What Korea's Committee Reform Reprices: Regulatory Discretion

The risk in Korean thermal assets is the government's reach over settlement, not the spark spread.

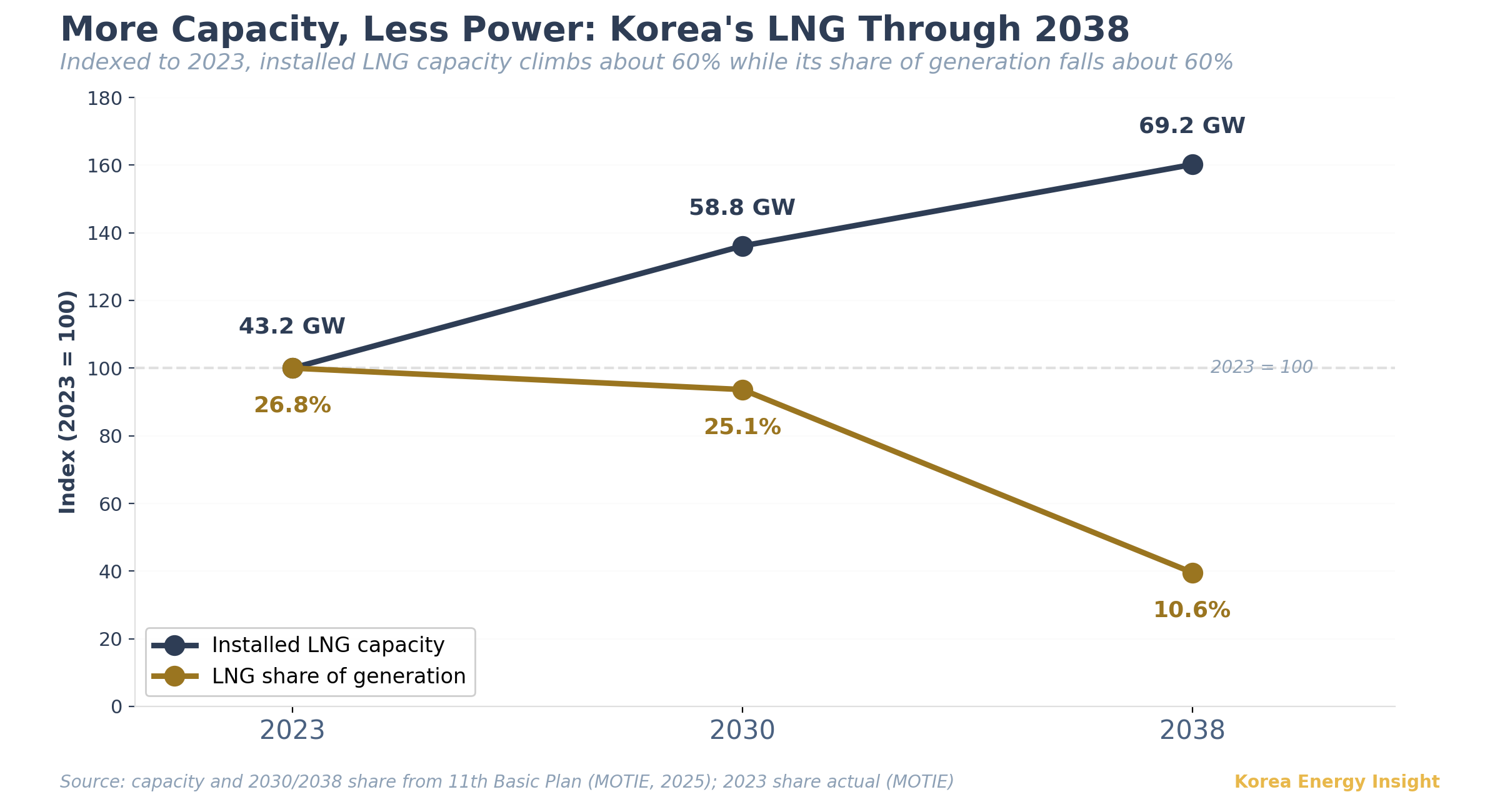

DEEP DIVE | Image: Korea Power Exchange

On June 16, the Korea Power Exchange (한국전력거래소, KPX) proposed to rebuild the Cost Evaluation Committee (비용평가위원회) as an expert-only panel, stripping out every market participant (전기신문). This is the committee that sets generator dispatch order and calibrates settlement in Korea’s wholesale market. KEPCO as buyer and the generation companies as sellers are removed, replaced by independent specialists in energy, finance, law, and IT, on the model of the US independent system operators (ISOs).

