The Cap Table Reveal: What Korea's First Domestic Offshore Wind PF Tells You About How These Deals Are Built

38% policy capital, contract margins to one foreign OEM, and a sponsor lineup rebuilt over seven years.

MARKET SIGNAL

The Financial Services Commission and the Ministry of Climate, Energy and Environment announced the financial close of Sinan-Wooi on April 9, 2026, describing it as Korea’s first large-scale (390 MW) offshore wind project financed with “purely domestic capital.” $2.34 billion (KRW 3.4 trillion; all USD conversions at approximately KRW 1,450/USD), after a seven-year stall. Read the press release before the headline.

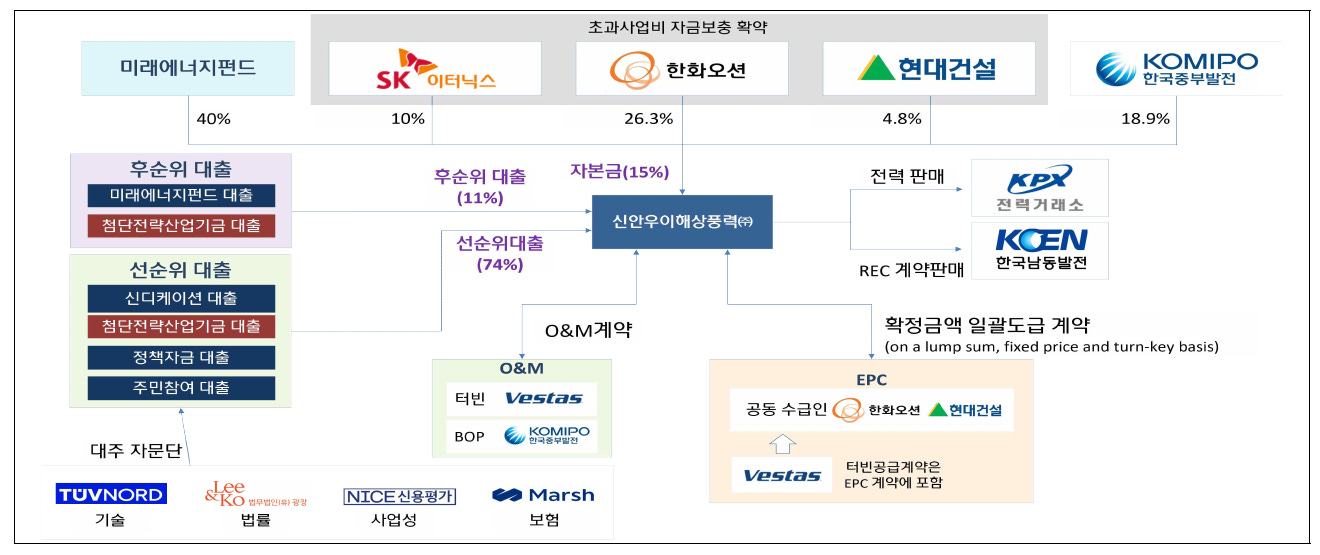

The release discloses senior and subordinated tranche sizes and ratios, identifies an 18-institution senior lending group, and maps the project’s equity, debt, and contract structure in unusual detail. It identifies Hanwha Ocean and Hyundai E&C as joint EPC contractors on a lump-sum, fixed-price, turn-key basis, and Korea Midland Power as BOP O&M contractor. Trade press later filled in contract details the release itself does not name. Hanwha Ocean holds a $1.36 billion (KRW 1.97 trillion) lead share of the $1.82 billion (KRW 2.64 trillion) combined EPC scope, with foundation fabrication subcontracted to Hyundai Steel Industries (a Hyundai E&C subsidiary).

The structure diagram goes one step further. It shows, in a separate annotation, that Vestas turbines are procured inside Hanwha Ocean’s EPC scope, while the turbine service agreement is contracted directly between Vestas and the SPC. Sinan-Wooi adopted a full-wrap EPC for turbine supply. It carved turbine service out into a separate SPC–OEM contract. That allocation — and the fact that the government diagram shows it — is the contracting-strategy reveal.

That last detail is a contracting strategy disclosure. Large offshore wind sponsors choose between two turbine procurement structures. A full-wrap EPC gives a single contractor single-point responsibility including turbines, at higher cost but lower interface burden on the SPC. An unbundled multi-contract structure has the SPC procure turbines directly from the OEM, transferring interface risk in exchange for a cheaper price. Both structures coexist in modern offshore wind PF, and the choice reflects sponsor risk appetite, OEM bargaining position, and market conditions at the time of contracting. Korean offshore wind has seen both.

Sinan-Wooi disclosed both that it adopted the full-wrap structure and that the wrap is centered on Hanwha Ocean rather than the OEM. Which procurement structure won is competitive intelligence in commercial PF. It reveals the sponsors’ risk appetite, exposes the EPC contractor’s negotiating position with the OEM, and becomes a benchmark that competing OEMs and EPC contractors use against the sponsors in the next deal.

Subordinated tranche ratios, lender exposure splits, and EPC contracting structures are protected information in commercial PF. They are not press release material. The fact that all of it appears in a Korean government structure diagram is itself the first evidence about what kind of transaction this is.

