The Anatomy of Korea's VPP Market: 80 Aggregators, Two Policy Tracks, No Profit Pool

Korea's government is not waiting for VPP economics to work. Two policy tracks are filling the gap.

DEEP DIVE | Image: KPX (Korea Power Exchange)

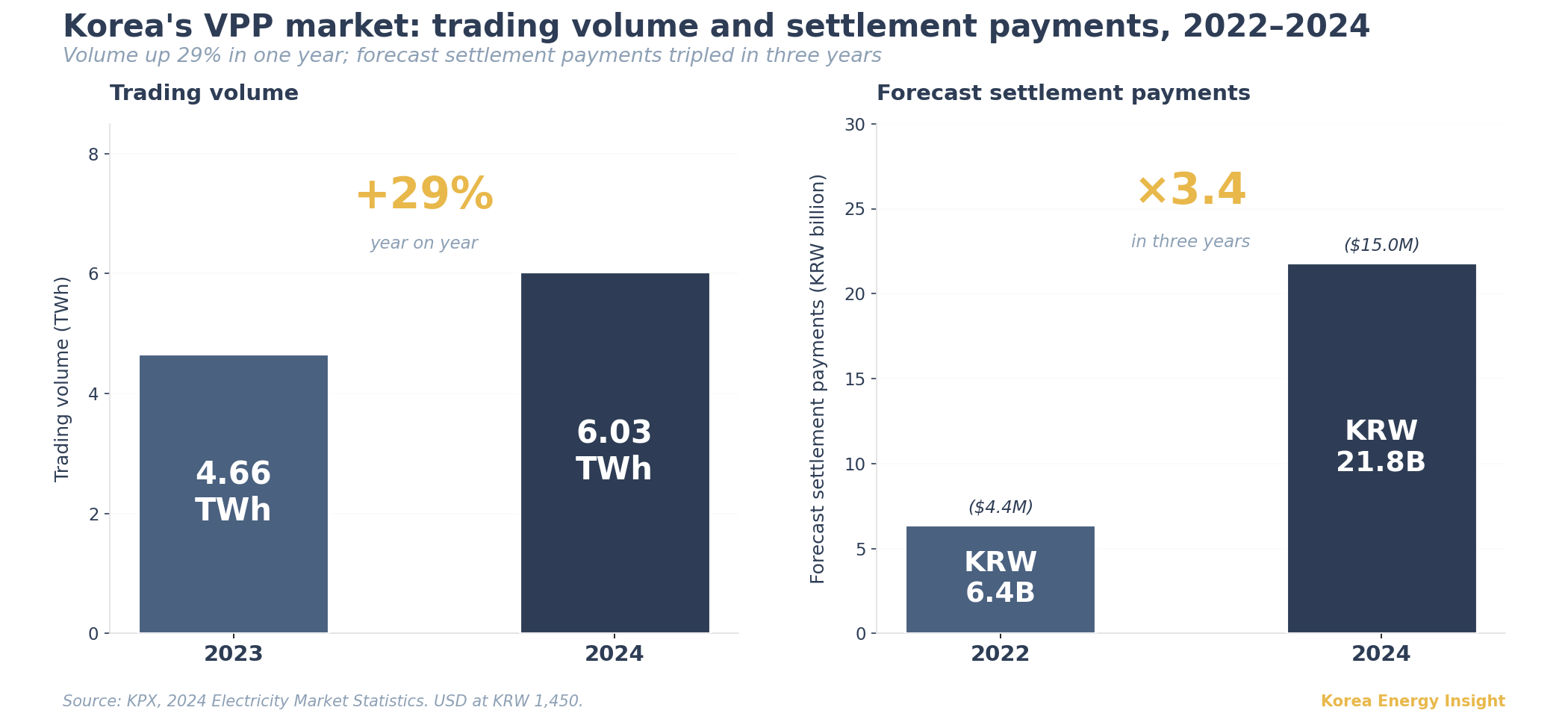

In 2024, Korea’s small-scale power brokerage market traded 6.03 TWh of electricity, up 29% from 4.66 TWh the year before (KPX, 2024 Electricity Market Statistics). Forecast settlement payments tripled in three years, from KRW 6.4 billion in 2022 to $15 million (KRW 21.8 billion; all USD conversions at approximately KRW 1,450/USD) in 2024. As of December 2025, eighty registered aggregators manage 6,611 distributed energy resources totaling 5,984 MW (KPX). By every volume metric, Korea’s virtual power plant (VPP) market is no longer a pilot. It is an early-stage commercial market.

