Korea's Ninh Thuan 2 Bid After the Westinghouse Settlement: What the April MOUs Mean for Financing Closure

Russia got an IGA. Korea brought policy banks on day one.

MARKET SIGNAL

Vietnam set two deadlines for its restarted nuclear program: an international partner agreement on Ninh Thuan 1 by September 2025, and on Ninh Thuan 2 by December 2025 (Government Resolution 249/NQ-CP, August 22, 2025). Both passed unsigned. Russia closed the gap on March 23, 2026, with an intergovernmental agreement covering two VVER-1200 reactors and 2,400 MW at Ninh Thuan 1. One month later, on April 22 in Hanoi, Korea moved to enter Ninh Thuan 2. Not with an IGA. With four memoranda of understanding signed across two days — two at the heads-of-state ceremony on April 22, two more around the Korea–Vietnam business forum on April 23. Same program, different counterparties, two stages apart.

That stage gap is where the analysis starts. The package was structured the way Korea structures a deal it cannot yet price. At the April 22 presidential ceremony: KEPCO with Petrovietnam (PVN) on nuclear cooperation review, and a four-party financing MOU placing both Korean policy banks at the table on day one — KEPCO, Korea Eximbank (KEXIM), Korea Trade Insurance Corporation (K-SURE), and PVN as parties. At the April 23 business forum: KEPCO with Vietnam Electricity (EVN) on power infrastructure covering transmission, BESS, and digital plant operations (specific scope undisclosed); Doosan Enerbility with PTSC and PETROCONs on supply chain. Policy banks at MOU stage is unusual, and it tells you what the bottleneck is. Korean engagement on Ninh Thuan 2 itself goes back more than a decade — a 2012 nuclear cooperation agreement and a 2013 joint preliminary feasibility study sized at roughly $10 billion (World Nuclear Association). What is new in April 2026 is not the interest but the structure.

Read together, the four documents look less like four separate MOUs and more like one architecture spread across four tracks: the reactor (KEPCO–PVN), the surrounding grid that has to absorb it (KEPCO–EVN, covering transmission, BESS, and digital plant operations), the local supply chain that has to build it (Doosan–PTSC and PETROCONs), and the financing that has to pay for all of it (the four-party policy bank MOU). That is closer to a build-operate-finance-and-integrate offer than a conventional EPC bid. The shape of the package reads as Korea’s diagnosis of where Vietnam’s power and nuclear program is bottlenecked today. Vietnam has made no public request for a bundle of this scope, but the substance of what was signed suggests a degree of acceptance. Heads-of-state signings rarely happen without a reason on either side. The package is politically meaningful but not yet bankable. None of the documents disclose price, technology model, financing size, risk allocation, or exclusivity.

The Settlement Korea Cannot Test in Public

This is Korea’s first overseas nuclear push initiated under the post-settlement framework. (The Czech Dukovany selection of July 2024 pre-dated the January 2025 Westinghouse–KHNP–KEPCO settlement; its commercial terms continue to be worked through within that framework.) Westinghouse’s official release stated that “details regarding the terms of the settlement remain confidential” (Westinghouse press release, January 16, 2025). Westinghouse had sued in October 2022, alleging that Korea Hydro & Nuclear Power’s APR1400 and APR1000 designs derived from licensed Westinghouse technology and required US Part 810 export authorization (Westinghouse Electric Co. v. KHNP complaint, US District Court for the District of Columbia, October 2022). The case was dismissed in September 2023 on the ground that Westinghouse had no private right to enforce Part 810. The 2025 settlement followed and reset the legal frame on commercial terms neither side has formally disclosed.

That is the constraint Korea brought into Ninh Thuan 2. Public reporting in Korean media has been extensive on the settlement’s specific cost provisions — per-reactor procurement, technology fees, letters of credit, fuel supply terms — but KHNP has declined to confirm specifics. What is not in dispute is that two letters of credit were issued for the Czech Dukovany project in February 2025, one from NongHyup Bank and one from KEXIM, both at $400 million each (National Assembly disclosure of Korea Eximbank data, October 2025). Whatever the per-reactor cost shape of the settlement is, it is now visible in capital movements.

Two Stretched Balance Sheets

The financing math on Ninh Thuan 2 has to close on two constrained balance sheets, and Vietnam’s side is the harder of the two on paper. The full Ninh Thuan program — Ninh Thuan 1 and 2 combined, 4 to 6.4 GW — is sized at around $22 billion in Korean industry estimates, or close to 5% of Vietnam’s GDP. Ninh Thuan 2 alone, on a 2 to 3.2 GW configuration, falls in the $10–11 billion range. For context, Vietnam’s planned government borrowing for 2026 is $37 billion (about VND 970 trillion), of which roughly 60% covers the budget deficit and the rest goes to principal debt repayment (Vietnam News Agency, April 2026). A single project of this size would absorb close to a third of that envelope.