The Capital Stack

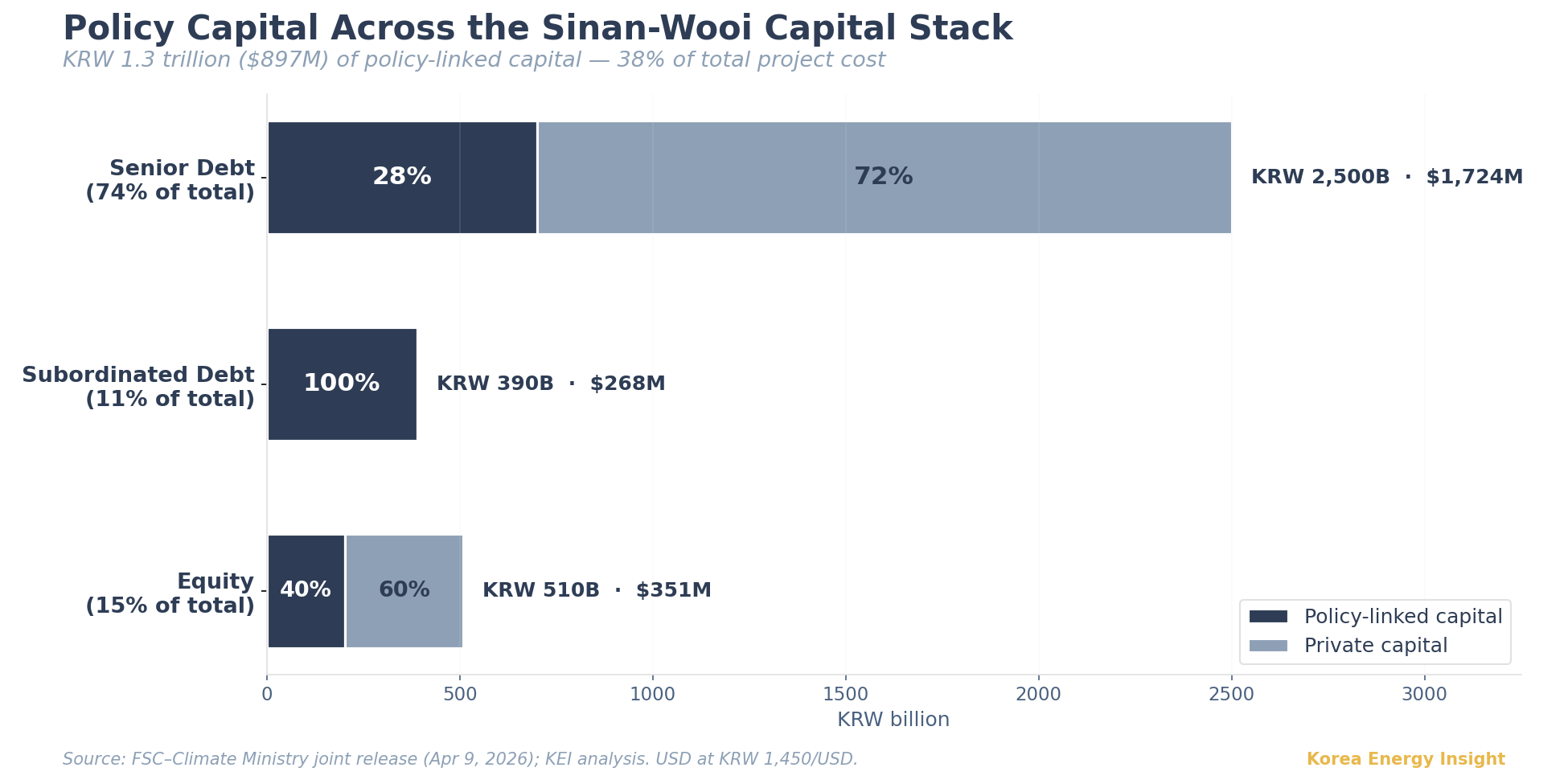

The subordinated tranche is the next signal. $269 million (KRW 390 billion), approximately 11% of total project cost. Public sponsor disclosures of large offshore wind PFs typically emphasize senior debt, and separately disclosed subordinated tranches at this scale rarely appear in those disclosures. A sub-debt layer of this size on a first-of-kind project signals that senior lenders demanded an unusually large cushion before signing. The entire layer is policy capital. Zero private participation.

