — additional on-site generation plans, relocation of non-fab operations, or lobbying for carve-outs.

KEPCO investment pace. The $50 billion (KRW 72.8 trillion) grid plan depends on a company with over $138 billion (KRW 200 trillion) in debt and approximately $30 billion (KRW 43 trillion) in recently accumulated losses. Watch for tariff adjustment announcements, bond issuance volumes, and any signs that transmission projects are being deprioritized or deferred beyond their already-delayed schedules.

In the next issue, KEI will examine the power supply models already moving outside the official plan — from CHP joint ventures and self-consumption generation to the long-term SMR option that Samsung is designing overseas.

If this analysis is useful for your team’s Korea infrastructure or semiconductor strategy, consider forwarding it to a colleague.