The Revenue Reset: What Korea's Renewable Reform (RPS) Means for Every Clean Energy Investment

A third of project revenue disappears with the REC. At current auction prices, the math barely works.

DEEP DIVE

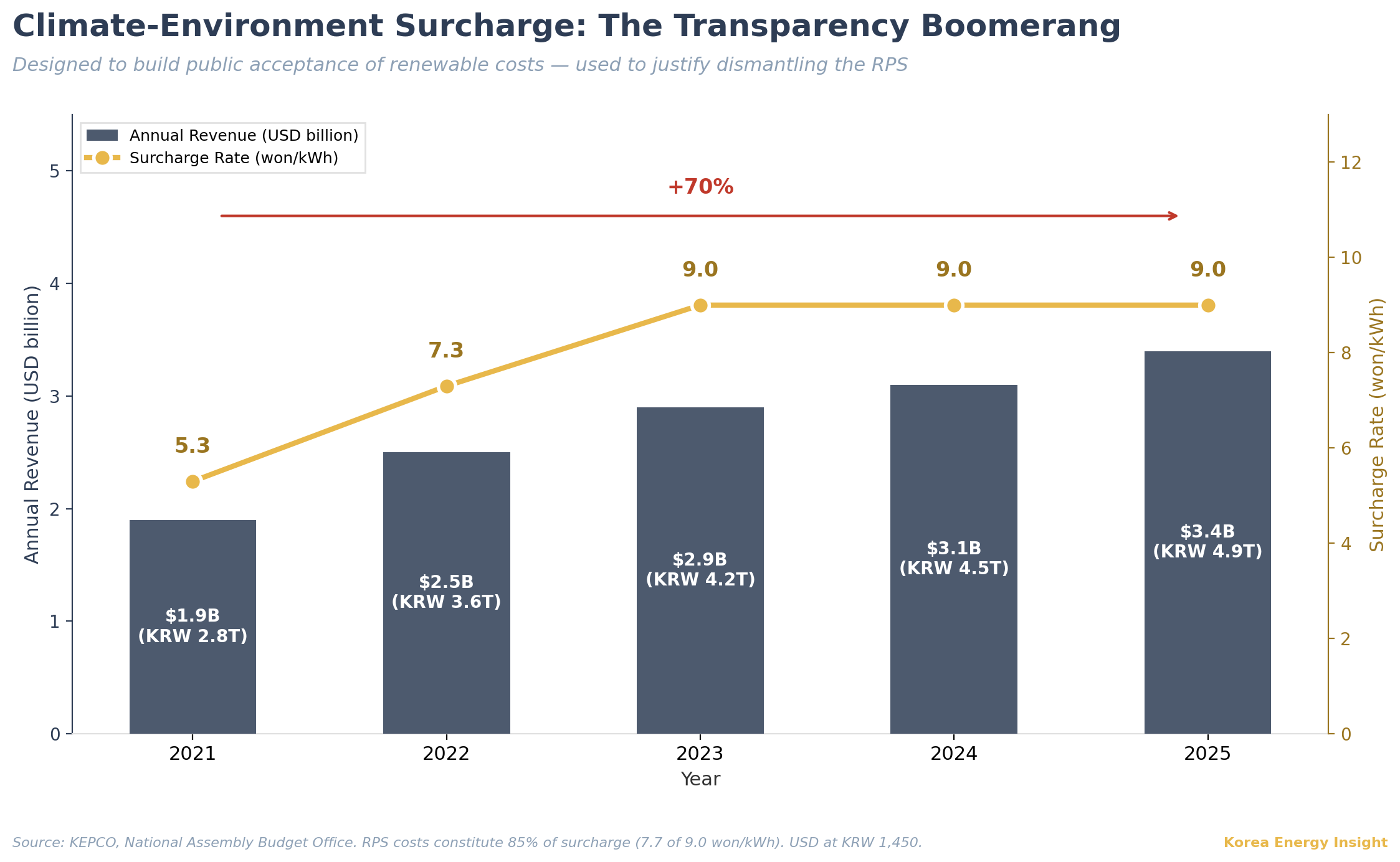

In 2021, Korea’s Ministry of Trade, Industry and Energy (MOTIE) made a deliberate choice: separate the cost of renewable energy support from the electricity bill and display it as a standalone line item. The new “climate-environment surcharge” (기후환경요금) started at 5.3 won/kWh. The logic was straightforward. Make the cost visible, and public acceptance of the energy transition would follow. MOTIE, Korea Electric Power Corporation (KEPCO), the Korea Power Exchange (KPX), and the Korea Energy Agency all endorsed the approach. I watched the consensus form firsthand.

Five years later, that surcharge has risen 70% to 9.0 won/kWh. Annual revenue grew from $1.9 billion (KRW 2.8 trillion; all USD conversions at approximately KRW 1,450/USD) to $3.4 billion (KRW 4.9 trillion) (KEPCO data, National Assembly Budget Office). The transparency designed to build support became the evidence used to dismantle the system.