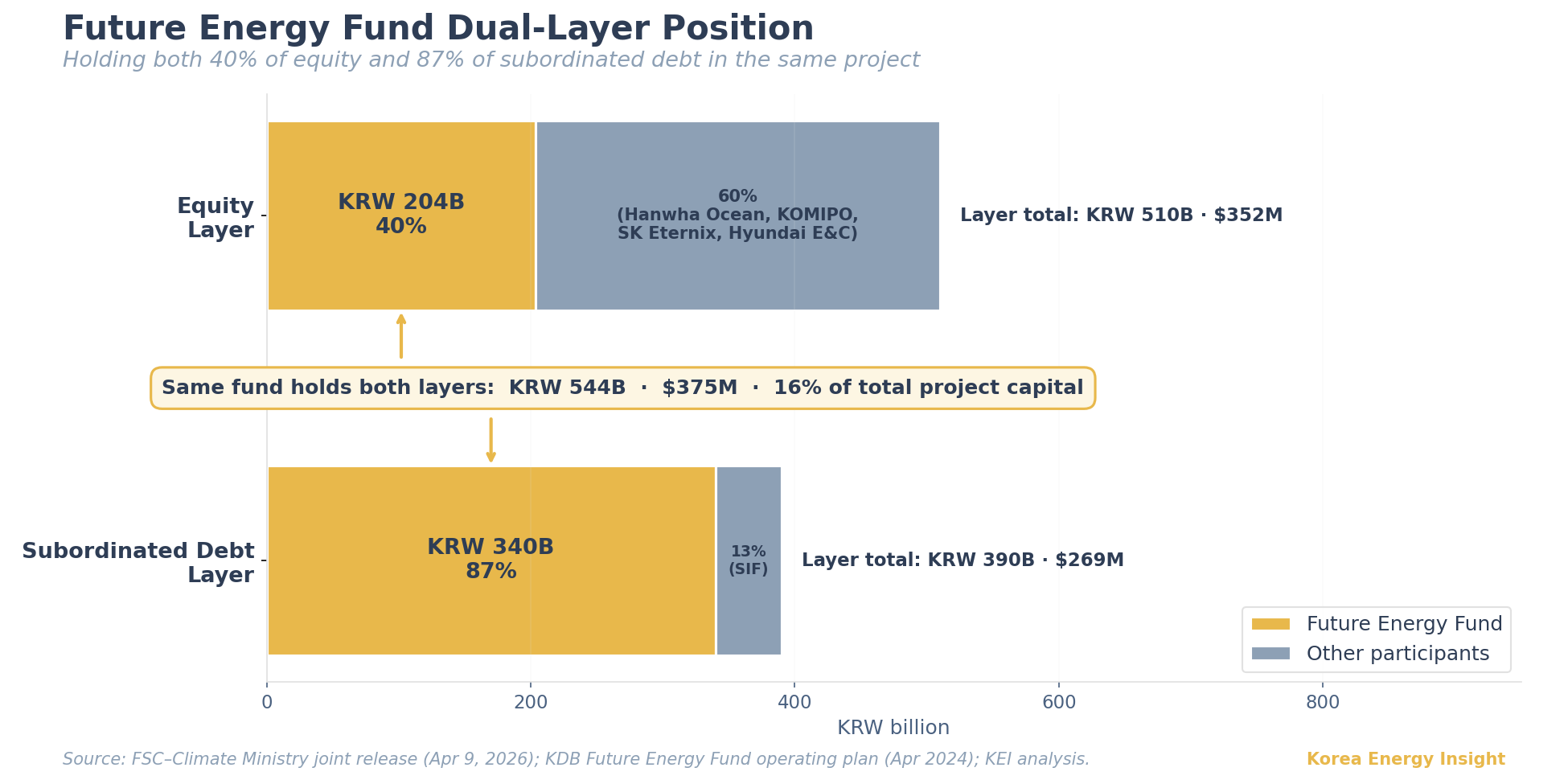

The composition of that policy layer matters more than the size. Future Energy Fund holds 40% of project equity ($141 million / KRW 204 billion) AND roughly 87% of the subordinated debt ($234 million / KRW 340 billion). Same fund, both layers, same project.

Future Energy Fund’s equity claims push toward residual-value maximization while its sub-debt claims require senior repayment ahead of equity dividends. Holding both a large equity position and most of the junior debt blurs the usual separation between residual-value maximization and junior-credit discipline. In a purely commercial structure, that overlap would normally raise governance and incentive questions. Sinan-Wooi closed with it anyway, which is itself a strong signal of policy intent.

The remaining 13% of sub-debt comes from the Strategic Industry Fund. Adding the Strategic Industry Fund’s $483 million (KRW 700 billion) senior tranche contribution, total policy-linked capital across equity, subordinated debt, and senior debt reaches roughly $897 million (KRW 1.3 trillion), or approximately 38% of project cost. The Strategic Industry Fund’s $517 million (KRW 750 billion) total commitment was approved by its operating committee on January 29, 2026, ten weeks before April 9 — the consummation, not the decision point.

Future Energy Fund is better understood as policy-structured capital than as purely private capital. It is a $6.21 billion (KRW 9 trillion) blind pool led by Korea Development Bank with five major Korean commercial banking groups as LPs, mandated to deploy into domestic renewables. The fund’s operating plan, published by KDB in April 2024, states the explicit mechanism: KDB’s anchor 20% LP position in each sub-fund allows participating commercial banks to apply a 100% risk weight to their investments instead of the standard 400%.

The Strategic Industry Fund, launched in March 2025, applies the same logic through a different channel. Its operating guidelines apply 100% RWA treatment to commercial bank exposures when policy capital provides cushion through a same-rank ~20% participation, a junior ~7.4% cushion, or a combination. Sinan-Wooi’s Strategic Industry Fund senior contribution of $483 million (KRW 700 billion) equals 28% of the senior tranche, meeting the same-rank threshold by a wide margin. The eighteen senior lenders sit on a cushion built explicitly to make their participation regulatorily affordable. The economic substance is publicly orchestrated risk-taking. The accounting form is private bank lending. Which is also why the structure diagram could be published at all — terms that a commercial sponsor would protect become public material in a state-orchestrated deal.

