The SMR Puzzle: Why Korea's Builders Are Betting on Everyone Else's Reactor

Seven firms, six reactor designs, zero of their own

DEEP DIVE

NuScale’s Idaho SMR project started at roughly $5,000/kW in 2020. By 2023, the estimate had reached $9.3 billion for 462 MWe — $20,130/kW — and the project was cancelled. Korea’s major nuclear builders, manufacturers, and energy companies are investing in SMR vendors anyway. Not in NuScale alone — across at least six Western designs, with equity stakes that did not exist four years ago. The pattern is not a technology bet. It looks more like a response to constraints that most SMR pitch decks do not address. (IEEFA, 2023; NuScale/UAMPS joint release, November 2023)

The Economics That Pitch Decks Skip

Every SMR vendor targets construction costs below $5,000/kW once modules are mass-produced. The first-of-a-kind (FOAK) reality is three to four times higher. Ontario Power Generation’s Darlington BWRX-300, the Western world’s most advanced SMR project, carries a first-unit reported total project cost of $4.5 billion (C$6.1 billion) for 300 MWe — over $14,600/kW before shared infrastructure. Korea’s own i-SMR targets $3,500/kW, but no unit has been built. NuScale also started at $5,000/kW. For reference, Korea built four APR1400 units at UAE’s Barakah for approximately $3,600/kW on the original contract value. These figures are not directly comparable — they mix contract prices, total project costs, and different scopes — but the order-of-magnitude gap between SMR FOAK costs and large-reactor benchmarks is real. (OPG project page, 2025; KEPCO (Korea Electric Power Corporation) E&C brochure; ENEC/Reuters)