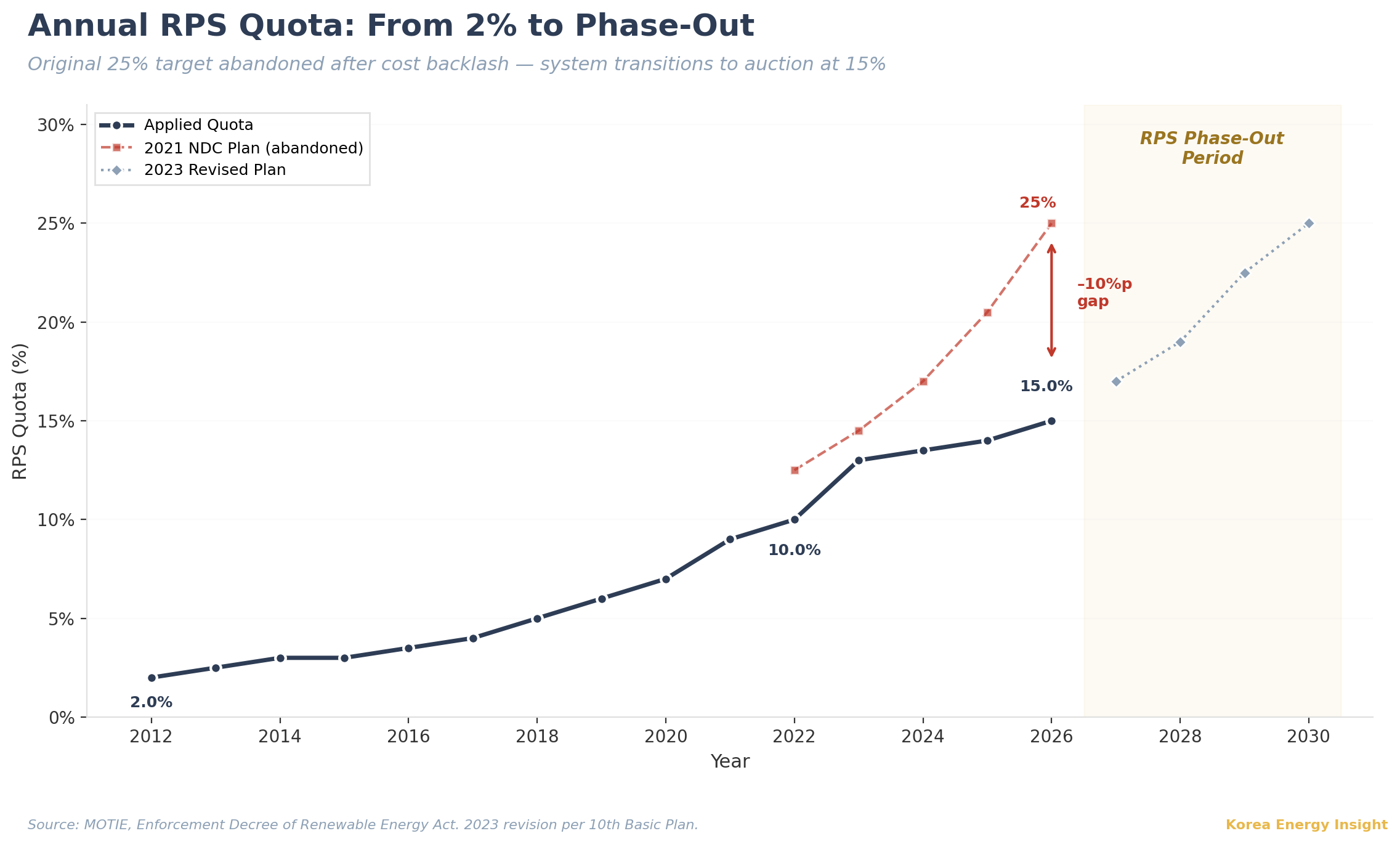

On February 12, 2026, the National Assembly passed amendments to the Renewable Energy Act that reorganized the legal framework, separating “new energy” (fuel cells) from renewables and rolling back local setback regulations. A companion bill by lawmaker Kim Jeong-ho, filed in January 2026, goes further: it proposes replacing Korea’s Renewable Portfolio Standard (RPS) with a government-led competitive auction and long-term bilateral contract market. That bill remains in subcommittee review, but the policy direction is set. The RPS, which has driven Korean renewable deployment for over a decade, is on track for phase-out by 2027. For every renewable asset in Korea, the revenue model that justified the original investment is being rewritten by the government that created it.

What Foreign Investors Are Comparing Against

The global benchmark for renewable support is the UK’s Contract for Difference (CfD). Allocation Round 7, whose offshore wind results were published on January 14, 2026, awarded 8.4 GW at a strike price of £91/MWh in 2024 prices. The contracts run 20 years with full CPI indexation. Settlement follows a pay-as-clear mechanism. The counterparty is the Low Carbon Contracts Company (LCCC), a government-owned entity with an investment-grade balance sheet separate from the national grid operator.