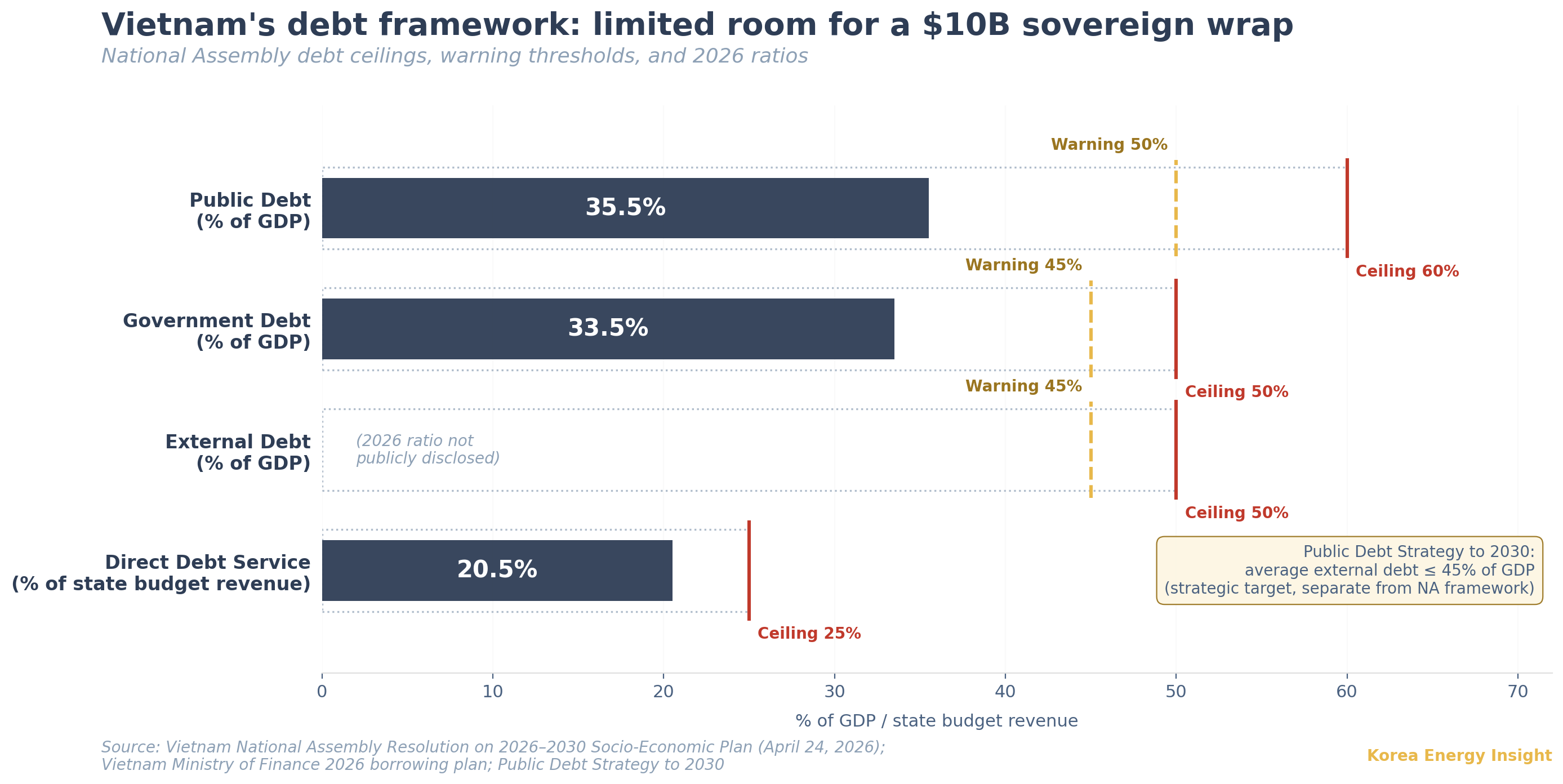

The constraint sits in Vietnam’s own debt rules. The National Assembly’s April 24, 2026 resolution reaffirmed the framework: an annual public debt ceiling of 60% of GDP with a 50% warning threshold; a government debt ceiling of 50% with a 45% warning threshold; an external debt ceiling of 50% with a 45% warning threshold; and direct debt service capped at 25% of state budget revenue. Vietnam’s Public Debt Strategy to 2030 commits to keeping average external debt at no more than 45% of GDP. Current ratios — public debt around 35–36% of GDP, government debt 33–34%, direct debt service obligations at 20–21% of state budget revenue — leave nominal headroom, but the strategic direction is to preserve that headroom, not consume it. Vietnam’s sovereign credit also remains sub-investment grade — S&P BB+, Moody’s Ba2, Fitch BB+ on the unsecured sovereign — with Fitch’s BBB- assigned in January 2026 limited to specific Brady-bond-backed instruments. That profile keeps unsecured external nuclear financing expensive. The historical model has been external concessional financing covering 85% or more, mirroring Russia’s 2011 offer of up to $9 billion for Ninh Thuan 1. It is also the reason the 2016 cancellation cited cost grounds.