The driver is structural. The 11th Basic Plan targets 77.2 GW of solar and 40.7 GW of wind by 2038. Korea Power Exchange (KPX)’s direct market visibility into installed solar capacity remains far smaller than Korea’s total fleet — most distributed solar sits outside the wholesale market entirely. As distributed resources multiply into the tens of thousands of units, KPX cannot dispatch them individually. Someone has to aggregate them, forecast their output, respond to dispatch signals, and bear the financial consequences of getting the forecast wrong. That someone is the VPP aggregator. The business model is monetizing the grid operator’s management risk.

Starting March 1, 2026, under the spring quasi-central dispatch window (March–May), Korea’s renewable quasi-central dispatch regime gave aggregators their first dispatch-linked revenue path. Renewable generators above 20 MW can participate directly; those at or below 20 MW must participate through a VPP aggregator. The base settlement rate is 10.68 won/kWh, with a forecast deviation deduction of 1.26 won/kWh applied to the prediction-scheme component (KPX, quasi-central dispatch operating notice). For the first time, aggregators have a revenue stream linked to dispatch performance rather than passive collection of the system marginal price (SMP).

The conventional reading of these numbers is that Korea has built a real VPP market and that the eighty registered aggregators are riding a structural growth wave. That reading is half right. The growth is real, but most of the eighty are not riding standalone economics at all. Across global markets where pure-play aggregator financials are visible, durable standalone margins do not exist yet. Korea’s policy architecture is not closing that gap by accident. It is making that asymmetry more explicit than other markets have, with capital and revenue flowing through specific operator categories rather than to the eighty as a class. This piece is about which categories, why, and what it means for the next twelve months of policy signals.

Global context: where standalone VPP economics actually work, and where they don’t

The growth case is straightforward. The profitability case is harder. Public evidence for durable standalone VPP margins is still thin.

Stem Inc., the only publicly listed pure-play VPP software company, reported $156 million in revenue and $6.7 million in adjusted EBITDA for full-year 2025 (Stem Inc., Q4 2025 results, March 2026). That works out to an EBITDA margin of roughly 4%, and it is the company’s first positive adjusted EBITDA at the annual level. In 2024, Stem wrote off $547 million in goodwill and posted a net loss of $854 million (Stem Inc., SEC 8-K filings). The 2025 turn matters, but on a thin margin and after a full goodwill impairment the prior year. The standalone software model is not yet proven at scale.

Statkraft operates Europe’s largest VPP — over 10 GW of capacity across more than 1,000 generators — but does not disclose VPP revenue separately. The VPP sits inside a 21.6 GW generation portfolio (Statkraft Annual Report 2024) as an optimization layer, not a standalone business unit. Sunrun, America’s largest residential solar company, takes the same approach. Its VPP enrollment numbers are growing fast, but Sunrun uses VPP as a tool to lift battery attachment rates rather than reporting it as a standalone revenue line.

Next Kraftwerke, once the reference case for independent VPP aggregation, was acquired by Shell in 2021. Its standalone financials are no longer public.

The pattern across the US, Europe, and Australia is consistent. Where VPP economics look durable, the operator already owns the underlying assets. Where the aggregator owns nothing and tries to earn a margin between grid payments and asset-owner incentives, public data shows margins that are thin, volatile, or simply not disclosed. Europe adds another pressure: aggregators acting as Balancing Responsible Parties bear financial responsibility for forecast deviations through imbalance settlement. A 2024 Greek study found that a 550 MW aggregator faces €1 million to €2.7 million in annual non-compliance charges at 5–6.5% deviation rates (ScienceDirect, December 2024). These charges eat directly into already thin margins. Korea is now building its own version of this market. Korea’s policy architecture is more explicit about which operators it supports than global markets have been, and the answer to who benefits is more specific than the headline numbers suggest.

Korea situation: a market growing fast on policy, not on standalone economics

Korea’s VPP market is growing because it has to. The 77 GW solar target makes aggregation a necessity, not a choice. But market revenue alone will not sustain independent aggregators, and the Korean government is filling the gap on two tracks.