Related-Party Contract Concentration

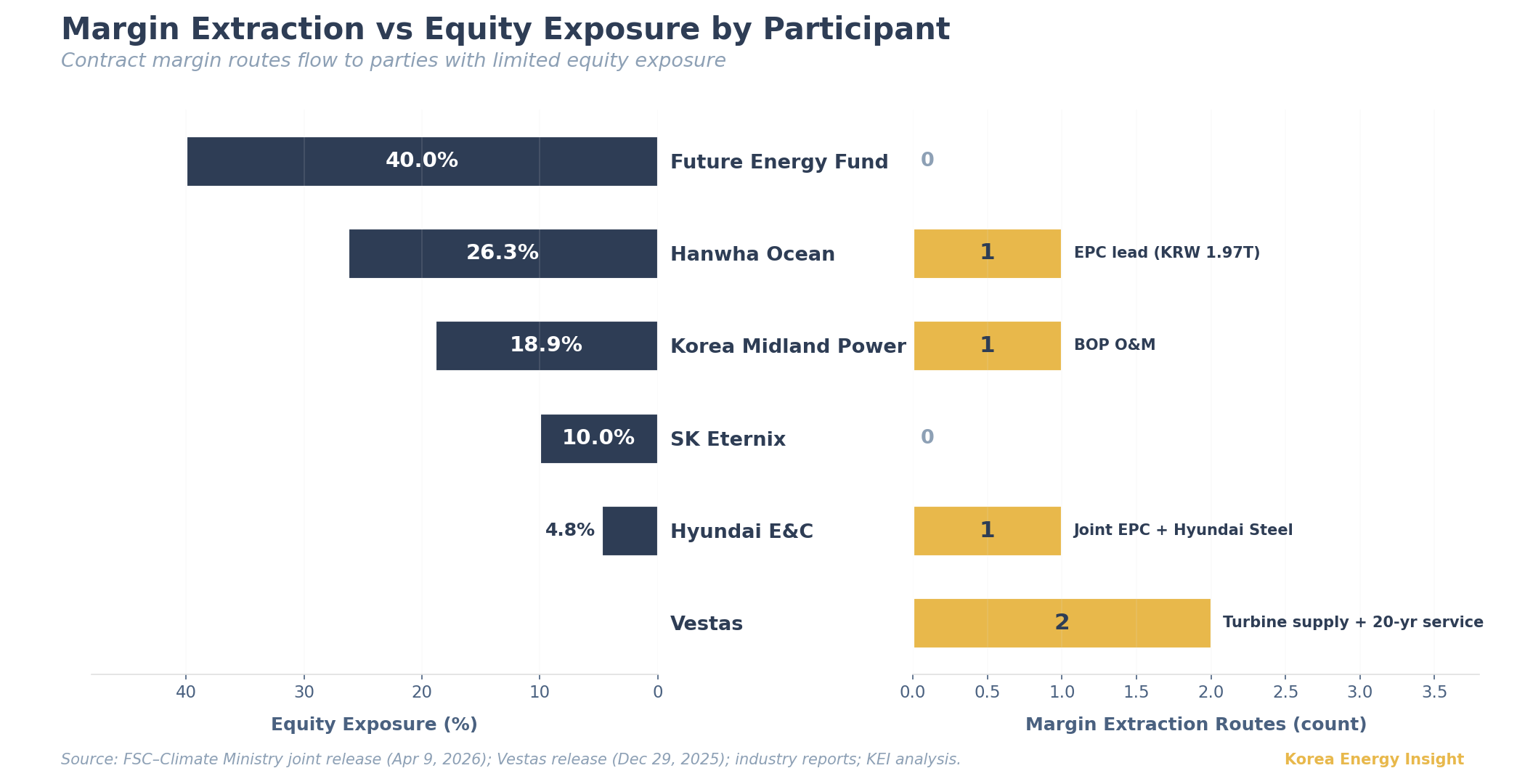

The SPC’s contract counterparties consist substantially of its own equity holders. Hanwha Ocean holds 26.3% sponsor equity and the lead EPC contract at $1.36 billion (KRW 1.97 trillion) out of the $1.82 billion (KRW 2.64 trillion) combined EPC value. Hyundai E&C holds 4.8% sponsor equity and the joint EPC contract, with foundation fabrication subcontracted to Hyundai Steel Industries, its subsidiary. Korea Midland Power holds 18.9% sponsor equity and the BOP O&M contract.

Vestas does not appear on the cap table at all but extracts margin on two routes in this project: once on the turbine supply embedded inside the EPC wrap, and again on a 20-year turbine service agreement contracted directly with the SPC. The turbine supply margin sits inside Hanwha Ocean’s EPC scope and carries no Vestas downside exposure. The service agreement margin is a different question. Its risk allocation between Vestas and the SPC depends on contract terms not in the public disclosure — availability guarantees, performance liquidated damages, parts cost pass-through, and scheduled maintenance scope. What can be said is simple: Vestas holds no project equity, and the service revenue stream flows offshore for twenty years regardless of how SPC-side equity returns develop. Korea Midland Power’s BOP O&M role does not change that picture. The “purely domestic capital” framing applies to sponsor equity, not to the highest-value equipment contracts. Those risks fall disproportionately on the non-contract equity holders, especially Future Energy Fund.