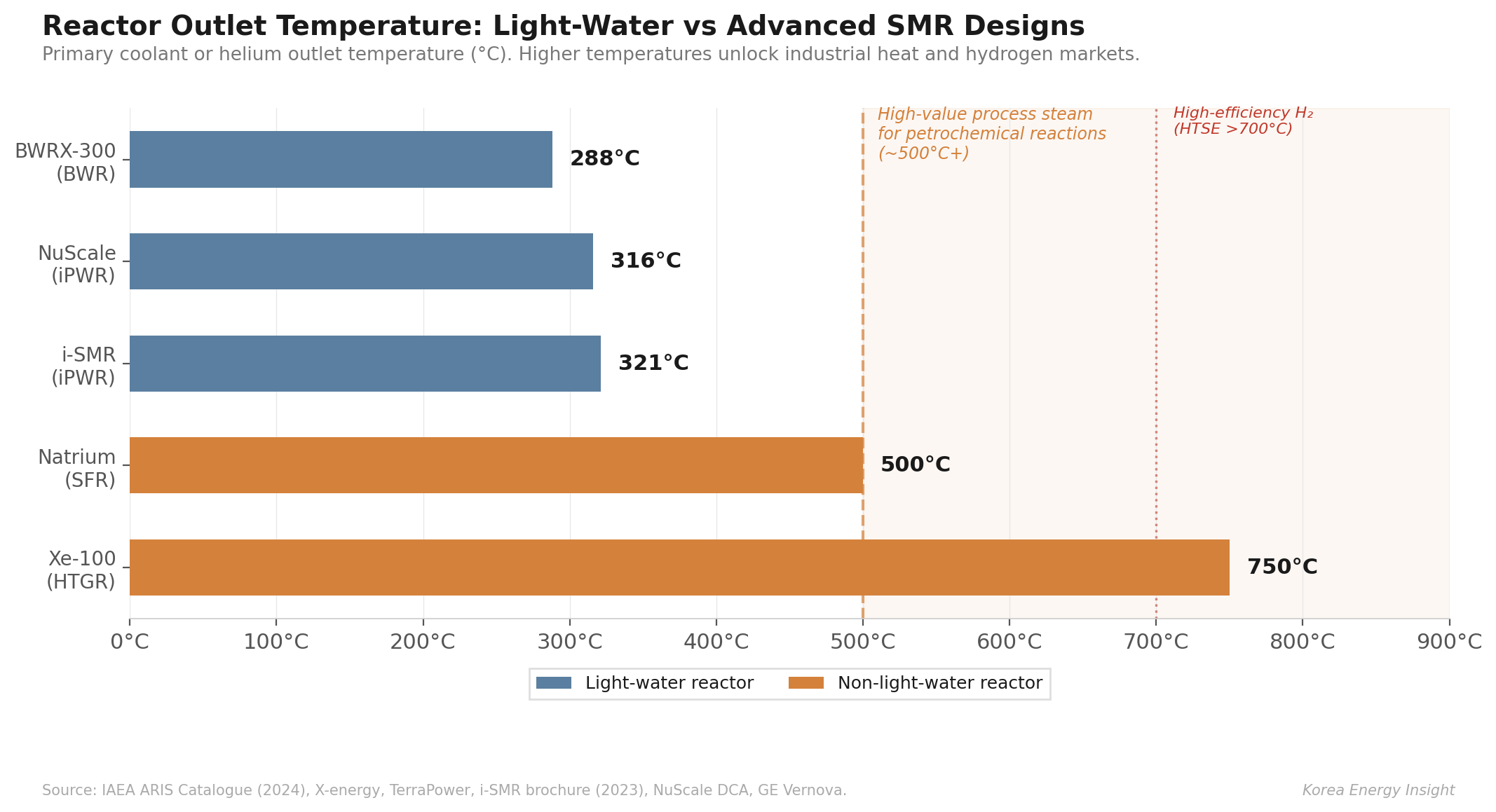

FOAK costs are always high. The question is whether the economics can close — and that depends on what an SMR can do beyond generating electricity. A large reactor already generates electricity at a fraction of the cost per kilowatt-hour. At $15,000–20,000/kW, an SMR needs additional value paths to justify the premium: high-temperature process heat, efficient hydrogen production, or flexible grid operations. Korea’s i-SMR — a 170 MWe pressurized water reactor with a primary coolant outlet temperature of 321°C — is poorly positioned for the first two, and can offer the third only with meaningful operating penalties.

What i-SMR’s 321°C Cannot Reach

The value paths that could justify a $15,000–20,000/kW premium — high-temperature industrial heat, efficient hydrogen production — require temperatures that light-water physics cannot deliver. High-value process steam for petrochemical high-temperature reactions runs above 500°C, and applications like steelmaking and cement demand 700°C or more. High-temperature steam electrolysis reaches system efficiencies above 90% at 850°C. Korea’s i-SMR operates at 321°C. NuScale reaches 316°C. X-energy’s Xe-100, a high-temperature gas reactor, produces helium at 750°C. TerraPower’s Natrium, a sodium-cooled fast reactor, operates above 350°C with integrated molten salt storage. That temperature gap determines whether an SMR can sell into higher-value heat and hydrogen markets or stay limited to power generation. (IAEA ARIS Catalogue, 2024; X-energy; TerraPower; DOE electrolysis targets)

Grid flexibility is equally constrained. As renewable penetration grows, grids need fast-response resources — what Korea’s grid operator KPX (Korea Power Exchange) calls “ultra-fast-responding resources” (초속응성 자원) — at response speeds that nuclear reactors, regardless of size, cannot match. A gas turbine can reach full output within minutes. A light-water reactor cannot. France has operated large PWRs in load-following mode for decades, cycling between 30% and 100% power, and Korea’s i-SMR targets the same range. But xenon-135 buildup, boron adjustment delays, and thermal cycling fatigue impose real operating penalties. NuScale bypasses these by running at full power and diverting steam to the condenser — at $20,000/kW, discarding output to follow load is an expensive form of flexibility. (SNETP factsheet, 2021; i-SMR brochure, 2023; NuScale technical publication, 2025)

Light-water reactors also face inherent disadvantages in fuel utilization. Their thermal neutron spectrum converts only a small fraction of U-238 into fissile material. Fast reactors can, if commercially proven, extract far more energy from the same fuel and burn long-lived actinides that light-water designs leave behind as waste. At $15,000–20,000/kW construction cost, adding a fuel and waste economics disadvantage widens the total cost-of-ownership gap further.