The first is a revenue track. The quasi-central dispatch settlement of 10.68 won/kWh, in effect from March 1, 2026, gives aggregators an income stream linked to dispatch performance, not wholesale price passthrough. Coverage is currently limited to the spring window and to renewables at or below 20 MW.

The second is a capital track. On February 20, 2026, the Ministry of Climate, Energy and Environment announced its Next-Generation Distributed Power Grid plan. The implementing program, run by the Korea Energy Agency (한국에너지공단), is the Distribution-Grid-Connected ESS Deployment Support Program (배전망 연계형 ESS 구축지원 사업). It commits KRW 117.6 billion ($81 million) in 2026 for 20 distribution circuits in Jeolla — 11 in Gwangju and South Jeolla, 29 in North Jeolla. Each circuit gets one 4 MW / 20 MWh ESS, financed at 50% public subsidy — about $4 million in public capital and $4 million in operator self-financing per circuit.

The full five-year plan through 2030 commits roughly KRW 1 trillion ($690 million), scaling to 85 circuits and 340 MW of total ESS capacity. Each circuit is designed to enable at least 5.7 MW of additional solar interconnection. The plan also introduces a Non-Wires Alternatives (NWA) compensation scheme: where ESS investment replaces new grid construction, the avoided construction cost is paid to the ESS operator. Eligible lead contractors are VPP operators specifically, with a 20-year minimum operational obligation. Final selection runs through mid-June 2026.