Cost overrun risk in this structure is partially balanced through sponsor support undertakings. The three sponsors with historical involvement in project development — Hanwha Ocean, Hyundai E&C, and SK Eternix — have committed to inject additional capital if project costs exceed the contracted amounts, creating a strong incentive for the parties controlling EPC execution to keep CAPEX disciplined.

Future Energy Fund Carries the Residual Risk Without the Margin

Excluding cost overrun, every other source of project downside — operational underperformance, SMP volatility, grid curtailment, and any other erosion of net cash flow — concentrates on the two cap table participants that hold no service contracts. SK Eternix holds 10% with no offsetting margin extraction (SK Eternix’s own KIND filings report 16.67%; this analysis uses the 10% figure from the joint government release). Future Energy Fund holds 40% with no offsetting margin extraction. Together they absorb 50% of project residual downside while collecting no upstream contract margins. Of that 50%, Future Energy Fund accounts for 80%.

Future Energy Fund’s expected return depends entirely on dividend distributions from SPC net cash flow, which is the residual after every upstream margin holder has been paid. Any erosion reduces the Future Energy Fund return one-for-one. Hanwha Ocean’s EPC margin, Vestas’s turbine and service margins, Hyundai Steel Industries’ fabrication margin, and Korea Midland Power’s BOP O&M revenue all sit upstream of that residual.

Future Energy Fund absorbs 40% of project residual downside, matching its cap table share. The distinction from Hanwha Ocean and Korea Midland Power, who hold equivalent equity-proportional exposures on paper, is the absence of an offset. Their residual downside is cushioned by upstream contract margin streams that flow regardless of operational performance. Future Energy Fund’s nominal equity share and its effective residual risk share are the same number. This single-project concentration matters for fund capacity. The binding constraint on how many similar deals the fund can absorb is per-project risk concentration, not headline capital size.