Korea’s new system shares the surface architecture: competitive bidding, long-term contracts, government oversight. The differences sit in the details that determine whether a project is bankable. No indexation clause has been announced. Contract duration is set at 20 years, but the price structure (pay-as-bid or uniform) remains undefined. The counterparty is expected to be KEPCO, carrying $82 billion (KRW 119–120 trillion) in standalone debt and $141 billion (KRW 205 trillion) consolidated. For a foreign infrastructure sponsor running a 20-year discounted cash flow, the absence of inflation adjustment alone can reduce contract value by 25–35% in present-value terms — relative to an indexed CfD at the same nominal strike price.

The Kim Jeong-ho bill proposes the detailed transition mechanism, including the REC phase-out timeline, transitional market operation, and small-project treatment. Subsidiary legislation covering auction design, price ceilings, and non-price evaluation criteria is expected in the second half of 2026. Until those details are set, the bankability gap between Korea’s auction and a UK-style CfD remains structural, not just procedural.

How the Current System Was Built — and Why It Broke

Korea’s RPS required 23 obligated entities — eight state-owned generation companies (KEPCO subsidiaries) plus 15 private generators above 500 MW, including SK Innovation E&S and GS EPS — to source a rising share of their output from renewables. Compliance meant either building renewable capacity directly or purchasing Renewable Energy Certificates (RECs) from independent developers.