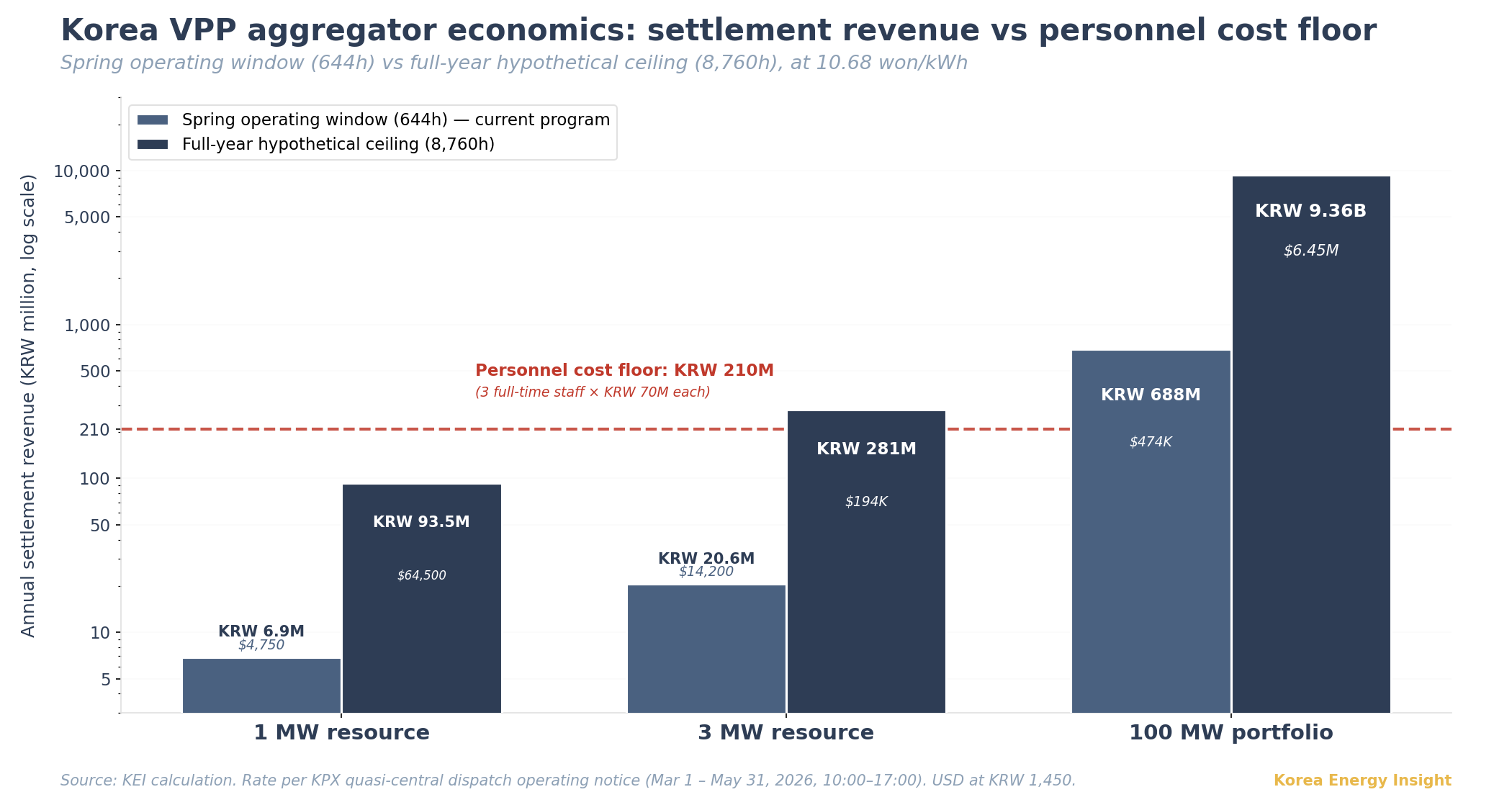

The arithmetic of why these tracks are necessary is straightforward, and it works at two levels. First, take the program as it actually runs today. The 2026 quasi-central dispatch window covers 92 days (March 1 to May 31), seven hours per day (10:00 to 17:00) — about 644 operating hours in total (KPX, quasi-central dispatch operating notice). Applied across the full 644-hour window at 10.68 won/kWh, a 1 MW resource tops out at about $4,750 (KRW 6.9 million) in maximum settlement. A 3 MW resource reaches roughly $14,200 (KRW 20.6 million). Even a 100 MW portfolio hits a ceiling of only about $474,000 (KRW 687.7 million). Now extend the same rate to a full 8,760-hour year as a hypothetical ceiling. The 1 MW resource reaches about $64,500 (KRW 93.5 million); 3 MW reaches $193,000 (KRW 280 million); 100 MW reaches $6.45 million (KRW 9.36 billion). The hypothetical ceiling is 13.6× the actual program, and even at that ceiling the smaller resource sizes do not clear the operating cost of running an aggregator.

Compare both cases to the cost of running an aggregator. Assume a viable VPP control desk needs at least three full-time staff at roughly KRW 70 million each. That is KRW 210 million in personnel cost alone, before any technology, settlement, or business development overhead. The forecasting and dispatch infrastructure does not scale down to two people. And the aggregator does not keep the full settlement: economics depend on a revenue share with the underlying generation owner, who is typically the larger party. Add forecast deviation deductions and settlement delays, and even at the full-year ceiling, only a 100 MW portfolio comfortably clears the personnel floor. Under the actual operating window, the math is much tighter. Below 100 MW, standalone economics simply do not work without policy backstop or asset ownership.

Together, the two tracks underwrite a business model that market margins alone cannot support. The question is no longer whether Korea’s VPP market grows — it will. The question is who captures the value.