Korean firms are not backing these vendors because light-water SMRs have solved their economics. They are buying access to projects they may not be able to lead with their own design.

Where Light-Water SMRs Might Work

None of these limitations make light-water SMRs useless. They narrow the economically viable use case to one: dedicated, 24/7 carbon-free power for a buyer willing to pay a premium over wholesale market prices.

The economics are straightforward. As renewable penetration grows globally, marginal wholesale electricity prices will decline — Korea’s own SMP (System Marginal Price, the wholesale market clearing price) trajectory confirms this. An SMR with an LCOE near 180 won/kWh ($130/MWh) cannot compete in a wholesale market where solar drives marginal costs toward zero. But a data center that needs uninterrupted carbon-free power operates outside that market logic. Microsoft, Google, and Amazon are exploring both large reactors and SMRs for dedicated behind-the-meter supply in the United States. The economics of light-water SMRs may ultimately depend not on construction cost per kilowatt, but on what corporate buyers will pay for 24/7 zero-carbon electrons. Korea’s SMP zero-price hours — 26 confirmed since January 2025 — are an early signal of the same dynamic.

That still leaves Korea’s main problem: even if the use case exists, can it bring its own reactor design to that market?

Why Korean Builders, and Why Now

The global SMR pipeline has a bottleneck that has nothing to do with reactor design: who can build these plants. Vogtle 3 and 4 finished seven to eight years late at ~$15,000/kW; Westinghouse went bankrupt mid-project. Hinkley Point C is years behind at £35 billion. Japan has not completed a new-build since Fukushima. China builds abroad but cannot access Western markets. In the Western-aligned world, Korea’s Barakah record — four APR1400 units delivered between 2012 and 2024 at a competitive cost — stands alone. The “on time, on budget” narrative around Barakah is not perfectly precise — early units faced delays against original targets — but in an industry where Vogtle and Hinkley define the norm, Korea’s delivery record is the strongest marketing asset any nuclear EPC can claim. It helped win the Czech Dukovany contract and remains central to every Korean export pitch. (AP News, 2024; EDF 2025 results)

Domestically, Shin Hanul 3 and 4 are under contract and the 11th Basic Plan adds two more units targeting 2037–2038. Korea’s EPC contractors see large-reactor pipelines as their core business. SMR is additive. The capacity exists, and the contractors know their position is rare.

But Korea cannot freely export its own reactor design. The constraint is regulatory and institutional. APR1400 descends from Combustion Engineering’s System 80+ design, which Westinghouse acquired in 2000. Because APR1400 incorporates US-origin technology, any export to a third country requires DOE Part 810 authorization for technology transfer and NRC Part 110 approval for physical equipment export. The critical bottleneck is Part 810: under US law, only a US person — in practice, Westinghouse — can file the application. KHNP (Korea Hydro & Nuclear Power) cannot submit it alone. If Westinghouse declines or delays filing, the export process cannot proceed. This gives Westinghouse powerful practical leverage over Korean reactor exports where US-origin technology is implicated.

