The Transformer Supercycle: Korea's Factories Are Booked, Its Projects Aren't

For underwriters of Korean power and data-center assets, transformer and switchgear lead time is now an interconnection-date risk.

DEEP DIVE

Korea’s power-equipment makers have rarely had a better year. By early 2026, the three largest — Hyosung Heavy Industries, HD Hyundai Electric, and LS Electric — carried roughly $20 billion (KRW 30 trillion, at approximately KRW 1,450/USD) in combined order backlog (public reporting on company results). Most of that demand comes from abroad: US grid replacement and AI data-center buildout.

So it would be easy to assume that Korea, of all countries, has nothing to worry about on the equipment side of its own energy transition. In May 2026, that assumption began to crack. MCEE convened KEPCO and the major transformer and cable makers for a formal supply-status review, citing global grid investment and Middle East instability (MCEE, May 26, 2026). The agenda was concrete: shifting procurement planning from one-year to three-year cycles, and flagging import reliance in high-voltage transformer components. The country helping fill the shortage had started to worry about its own.

The Global Squeeze

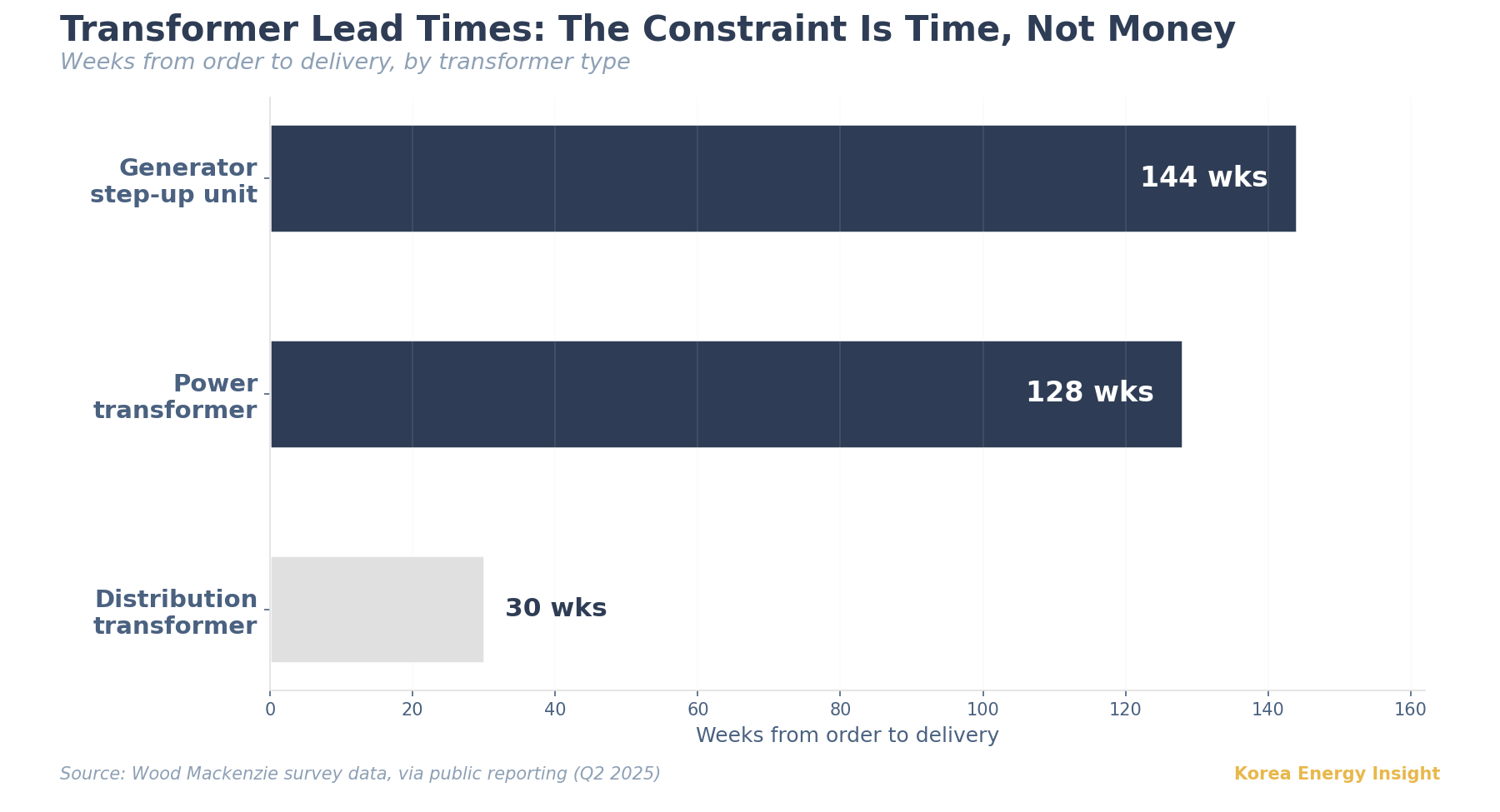

The shortage Korea is responding to is well documented. The International Energy Agency (IEA) reported that, in real terms, cable costs have nearly doubled since 2019 and power-transformer prices have risen by around 75%, with direct-current cable lead times exceeding five years (IEA, February 2025). Public reporting on Wood Mackenzie survey data puts power-transformer lead times at 128 weeks and generator step-up units at 144 weeks — roughly two and a half years. Distribution transformers have eased to about 30 weeks.

The constraint is no longer mainly about money. It is about time and queue position. In the United States, public reporting indicates domestic manufacturing meets only about a fifth of power-transformer demand, leaving the rest to imports. China, by industry estimates, holds close to 60% of global transformer capacity, built on a supply chain that runs from electrical steel through cores and on-load tap changers. For hyperscale data-center developers, electrical equipment is a small share of project cost but can carry almost the whole schedule risk.

Korea sits on the supply side of this shortage. That is precisely why its own exposure has surfaced late.