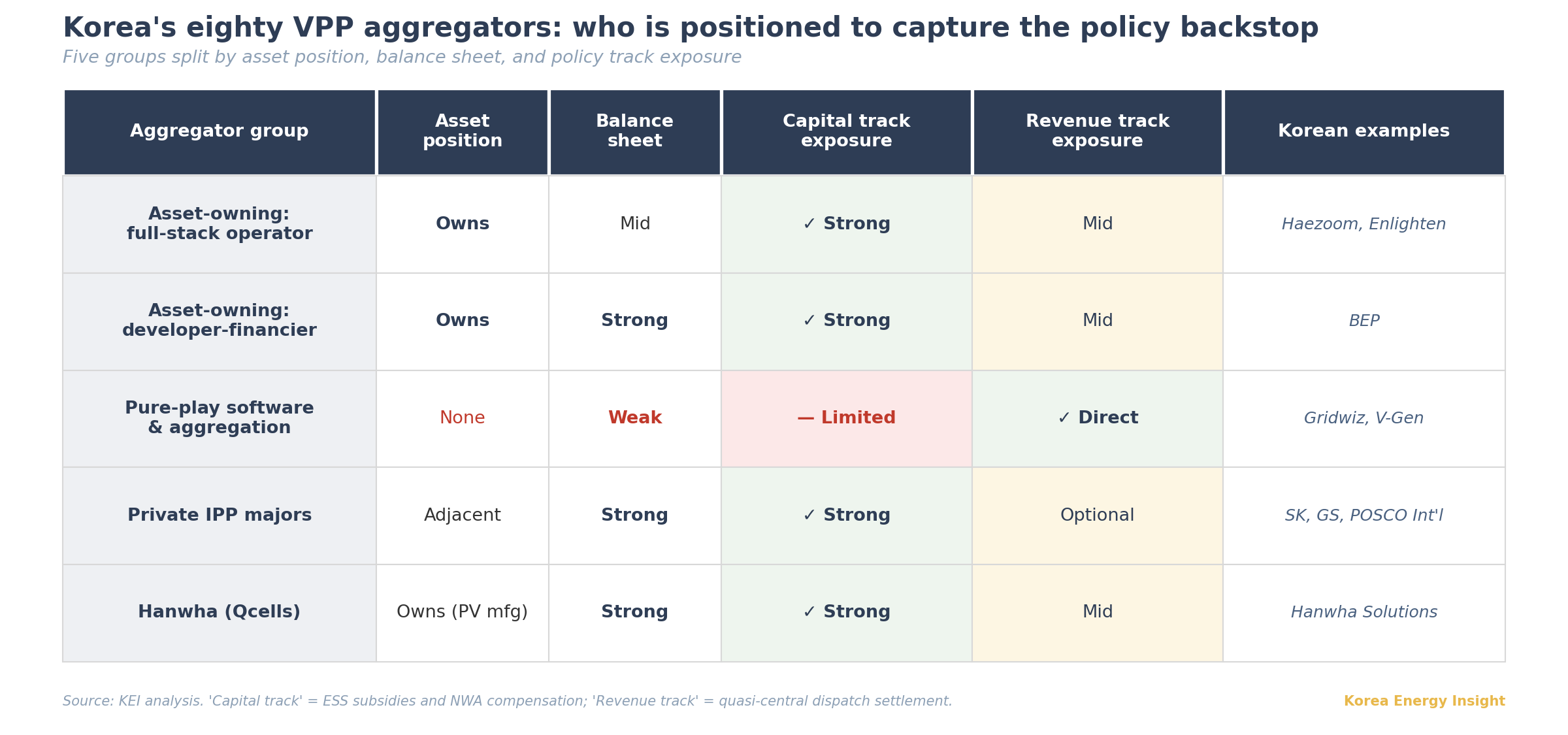

The eighty aggregators are not one asset class

Korea’s eighty registered aggregators are not a single asset class. They split into three core groups, with one notable outlier — Hanwha as a hybrid case — and GENCOs covered as a separate observation. Each group’s exposure to the policy backstop is different.

Asset-owning aggregators are most directly aligned with the global pattern of VPP profitability. They split into two sub-types. The first is the full-stack operator model: companies like Haezoom and Enlighten that run solar EPC, O&M, and forecasting/control software in-house. Haezoom manages roughly 1.3 GW; Enlighten reports around 5.4 GW connected. The second is the developer-financier model: companies like Bright Energy Partners (BEP) that hold solar and BESS assets directly but concentrate on business development and project finance, sourcing EPC externally. BEP runs more than 300 solar plants and has secured BlackRock financing across four rounds. Both sub-types share the same structural advantage: they already control the underlying solar and BESS assets, so the marginal cost of layering VPP services on top of an existing project pipeline is low. Both are also the clearest beneficiaries of the capital track. ESS subsidies and NWA compensation flow most easily to operators that can finance, build, and operate distribution-grid ESS. BEP’s recent Jindo long-duration BESS award with Korea Southern Power, structured as a consortium, is one example.

Pure-play software and aggregation specialists — companies like Gridwiz and V-Gen — built their businesses around forecasting, control, and settlement capability rather than asset ownership. These are the closest analogues to Stem Inc., and the most exposed to the global pattern: thin margins, dependence on platform scale, vulnerability to settlement-rate changes. They benefit most directly from the quasi-central dispatch revenue stream but bear the full forecast-deviation deduction if accuracy slips. They have the strongest forecasting tools but lack the balance sheet to compete for the capital track.