The system’s early success depended on financial engineering. Banks and institutional lenders required long-term revenue certainty before committing project finance. MOTIE responded by introducing fixed-price REC contracts, typically 20 years, where developers locked in a combined SMP+REC price with an obligated utility. The mechanism made non-recourse project finance and post-COD refinancing market-standard for Korean solar. Between 2017 and 2021, the six state-owned generation companies spent $4.7 billion (KRW 6.86 trillion) purchasing RECs from external developers, with 68% of their RPS quota met through external procurement (Korea Energy Agency).

The system worked until the market moved underneath it. REC spot prices collapsed to $21/REC (KRW 29,981) in July 2021 as solar installations surged. Then they tripled to $56/REC (KRW 80,731) by September 2023 as RE100 corporate demand rose and the RPS quota ratio tightened. Developers who had locked in fixed contracts at 143–155 won/kWh (SMP+REC combined) watched spot-market peers earn 30–40 won/kWh more on the REC component alone. Some demanded contract termination. The buying utilities refused. Lawsuits followed.

The mirror image was equally damaging. When REC spot prices were high, developers refused to enter fixed contracts. The 2024 second-half fixed-price tender offered 1,000 MW. Only 80 MW bid in. Only 72 MW was awarded. It was the fourth consecutive under-subscription (Electimes, December 2024). The instrument built for bankability had become a trap nobody would voluntarily enter.

The cost side completed the loop. RPS compliance costs flow through to consumers via the climate-environment surcharge. That surcharge constitutes 85% of the total — 7.7 won out of 9.0 won/kWh. The National Assembly Budget Office projects renewable support costs could exceed $6.9 billion (KRW 10 trillion) annually within years. The bill proposing the RPS phase-out cites REC price volatility and consumer burden as primary justifications (National Assembly, February 2026). The official narrative is “global standard adoption.” The operational driver is cost control.

RE100 implementation compounds the problem. Korean companies participating in RE100 sourced 98% of their procurement volume through the “green premium” mechanism in 2024 (Korea Energy Agency). The green premium has been flagged as non-compliant with international Scope 2 accounting standards. With REC trading being converted to a non-tradeable “generation information certificate,” the remaining option is direct power purchase agreements. As of mid-2025, cumulative direct and third-party PPA contracts in Korea totaled just 1.7 GW (IEEFA). For manufacturers in global supply chains requiring verified renewable sourcing, Korea’s RE100 compliance options are not expanding. They are contracting to a single pathway that has barely started to develop.