In a publicly broadcast presidential briefing on December 17, 2025, President Lee Jae-myung asked whether Westinghouse’s intellectual property claims should have expired after 25 years of Korean development. MOTIE (Ministry of Trade, Industry and Energy) Minister Kim Jeong-gwan responded that trade secrets carry no statutory time limit. The exchange confirmed, at the highest level of Korean government, that Westinghouse’s IP position remains legally valid and that the settlement reached in January 2025 was a necessary accommodation — not a resolution of the underlying dependency. (MBC/News1, December 17, 2025)

The settlement’s commercial terms are officially confidential but have been widely reported in Korean media. According to multiple outlets, each future reactor export would require KHNP and KEPCO to purchase approximately $650 million in goods and services from Westinghouse and pay roughly $175 million in technology licensing fees — reported figures totaling over $800 million per unit, under a 50-year agreement. Korean media also reported that independently developed next-generation reactors, including SMRs, must pass a Westinghouse IP non-infringement verification before export. These figures have not been officially confirmed by either party. The current Korean government has initiated a review of the agreement, with MOTIE pledging to report findings to the National Assembly. (MBC, August 2025; Financial News, September 2025; Seoul Shinmun, October 2025)

The settlement’s market-access implications have also become clearer. KHNP signed the Dukovany contract with the Czech Republic in June 2025 — a deal predating the settlement. But reporting in August 2025 indicated that the agreement restricts KEPCO from bidding on other projects in the United States and Europe — a claim consistent with the post-settlement pattern but not officially confirmed. Westinghouse launched its AP300 — a 300 MWe light-water SMR scaled from the AP1000 — and signed an $80 billion strategic partnership with the US government in October 2025. Where Westinghouse competes, APR1400 faces what appears to be a contractual barrier to entry. Where Westinghouse cooperates, the reported terms suggest projects may be steered toward AP1000, with Korean firms potentially serving in a subcontractor capacity rather than as prime contractor. (NEI Magazine, March 2026; Westinghouse/Brookfield announcement, October 2025)

Korea’s i-SMR does not clearly escape this framework. Technically, i-SMR descends from the SMART reactor lineage — a separate design family from APR1400/System 80+, developed by KAERI (Korea Atomic Energy Research Institute) since 1997. KHNP submitted the standard design approval application to Korea’s NSSC (Nuclear Safety and Security Commission) in February 2026. But US export control law does not distinguish by reactor size. Under Part 810 and EAR, any reactor that incorporates US-origin intellectual property, engineering tools, or technical support falls under the same control framework. And the reported settlement terms explicitly require IP non-infringement verification for next-generation Korean reactors, including SMRs, before export. The SMART lineage is technically distinct from System 80+. Whether that distinction survives a Westinghouse verification process is untested.

In practice, Korea has the Western world’s most demonstrated nuclear construction capability, but no reactor design whose export is free from US regulatory gatekeeping.