Revenue Structure Adds a Layer of Volume Risk

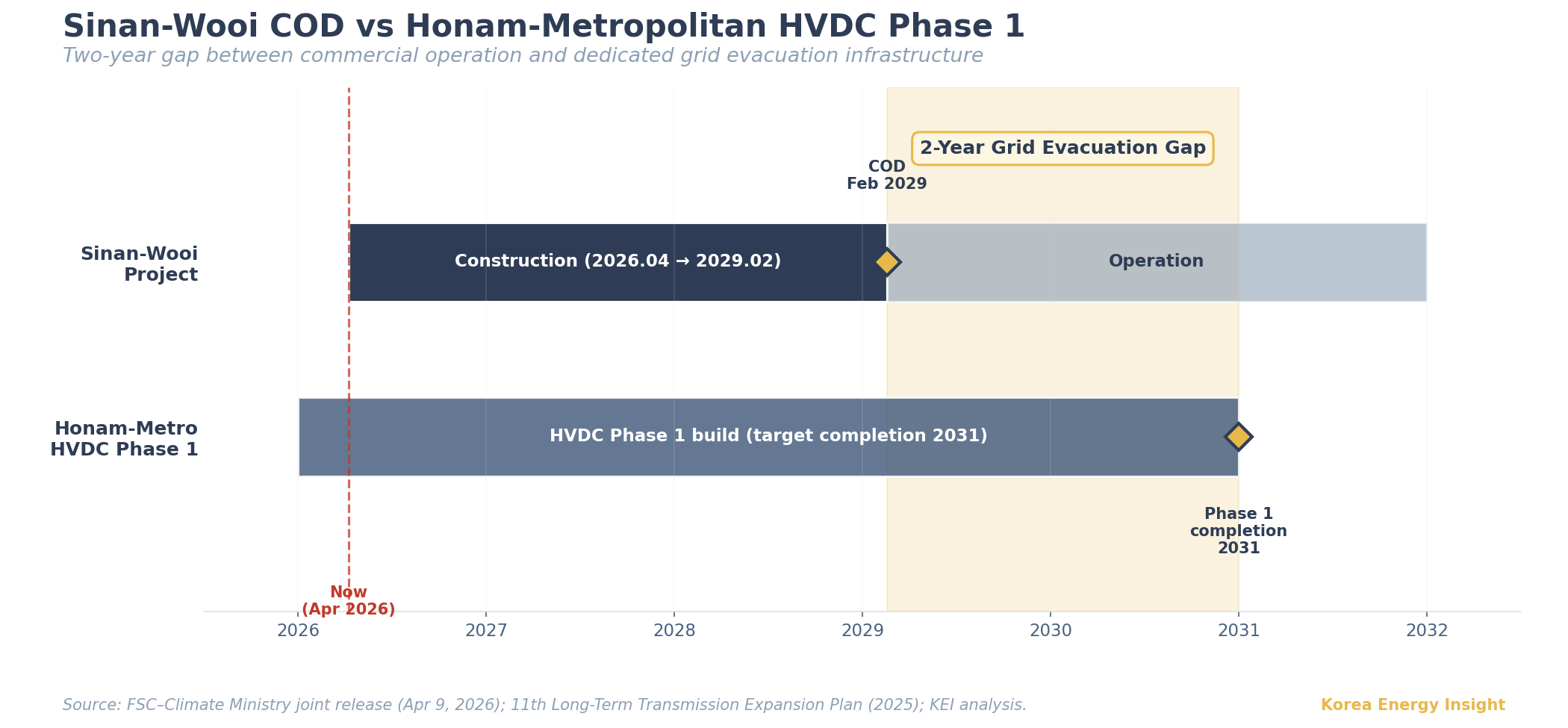

Korea’s Renewable Portfolio Standard structure pays project revenue through two channels: System Marginal Price (SMP) for energy and a separate Renewable Energy Certificate (REC) market. Sinan-Wooi secured a fixed REC price through Korea’s wind power fixed-price auction in 2023, and the structure diagram in the joint government release identifies Korea South-East Power as the REC offtake counterparty under a long-term contract. This provides price certainty on the REC component. SMP, by contrast, fluctuates with the wholesale market. REC pricing is locked for the contract term. Volume is not.

Volume depends on grid availability. Korean renewable generation is technically must-run, so dispatch curtailment is rare. Grid congestion curtailment is not. The Jeolla region, where Sinan-Wooi is located, already hosts solar capacity that exceeds available transmission to the Seoul metropolitan demand center. Resolving this bottleneck requires the Honam–Metropolitan HVDC corridor, whose phase 1 is targeted for 2031 under the 11th Long-Term Transmission Expansion Plan finalized in 2025. Sinan-Wooi targets COD in February 2029, two years before the first HVDC phase comes online. Sinan-Wooi will reach commercial operation into a transmission environment where the dedicated evacuation infrastructure is not yet built, with timing of resolution outside any sponsor’s control.

This grid risk distributes through the same allocation logic. Margin contracts are paid before COD or depend only on operations, not on whether dispatch reaches the demand center. Future Energy Fund’s 40% equity stake absorbs volume risk in full.

The seven-year history of the sponsor lineup explains how this asymmetry took shape — and who shaped it.