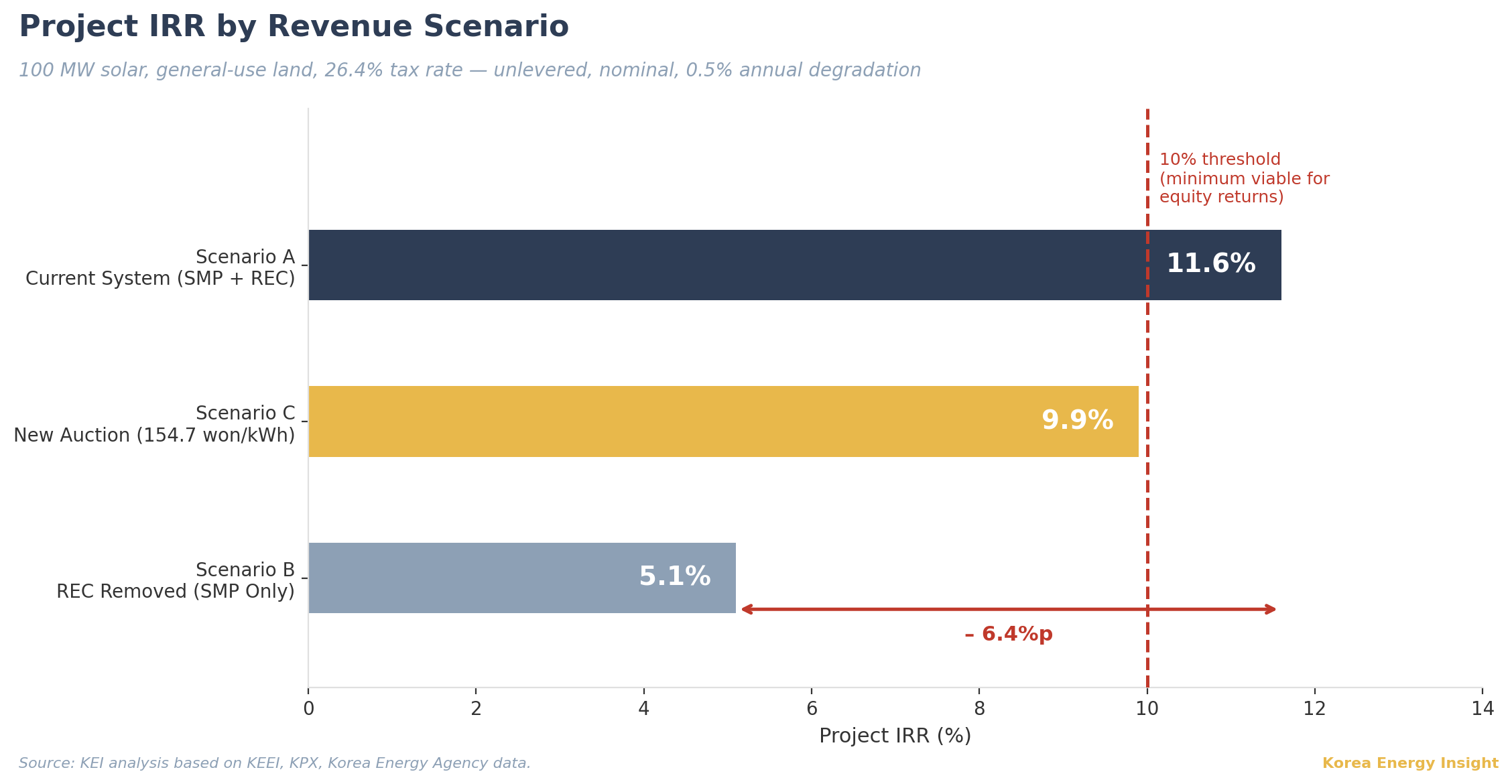

Simplified Valuation: What REC Removal Does to Project Returns

None of this matters to an investment committee without a number attached. Below is a simplified unlevered model for a 100 MW ground-mount solar project on general-use land, using 2025 market data (KEI analysis based on KEEI, KPX, and Korea Energy Agency published data). The model uses solar as the illustrative case, but the REC-dependent revenue structure applies equally to onshore wind (REC weight 1.2), offshore wind (2.5+), and biomass. Wind projects carry higher REC weights, meaning their revenue exposure to REC removal is proportionally larger.

Key assumptions: daily generation 3.4 hours (Korea average), REC weight 0.8 (general-use land, 3 MW+), 2025 integrated SMP 112.72 won/kWh, 2025 REC spot average approximately $50/REC (KRW 72,000), total CAPEX approximately $73 million (KRW 105.8 billion) including EPC at $0.73 million/MW (KRW 1.06 billion, KEEI 20 MW benchmark), 20-year life, 0.5% annual degradation, corporate tax rate 26.4% (24% national + 2.4% local; an SPC taxed at the lower 20.9% bracket would show higher returns). Permitting fees, grid connection costs, and supervision fees are included in total CAPEX. Financial leverage, inverter mid-life replacement (typically year 10–12), and solar capture-price discount are not modeled. All figures are nominal.

Scenario A — Current system (SMP + REC): Year 1 revenue approximately 21.1 billion won. Project IRR: 11.6%.

Scenario B — REC removed, SMP only: Year 1 revenue drops to approximately 14.0 billion won. Project IRR: 5.1%.

Scenario C — New auction at current fixed-contract level (154.7 won/kWh): Year 1 revenue approximately 19.2 billion won. Project IRR: 9.9%.