Private IPP majors — SK (including SK Innovation E&S), GS, and POSCO International — are the three dominant players in Korea’s private power generation space. Their VPP activity to date varies and is rarely a headline business line. The category matters less for current VPP exposure than for adjacency and scale. Each already runs LNG combined-cycle generation, retail electricity supply, renewable development, and energy trading, and any of them can stand up or pivot a VPP business off that platform whenever the economics warrant. Their willingness to operate at low or zero standalone VPP margins is structurally higher than the pure-play group’s.

Hanwha runs its VPP activity through a single entity: Hanwha Solutions’ Qcells division, the group’s solar PV manufacturing arm. Qcells operates its own VPP platform Q.OMMAND and entered Korea’s small-scale brokerage market in early 2023 (Industry News interview with Qcells executive Yoo Jae-yeol, March 2023). It is pursuing a VPP model that integrates its solar manufacturing, residential energy systems, and EV charging businesses. Hanwha Energy, the group’s industrial-complex CHP (district energy) operator, is unlikely to register on its own; if its CHP fleet ever joins a Hanwha VPP portfolio, the integration would route through the Qcells track. The group’s domestic IPP scale is smaller than the three majors above, but the Qcells VPP entry is one of the more concrete commitments in this category.

A separate observation: Korea’s GENCOs are also active in the brokerage space. KOMIPO operates a public VPP platform, and KOEN was named as a brokerage participant as early as 2023. But the policy backstop’s lead-contractor language does not appear to flow to public-enterprise generators by institutional default.

Implications: who captures the value the policy is creating

The two tracks exist because Korea’s government has reached the same conclusion the arithmetic already points to: independent VPP aggregators cannot sustain themselves on market revenue alone. The revenue track — quasi-central dispatch settlement — opens an income stream linked to dispatch performance, but on its own it is not enough. The capital track is the heavier commitment. It puts public money into the distribution-grid ESS hardware that makes aggregation physically possible, and routes that money through VPP operators as eligible lead contractors. That is where the structural advantage sits.

The Korea Energy Agency has been explicit about why. A KEA official told Electimes that the program’s core is “not ESS deployment but VPP operator development” (Electimes, March 2026). The 20-year obligation paired with VPP-only contracting screens for operators that can commit two decades of balance-sheet capacity to a first-of-kind program. The eligibility rules and per-unit economics are where the friction will show up. First-of-kind Korean support programs in this space usually reveal gaps between policy intent and operational reality only after contractors start working through the conditions.

Korea is creating a VPP market, but not yet a standalone profit pool for the eighty aggregators currently registered. The two policy tracks favor operators with existing assets, balance sheets, and regulatory access — not pure-play software aggregators. Looking at how Korean energy policy has historically managed fragmented markets, the policy architecture appears more compatible with a smaller field of operators than with supporting eighty independent ones. The existing eighty are left to find their own level rather than seeing the field expand further.

The base case is straightforward. Korea’s VPP trading volume continues growing at the recent ~30% pace as renewable capacity expands. Asset-owning aggregators reach positive operating margins first, supported by the capital track. Pure-play software specialists remain dependent on settlement-rate calibration and forecasting accuracy. Private IPP majors keep VPP as an optionality layer on top of existing portfolios, ready to scale or acquire if the policy architecture develops. The government adds incremental revenue channels over the next twelve months, most likely through expanded quasi-central dispatch scope and the first NWA compensation payments.

What to watch

Settlement data from the spring 2026 quasi-central dispatch window once it becomes available. The first selections under the Distribution-Grid-Connected ESS Deployment Support Program in mid-June 2026, including which operator categories actually win the 20 Jeolla circuits. The 12th Basic Plan for Electricity Supply and Demand’s treatment of VPP and distributed resources. Any signal that MOTIE is opening balancing or capacity market access for aggregators.

What would change the base case: A Korean pure-play aggregator demonstrating positive operating margins from market revenue alone — without leaning on the capital track or settlement subsidies. Or a global pure-play VPP company achieving sustained EBITDA margins above 15% across two or more reporting years.

If this analysis is useful for your team’s view on Korea’s distributed energy market, consider forwarding it to a colleague.