A direct sovereign guarantee from Hanoi for a Korean-led $10 billion deal is therefore not a free choice. It interacts with the public debt warning thresholds, the external debt warning, the Public Debt Strategy 2030 average target, and the 25% debt-service rule. PVN and EVN are designated to lead Ninh Thuan 2 and 1 respectively, but neither can carry a project of this scale on its own balance sheet without a sovereign wrap that has limited room to grow. That is what makes the day-one presence of KEXIM and K-SURE in the four-party MOU substantive rather than ceremonial. Korean policy banks were brought to the table because the Vietnamese side cannot guarantee its way to closing on its own.

Korea’s side adds a second layer. KEPCO carries roughly $145 billion (KRW 206 trillion; all USD conversions at approximately KRW 1,420/USD) in consolidated debt as of year-end 2025, even after posting record operating profit of KRW 13.5 trillion (~$9.5 billion) for the year — its highest ever (KEPCO preliminary 2025 results, February 26, 2026). The debt is the legacy of the 2022–2023 fuel-cost shock absorbed under regulated tariffs; the record profit has not yet meaningfully reduced it. The same KEPCO is now expected to sponsor an overseas deal whose Korean precedent, UAE Barakah, returned 0.32% accumulated profit at the parent level and a KRW 332.9 billion (~$234 million) accumulated loss at KHNP (KEPCO 2024 business report; KHNP 2025 H1 report). The four-party MOU is not a financing solution. It is a financing problem put on the table early.

What This Is Not

This is not Russia displacing Japan, or Korea displacing Russia. Vietnam selected Russia for Ninh Thuan 1 and Japan for Ninh Thuan 2 in 2010, suspended both in 2016, and resumed the program in 2024 under a revised Power Development Plan 8 targeting 6.4 GW of nuclear by 2030–2035 and 8 GW by mid-century (Reuters reporting on PDP8 revision, April 17, 2025). Multi-vendor nuclear programs are normal — the UK and China both run them. The substantive change came in late 2025: in a December 8, 2025 interview, Japan’s ambassador to Vietnam, Naoki Ito, told Reuters that “the Japanese side is not in a position to implement the Ninh Thuan 2 project,” citing tight timelines, while signaling continued interest in later-stage SMR cooperation. That ambassador-level on-record statement is closer to an official position than press speculation. It is not a government-to-government withdrawal document. Whether Japan returns to the dialogue at the SMR layer, and on what timetable, is an open variable for Korea — not a settled fact.

What is being tested at Ninh Thuan 2 is not simply whether Korea can win another nuclear contract. It is whether Korea’s post-settlement export package can actually close: bundled across reactor, grid, supply chain, and finance; dependent on policy-bank risk capacity; and negotiated against a Vietnamese balance sheet that still has room on paper but limited room in practice. The April MOUs did not solve that problem. They made it visible.

Base Case, What to Watch, What Would Change It

Base case. Korea moves from MOU to IGA discussions over the next 12–24 months, but EPC and financing close only if the package can solve three constraints simultaneously: Westinghouse-linked cost allocation under the January 2025 settlement, Vietnam’s sovereign-linked financing capacity within its debt-ceiling framework, and KEPCO’s sponsor balance sheet. Pricing will be more compressed for Korea than Barakah was in 2009 or Czech Dukovany was in 2024. The reactor model and technology stack are not yet specified and will be a negotiating variable.

What I’m watching. First, the timing of any Korea–Vietnam IGA — the gap to close before Russia’s pace becomes the benchmark. Second, the disclosed scale of KEXIM and K-SURE commitments under the four-party MOU, which will reveal Korea’s appetite for sovereign-linked exposure. Third, conversion of the Doosan supply chain MOU into binding contracts, which will indicate how the Korean industrial cluster is positioned within the settlement’s component allocations. Fourth, any Japanese signal about SMR cooperation in Vietnam, formal or informal. Fifth, Vietnamese National Assembly action on PVN’s Ninh Thuan 2 investment policy, scheduled for May 2026. Sixth, whether the EVN grid track converts into separate PPAs or EPC contracts on its own — if Ninh Thuan 2 itself stalls but the grid track moves forward, that confirms a fall-back revenue path for Korean firms; if both stall together, the bundle was a single offer.

What would change my mind. A second Westinghouse-related public action — court filing, regulatory disclosure, or US administration statement — that surfaces settlement terms relevant to Vietnam. A Vietnamese sovereign credit action that materially changes external financing costs. A Korean policy shift on KEPCO debt or overseas nuclear sponsorship limits. A Japanese return to Ninh Thuan 2 at the EPC level rather than the SMR level.

If this analysis is useful for your team’s Asia infrastructure strategy, consider sharing it with colleagues pricing Korean overseas nuclear bids or evaluating Vietnamese sovereign-linked exposure.