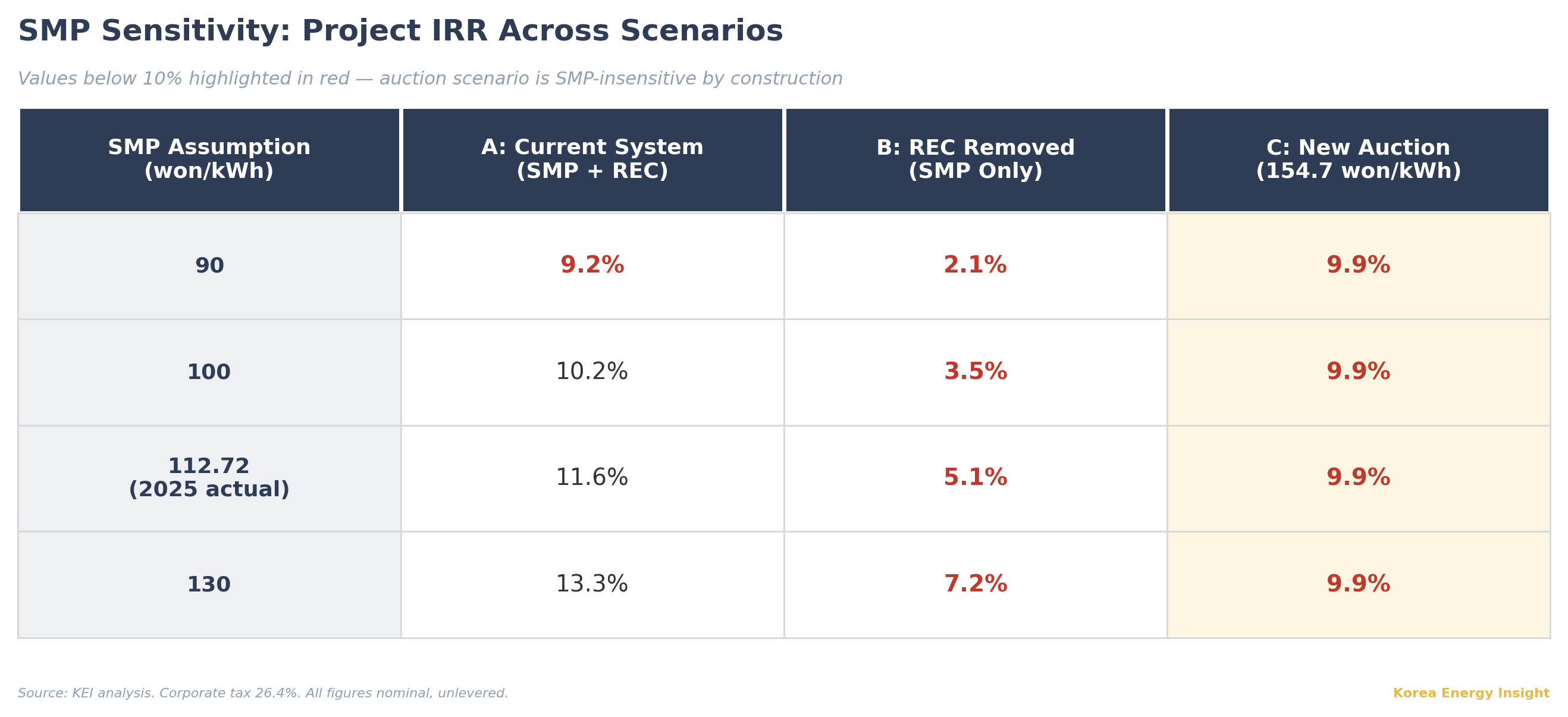

REC accounts for 33.8% of total revenue and roughly 37% of after-tax free cash flow. Removing it cuts the project IRR by 6.4 percentage points. To maintain the current IRR under the new auction system, the all-in contract price would need to reach approximately 170 won/kWh — 10% above the latest fixed-contract average and well above any publicly discussed ceiling.