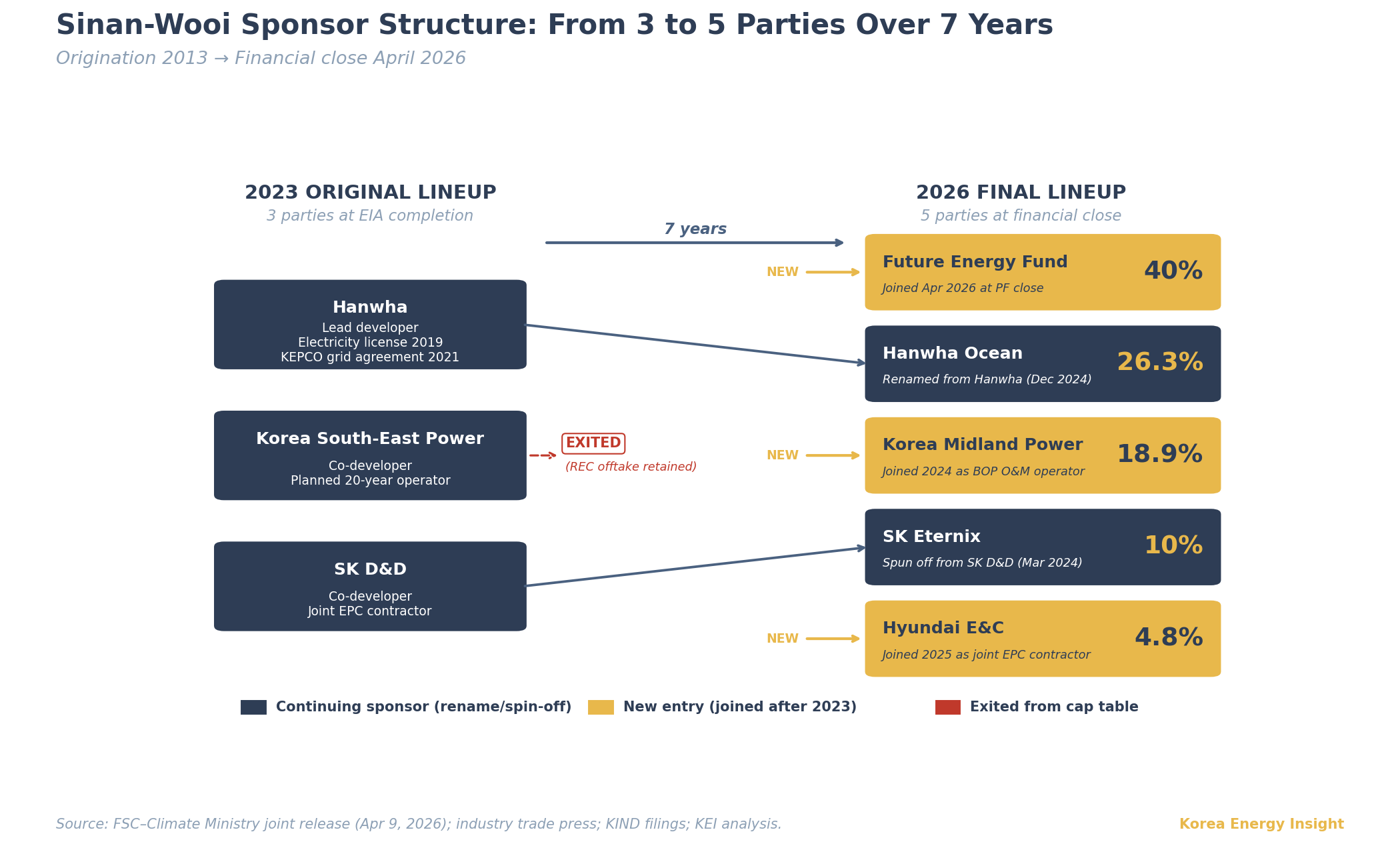

The Sponsor Lineup History

Sinan-Wooi was originated in 2013 by Hanwha’s construction division, which obtained the electricity business license in 2019, signed the grid connection agreement with KEPCO in 2021, and led development through environmental impact assessment completion in August 2023. The original project sponsor lineup, as documented in 2023 industry trade press coverage of the implementation design kickoff meeting, consisted of three parties: Hanwha as lead developer, Korea South-East Power as co-developer and planned 20-year operator, and SK D&D as co-developer and joint EPC contractor.

Between late 2023 and the financial close in April 2026, the sponsor structure was rebuilt. Hanwha’s role transferred to Hanwha Ocean through an intra-group business transfer effective December 1, 2024, with the Sinan-Wooi position specifically identified within the wind business transfer perimeter in regulatory filings. SK D&D’s renewable energy business was spun off as SK Eternix in March 2024. Korea Midland Power joined the cap table at 18.9% as the BOP O&M operator.

Korea South-East Power, the originally planned 20-year operator under the 2023 lineup, no longer appears in the sponsor structure; the joint government release shows Korea South-East Power retained only the REC offtake contract counterparty role. Hyundai E&C joined as joint EPC contractor. Future Energy Fund joined as the largest single equity holder at 40%.

The final lineup at financial close consists of five parties: Hanwha Ocean 26.3%, Korea Midland Power 18.9%, SK Eternix 10%, Hyundai E&C 4.8%, and Future Energy Fund 40%. Seven years passed between the 2019 electricity business license and the 2026 financial close. SK Eternix itself is currently being acquired by KKR, named preferred bidder in February 2026 on a 30.98% + 12.52% stake package, with closing scheduled for June 30, 2026. The implications of this transfer are addressed in the forward-looking section.

The reshuffling has two distinct layers. Korea South-East Power’s retreat to the REC offtake position and Hanwha’s transfer to Hanwha Ocean were commercial decisions made within the sponsors’ own assessment frame. Korea South-East Power’s exit preceded both the Future Energy Fund’s active deployment and the Strategic Industry Fund’s launch, which indicates the decision was based on project economics as they stood at the time, not on the cushioned structure that eventually closed. Had policy capital of this scale been visible as an incoming variable, the REC-only retention would have been difficult to justify internally — the cushioned structure meaningfully reduces the risk profile that drove the exit in the first place. The retention of REC offtake without equity, operational responsibility, or further CAPEX commitment reads as a hedged exit: project economics assessed as insufficient, downside contained, REC revenue retained as a back-end claim if the project eventually reached COD.

Hanwha Ocean’s 26.3% continuing position follows a different pattern, one well-established in Korean LNG combined-cycle PFs. Korean EPC contractors routinely hold equity through construction as a credibility and performance guarantee, then exit after COD once the contract margin is booked and the reference credential is built. Whether this pattern repeats at Sinan-Wooi becomes visible only after COD.

Future Energy Fund’s 40% late-stage entry sits in a different layer. Fund deployment of this scale is not a variable a commercial developer prices into a financial model during development. Policy capital reduces project risk but imposes governance constraints that equity-heavy sponsors tend to avoid when commercial alternatives exist. A developer building the project from 2019 onward would not base its financial plan on policy capital of this scale arriving later. They would attempt to secure it when the window opened, but not stake the project economics on it in advance.

The implication for the template question is narrower than the headline framing suggests. Commercial sponsors can replicate the cap table architecture. They cannot replicate the cushioning layer on their own. The template question therefore splits into two separate questions: whether commercial sponsors adopt the architecture, and whether policy funds match it on a project-by-project basis.

What This Is

The sponsors that extract the largest contract margins absorb only 26.3% (Hanwha Ocean) and 18.9% (Korea Midland Power) of project downside through their cap table positions, and that exposure is itself cushioned by the upstream margin they are already receiving. The largest equity holder, Future Energy Fund at 40%, extracts no margin at all. The other non-contract sponsor, SK Eternix at 10%, extracts no disclosed operating margin.

The “purely domestic capital” framing in the headline describes the cap table accurately. The contract margin distribution tells a different story, where the highest-value extraction routes flow either to a foreign OEM with zero equity exposure or to domestic contractors whose downside exposure through equity is a fraction of their margin upside through contracts.