The Multi-Vendor Strategy

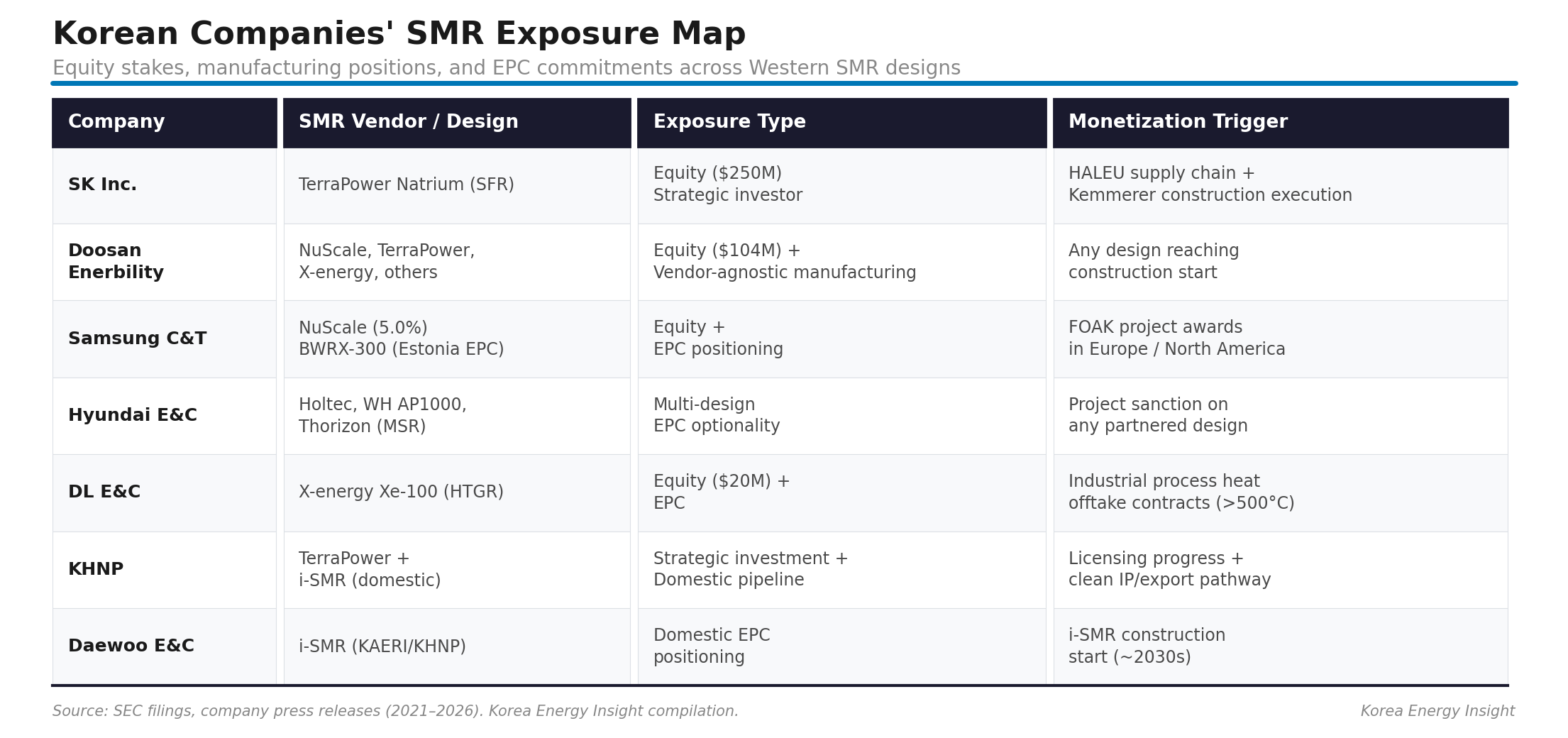

Korean builders, manufacturers, and energy companies have responded with a strategy unprecedented in the country’s nuclear history. Rather than backing a single design, they are positioning across the entire Western SMR field — and putting equity behind it.

The bet is not that any particular SMR design will dominate the merchant power market. It is that whichever design reaches construction, the companies that supply components, execute EPC work, and manage nuclear-grade quality assurance will earn revenue — especially on government-backed FOAK projects where policy financing absorbs the plant-level economics. Here, equity does more than provide capital — it secures a place inside the vendor-led consortium. EPC contracts alone do not guarantee a seat at the table when project teams form.

The roles are distinct. SK’s $250 million in TerraPower targets sodium-cooled fast reactors with DOE backing. Doosan Enerbility holds a vendor-agnostic position: as a manufacturer of reactor pressure vessels, steam generators, and heavy forgings, it supplies components to NuScale ($104 million invested), TerraPower, and others — whichever design builds first, Doosan’s order book fills. Samsung C&T (NuScale 5.0%, plus BWRX-300 EPC positioning in Estonia) and Hyundai E&C (Holtec, Westinghouse AP1000, and Thorizon’s molten salt reactor as of March 2026) are playing the EPC angle. DL E&C’s $20 million in X-energy targets the one SMR category where process heat creates a genuine economic differentiator. KHNP joined TerraPower’s investor base in January 2026. Daewoo E&C is securing its position in the only Korean-designed SMR pipeline through the domestic i-SMR program. (SEC filings; company press releases, 2021–2026)