The sensitivity to wholesale price makes the picture worse. If SMP falls to 90 won/kWh, plausible given the zero-price hours documented in Issue #4, the REC-removed scenario delivers an IRR of just 2.1%. The current merchant stack (SMP + REC) would still return 9.2% at the same SMP. The auction scenario, being SMP-insensitive by construction, remains at 9.9% regardless of wholesale price movements.

This model is deliberately generous. It assumes a flat 20-year price deck, no solar capture-price discount, no curtailment losses, and no inverter replacement reserve. In practice, each of those factors erodes returns further. Yet even under these favorable conditions, Scenario C delivers a project IRR of 9.9%. In renewable project finance, equity investors size their returns off equity IRR, not project IRR. With typical leverage (70–80% debt), a project IRR below 10% compresses equity returns below the hurdle rates that infrastructure funds require. The 9.9% in this model is not a comfortable margin — it is the floor, built on assumptions that real due diligence would discount. If the government sets auction ceilings below current fixed-contract levels to achieve its stated cost-reduction goal, the math does not work. Developers would not bid, repeating the under-subscription pattern that helped dismantle the RPS in the first place.

So What

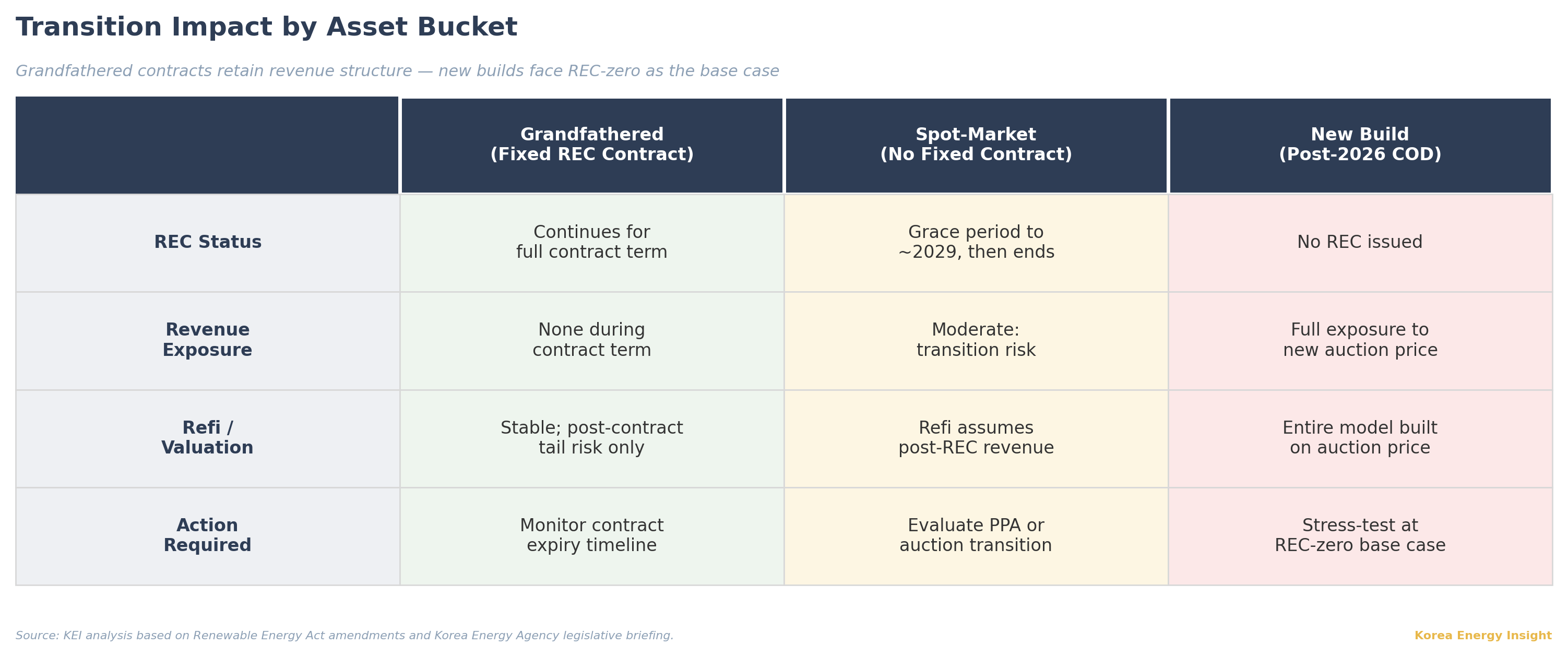

The transition does not hit all projects equally. Those with existing fixed-price REC contracts are fully grandfathered — REC issuance continues for the full contract term, meaning a 20-year contract signed in 2026 runs through 2046 under current terms. For these assets, the revenue structure is intact and valuations hold. Spot-market participants without fixed contracts have a shorter runway: a 2–3 year grace period (expected to end around 2029) during which REC issuance continues. After that, they must transition to either direct PPAs or the new contract market via a transitional market starting in 2027. The real exposure sits with new projects. Any facility reaching commercial operation after 2026 receives no REC. Its entire revenue case depends on the new auction system.

For portfolios holding Korean renewable assets, the immediate question is which bucket each asset falls into. Grandfathered contracts are safe for their remaining terms, but refinancing, secondary-market valuation, and contract-extension assumptions must now price in a post-REC revenue environment. For new entry, the REC-zero stress test is the base case.