Korea’s Problem Is Queue Position

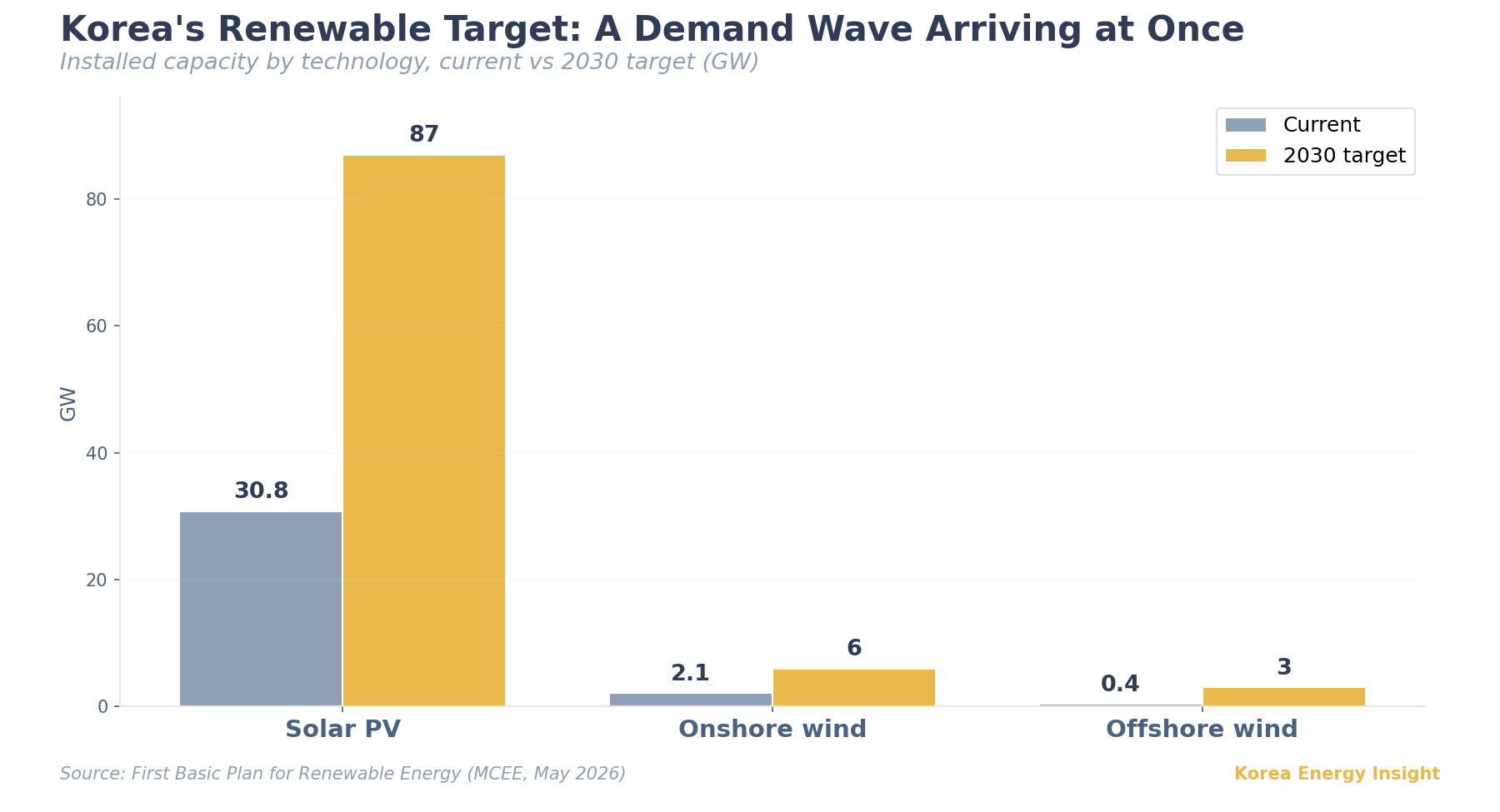

Korea’s problem is not capacity. It is allocation. The same factories filling multi-year export books now face a domestic demand wave arriving at once. The First Basic Plan for Renewable Energy, unveiled on May 19, 2026, targets 100 GW of renewables by 2030. Solar rises from 30.8 to 87 GW, onshore wind from 2.1 to 6 GW, and offshore wind from 0.4 to 3 GW. The plan also targets a renewable share above 30% by 2035 (MCEE, May 2026). Behind that sit the transmission buildout and a data-center pipeline: government and KEPCO data point to 147 operating data centers in 2024 and 637 new power-demand notices by 2029, most in the capital region. All of it lands on the same factories already working through multi-year export books.

The transmission buildout is itself large. KEPCO’s 11th long-term plan targets $50 billion (KRW 72.8 trillion) in grid investment by 2038 — 61,183 circuit-kilometers of transmission lines and 1,297 substations. It explicitly includes the Honam-to-capital HVDC buildout and more than 10 GW of supply for the Yongin semiconductor cluster (KEPCO plan). This volume of transformers and cable, installed at home this decade, is unprecedented, and it competes directly with the export book.

Why does domestic volume lose that contest? The driver is commercial, not cultural. Export orders are larger, booked earlier, dollar-linked, often higher-margin, and increasingly tied to customer proximity in the United States. When the same factory slot can serve a multi-year US utility or data-center order, a domestic project arriving later does not automatically come first. In an economy the OECD describes as tilting resources toward exports and away from domestic consumption — with two-way trade above 80% of GDP — the export book usually wins (OECD Economic Survey of Korea, 2024).

The same logic is now reinforced by overseas expansion. Hyosung is investing $157 million to expand US transformer production (Reuters, December 2025), pulling scarce capacity closer to American buyers and further from the domestic queue. The government appears to grasp this. It is the likely reason MCEE convened the makers at all, rather than leaving domestic supply to the market.