But vendor risk is real. NuScale’s UAMPS cancellation destroyed $9.3 billion in projected value overnight. Korean investors — Doosan, Samsung, GS Energy — still hold their positions, but the commercial pipeline has not recovered. TerraPower received NRC construction permit approval for Kemmerer on March 4, 2026 — a milestone. Yet HALEU fuel supply remains unresolved. DOE acknowledged in August 2025 that domestic commercial HALEU is not available at scale. A construction permit without fuel is a regulatory achievement, not a commercial one. (TerraPower NRC announcement, March 2026; DOE HALEU statement, August 2025)

Implications for SMR Project Evaluation

Three points for anyone evaluating SMR investments or partnerships.

First, separate plant economics from supplier economics. An SMR project may struggle to compete on wholesale electricity price — but the EPC contractors, component manufacturers, and quality assurance providers that build it can earn revenue regardless, especially on government-backed FOAK projects where policy financing absorbs the plant-level risk. Korean firms’ multi-vendor positioning is not a bet on any single reactor’s commercial success. It is an option on construction activity itself. Check the EPC line, not just the reactor design: a credible nuclear-grade builder reduces completion risk, which improves project bankability. Korean EPC participation is becoming a de facto signal of execution credibility.

Second, understand the regulatory gatekeeping. The January 2025 settlement resolved the legal dispute between Westinghouse and KEPCO, but it did not eliminate the underlying regulatory dependency. Under US law, exporting any reactor containing US-origin technology requires a Part 810 filing by a US person. The reported settlement terms extend this framework to next-generation Korean designs, including SMRs. The competitive map is not defined by technology — it is defined by who holds the export-control key.

Third, distinguish between light-water and non-light-water SMR value paths. A 320°C reactor competing on electricity alone faces a challenging value proposition against large nuclear and falling renewable costs. The FOAK cost premium is more defensible where higher outlet temperatures open process heat, hydrogen, or industrial cogeneration markets — applications that light-water physics cannot reach.

What to Watch

Darlington BWRX-300 construction cost. If AtkinsRéalis and Aecon deliver near the $4.5 billion (C$6.1 billion) target, FOAK cost credibility improves for all SMR designs and Korean EPC value as a de-risking partner rises. If costs escalate toward NuScale territory, the learning-curve thesis weakens — and the case for light-water SMRs narrows further to behind-the-meter buyers willing to pay above wholesale.

TerraPower HALEU fuel pathway. The NRC construction permit is secured. Until a commercial-scale domestic HALEU supply chain is proven, Korean suppliers’ exposure to Natrium remains an option on future construction — not a near-term revenue stream. Centrus delivered 900 kg in 2025; Kemmerer needs orders of magnitude more.

i-SMR standard design approval. NSSC accepted the application in February 2026. Domestic licensing progress on the 2028 timeline is a positive signal, but export monetization remains constrained until the Westinghouse IP verification pathway is tested. A clean pass would materially widen i-SMR’s addressable market.

Westinghouse settlement review. The current Korean government has ordered a review of the January 2025 agreement. If renegotiation loosens the reported restrictions on independent bidding, Korean prime-contractor upside in third-country markets improves materially — for large reactors and SMRs alike.

The global SMR race is widely framed as a technology competition — which design is safest, most efficient, most innovative. From inside Korea’s nuclear industry, the view is different. The binding constraint is not the reactor. It is who can build it, who owns the underlying IP, and who holds the regulatory key to export. Korea has answered the first question decisively. The second and third are held by Westinghouse — and that single fact explains why seven Korean companies are investing in everyone else’s reactor.

If this analysis is useful for your team’s SMR evaluation, consider forwarding it to colleagues. Korea Energy Insight publishes Deep Dives and Market Signals on Korea’s power market, energy policy, and the commercial logic behind major energy investments.