The first auction results will determine whether the new system attracts capital or simply reorganizes existing players. Until then, every financial model built on the RPS framework needs to be rebuilt from the contract price up.

What to Watch

Subsidiary legislation (2026 H2): The auction’s price structure (pay-as-bid vs uniform), indexation clause, and settlement formula will determine whether this is a bankable CfD or an administered price cap. If indexation is absent, expect foreign sponsors to price Korean renewable assets at a discount to comparable UK or Taiwanese projects.

First auction clearing price — and whether it clears at all: If the initial auction clears below 155 won/kWh without indexation, the market will read it as a cost-reduction exercise. Watch whether developers bid aggressively or repeat the under-subscription pattern. Under-subscription would not signal market caution. It would signal that investment economics do not hold at the offered price.

Direct PPA market depth: With REC trading ending and green premium under international scrutiny, corporate RE100 demand must migrate to direct PPAs. The speed and depth of this migration determines whether solar project economics find a new buyer or face a demand vacuum.

KEPCO counterparty risk: The legislative briefing indicated KEPCO would serve as the single buyer. KEPCO’s standalone debt stands at $82–83 billion (KRW 119–120 trillion), consolidated at $141 billion (KRW 205 trillion). For 20-year contracts without sovereign guarantee, the counterparty’s credit trajectory is itself a bankability variable.

Community benefit-sharing and margin compression: The Sinan model requires 4% of total project cost or 30% equity participation for local communities, funded through additional REC weight premiums. Lawmaker Seo Wang-jin introduced a bill on March 20, 2026 to codify benefit-sharing nationally. Under the new auction system, REC weight premiums disappear — eliminating the funding source while the obligation may remain. Developers face margin compression from both sides: lower auction prices and unfunded community commitments.

Jeju negative bidding sustainability: Jeju’s isolated grid has produced negative-price bidding in the ESS central contract market, where operators accept below-cost contracts to secure grid access. If the renewable auction adopts similar dynamics, it would signal that the market is allocating losses rather than generating returns — a structural warning for any new entrant.

If this analysis is useful for your team’s Asia energy strategy, consider sharing it with colleagues evaluating Korean market exposure.