All of that is about volume. A second exposure is narrower, and different in kind: not volume, but dependency. MCEE’s own review named the dependency: bushings and on-load tap changers for high-voltage transformers are import-dependent. Korea’s transformer strength rests on assembly, testing, delivery, and a domestic materials base. POSCO has produced grain-oriented electrical steel since 2004, and Korean steel is exported widely enough to draw anti-dumping cases abroad. But supply of those high-voltage components remains concentrated among a few global suppliers, a sourcing dependency Korea has not closed. In May 2026, Hyosung Heavy Industries signed a 765 kV bushing supply contract with Trench Group (industry reporting) — a reminder that even Korea’s strongest maker reaches outside for the parts that gate delivery. China, which localized converter-transformer tap changers in 2022, is closing that loop; Korea is not there yet. This is not a claim that Korea cannot make these parts; national research programs produced composite bushings up to 550 kV years ago. But the high-voltage, schedule-critical volume still leans on the global chain.

Price is the quieter risk. Export prices have climbed in a sellers’ market, but Korean domestic award prices have stayed comparatively contained, a function of utility purchasing power and that domestic steel base. The buffer is not permanent. As raw-material costs feed through, the gap between export and domestic pricing narrows. KEPCO has agreed to reflect naphtha-driven cable cost increases of 30–40% in contract prices (industry reporting). The stability Korean models quietly relied on begins to loosen.

What This Means for Capital

For a private-equity or infrastructure desk, the first conclusion is structural: there is no clean control-equity playbook for this supercycle in Korea. Transmission is a KEPCO monopoly, so the regulated-grid stake KKR and PSP Investments took in American Electric Power — 19.9% for $2.82 billion — has no local equivalent. The equipment makers are large listed companies whose valuations already reflect the boom. The fragmented mid-market that lets a firm like Blackstone roll up bushing and switchgear suppliers in the US is far thinner here. The two playbooks that work elsewhere are both closed.

So equipment stops being a bet and becomes a lens. For investors underwriting Korean generation or data-center assets, the variable is no longer only the power price. It is whether the project owner can actually procure the transformers and switchgear that energize the connection, and when. In my experience, that question has never appeared in a Korean underwriting case; equipment simply arrived when needed, even through the global shortage of 2026. The exposure is sharper because Korean generation projects run on thin margins. Project IRRs around 9% leave little room for contingency, so equipment-price volatility hits a buffer that was never built to absorb it. That reshapes diligence: the question is no longer only whether grid connection is approved, but whether the project has reserved the transformer, switchgear, and cable slots to energize it.

Data centers carry the same variable with a regulatory twist. Foreign capital is already entering — Macquarie acquired a Hanam facility and launched a hyperscale platform with Gabia, and Digital Edge raised $1.6 billion for regional expansion. But the behind-the-meter workaround common in the US is constrained here. Korea’s direct PPA route is renewable-only: a data center can contract renewable power directly, but it cannot replicate the US gas-fired behind-the-meter PPA workaround as a simple bilateral power contract. Connection, and the equipment behind it, stays on the critical path.

One indirect exposure remains. Grid-balancing assets such as storage and pumped hydro may gain value as transmission slips, but that runs one step removed from the equipment itself — through the delay, not the hardware.

What to Watch

Three signals will tell you whether this moves from concern to cost. First, watch whether MCEE’s shift to three-year procurement and its localization push actually secure domestic volume. If they fall short, transmission slips further, and the GW-scale solar parks in the capital region and Gangwon — most dependent on new substations — feel it first in their commercial operation dates. Second, watch domestic equipment award prices. Once the export-domestic gap closes, generation projects with thin contingencies are where CAPEX room erodes first. Third, watch high-voltage component contracts like the Hyosung-Trench bushing deal. Each one signals where the schedule-critical dependency still sits, and which projects inherit it.

Equipment arriving on time was the one free option Korean projects carried without writing it into the model. That option is starting to cost something.

If your team is underwriting Korean power or data-center assets, equipment lead time belongs in the schedule-risk column — pass this to whoever owns the model.