The Same Pattern Built Korean Heavy Industry

The asymmetry described above is unusual by global PF standards. It is also recognizable. Korean shipbuilding, steel, semiconductors, and lithium-ion batteries all developed under variations of the same pattern. Public capital absorbed first-mover risk on a strategic project.

Selected domestic contractors built operational credentials they could not otherwise build. Once those credentials existed, the same firms competed in global markets on commercial terms. The model has produced multiple globally competitive industries over five decades.

Korean offshore wind suppliers, including the foundation fabricators, cable manufacturers, and the 15-MW WTIV vessel built specifically for this project, gain reference credentials through Sinan-Wooi that they can use in markets where reference matters more than price. Credential formation here splits into two tracks on different clocks. Supply chain credentials — foundation fabrication, cable supply, installation vessels — can be built through a single large project because the underlying manufacturing and heavy construction capabilities already exist in Korean shipbuilding, steel, and civil engineering. The gap being filled is offshore-wind-specific reference, not fundamental capability, and that gap closes fast.

O&M credential formation runs on a different clock. It requires operating time, and the turbine service component is gated by the long-term service agreement cycle. A domestic operator cannot accelerate into turbine service during an existing contract period. The first genuine opening comes at LTSA renewal, typically 5 to 10 years after COD.

The seven-year stall ended in a single financial close, and subsequent permits and PF closings are likely to move faster because the precedent now exists. The policy capital sits inside the SPC rather than on any sponsor’s balance sheet. This distinguishes Sinan-Wooi from direct firm subsidy. The capital is ring-fenced to the project, not the companies, which is a different kind of arrangement from what standard corruption or favoritism critiques assume. Whether the offshore wind ecosystem follows the trajectory of Korean shipbuilding or stalls at the first PF depends on what the next three to five large-scale projects look like.

Base case: The Sinan-Wooi capital structure becomes the template for Korea’s next wave of large-scale offshore wind PFs. Future Energy Fund and the Strategic Industry Fund provide first-loss layers and RWA relief on a project-by-project basis. At the full $6.21 billion (KRW 9 trillion) of Future Energy Fund capital deployed across its planned five-stage rollout, and roughly $375 million (KRW 540 billion) deployed in this single project, the fund has theoretical capital-basis capacity for approximately fifteen similar transactions over its full deployment cycle. Risk-basis capacity is lower. If each subsequent project places Future Energy Fund in the same unoffset 40% position as Sinan-Wooi, the effective deployment ceiling is bounded by how much offshore wind residual risk one fund book can hold at a time rather than by capital availability. Stage-by-stage commitment limits how quickly either capacity becomes available.

What I’m watching:

Whether the next large-scale offshore wind PF in the pipeline replicates this capital structure or moves to a different model.

The closing of the KKR–SK Eternix transaction, scheduled for June 30, 2026. Reporting indicates the deal was marketed as part of a broader renewables package including SK Innovation E&S and SK Ecoplant assets, although the formal sale filings cover only SK Eternix shares. The Sinan-Wooi exposure sits inside SK Eternix, which separately discloses a direct SPC shareholding in its own filings. Public filings disclose no carve-out, and SK Discovery retains no renewable operating arm capable of holding the stake post-closing. On both counts, the Sinan-Wooi equity should be read as transferring with SK Eternix when the deal closes. That moment becomes the first foreign PE entry into a Korean offshore wind project closed on policy capital cushioning. Project governance impact is unclear given the stake size.

Whether Korea Midland Power, the BOP O&M contractor, expands its scope to include turbine service at the first contract renewal cycle. Long-term turbine service contracts in adjacent rotating equipment markets typically run in 5–10 year cycles, with renewal negotiations creating opportunities for scope transfer to local operators. Whether this dynamic applies to offshore wind LTSA in Korea is untested.

Disclosure of turbine service agreement terms in subsequent large-scale Korean offshore wind PFs. Availability guarantees, performance liquidated damages, and parts cost allocation set the pricing floor for Korean offshore wind O&M and determine whether long-term service revenue remains with the foreign OEM or transfers to domestic operators at contract renewal. The Sinan-Wooi service agreement terms themselves are unlikely to be disclosed directly, but competitive OEM quotes in subsequent PFs can reverse-engineer the benchmark.

Honam–Metropolitan HVDC corridor phase 1 completion timeline relative to Sinan-Wooi’s February 2029 COD target.

Future Energy Fund deployment pace across its planned five-stage rollout. The fund’s remaining capacity after Sinan-Wooi determines how many of the pipeline’s large-scale offshore wind projects can rely on the same cushioning mechanism. If the fund’s stage gates slow the availability of capital below the pace of project development, the template question answers itself by default: the next few projects will not have the same structure because the structure will not be available.

What would change my mind: A subsequent large-scale offshore wind PF closing without policy fund participation, or with materially different sponsor cap table architecture. That would suggest the Sinan-Wooi structure was a one-time arrangement to clear the seven-year backlog rather than a permanent operating model for Korean offshore wind PF.

If this analysis is useful for your team’s Korea offshore wind exposure assessment, consider sharing it with colleagues evaluating the next round of projects.