This is the same committee that, in October 2024, changed the settlement rules so current-year costs are recovered before accumulated receivables. Industry participants read that change as turning the East Coast private coal plants’ roughly $897 million (KRW 1.3 trillion; USD conversions throughout at approximately KRW 1,450/USD) of receivables into an interest-free balance with no fixed repayment date (전기신문; KEI Issue #24). The reform is presented as governance modernization. What it does is give the government a freer hand over the numbers that set generator revenue, and remove the one party with a reason to push those numbers up. For a fund underwriting a Korean thermal plant, the implication is direct: its cash flow is not priced in a market but calibrated by this committee, and the reform changes who sits on it.

The price Korea’s generators don’t set

The reference model is real. PJM, CAISO, and NYISO keep market participants off their governing boards, precisely so the buyers and sellers of power cannot write their own settlement rules. Independence from stakeholders is the global standard, and Korea citing it is not a stretch.

But in the US the excluded generator still sets its own price. Its energy revenue forms from the offers it submits; its capacity revenue from a capacity auction (PJM) or a resource-adequacy obligation (California); its ancillary revenue from co-optimized service markets. The board governs the rulebook, while the price itself forms in the market, so exclusion is fair: the excluded still set prices.

Korea’s generators do not. Their market is a cost-based pool (변동비 반영시장, CBP): a generator’s bid is the variable cost the committee has evaluated for it, not a price it is free to set, and SMP clears at that evaluated cost rather than at what a competitive market would pay. The generator never prices its own output; the committee that fixes the cost parameters does. So whoever controls the committee controls those numbers, and the reform hands that control to the government. Which raises the question that matters: what does the government want those numbers to do?

What the government wants

It wants two things from the wholesale market, and in Korea they are the same thing. It wants to hold down KEPCO’s losses, so it need not raise the politically sensitive retail tariff. And it wants to curb what private generators earn, the “excess profit” that draws political attention whenever margins are visible. These collapse into one objective, because KEPCO’s wholesale cost is the generators’ revenue: KEPCO buys power from generators and sells it to households, often below cost, so every won a generator earns is a won KEPCO pays. Compressing generator revenue is how the government shrinks KEPCO’s deficit. The Cost Evaluation Committee is the instrument that sets that revenue.

And it is not a neutral instrument. The reform replaces stakeholders with “independent experts,” but the proposal does not say who appoints them, and with the transacting parties gone that appointment most likely falls to the government. Even where it does not name members directly, few Korean statutory committees operate as neutrally as their charters imply. The Minimum Wage Commission’s deciding members are government-named, and the Korea Electricity Commission’s standing member is a sitting Ministry bureau chief, a structure long criticized at home as falling short of genuine independence. The reform does not create neutrality. It removes the one voice in the room that is not the government’s.

It has done exactly this before

The clearest evidence is recent. Through the 2022 fuel shock, KEPCO’s wholesale cost ran far above the frozen tariff, and its operating loss reached KRW 32.6 trillion. The government’s answer was the SMP cap (정산상한제): when the wholesale price ran high, KEPCO paid generators not the market price but roughly 1.5 times a ten-year average. It was introduced expressly to cut KEPCO’s deficit and restrain the tariff, and it did both by capping what generators received: the sell side suppressed to relieve the buy side, in a single move. Private generators fought it and some sued; the electricity commission approved it anyway.

The same intent sits in the permanent machinery. The settlement adjustment coefficient (정산조정계수), which sets how much of the margin between SMP and a plant’s cost the plant is allowed to keep, is capped at 1.0, so it can pull a generator’s revenue back toward cost but never above the market price. The fuel cost pass-through (연료비 연동제), built to move fuel costs into tariffs automatically, was suspended whenever it would have raised them. The most visible case came before the 2022 election, when the formula indicated a 29.1 won/kWh adjustment and the government held the applied rate at zero. The pattern is consistent: where a rule would lift what KEPCO pays or what households are charged, it is capped, deferred, or overridden. The committee reform widens the discretion to keep doing it.

Private generators want the opposite

What private generators need runs directly against that, and it runs through the same committee. Their claim rests on a feature of the market that is easy to miss: almost nothing in Korean wholesale settlement is paid at a plant’s actual cost. It is a conceptual settlement, theory fitted to practice. Even SMP, the marginal price built from generators’ cost-based bids, runs on standardized variable costs rather than the fuel a unit actually burned. That is the premise behind the demand: when the numbers are constructs, “realization” (현실화) means pulling them toward present reality.

It matters more each year. As renewables push Korea’s SMP toward zero on spring afternoons (KEI Issue #4), the energy market thins as a revenue source, and a generator’s return migrates onto three administered numbers the committee sets: the capacity price, the ancillary services settlement rate, and the recovery basis for Renewable Portfolio Standard (RPS) obligation costs. These have become the private generator’s profit and loss, and on each one, the figure generators want lifted is the “excess profit” the government means to curb.

They want the capacity price made realistic, because it is still pinned to the investment cost of the Shin-Incheon gas turbine alone (the turbine, not the full combined cycle), so it understates what a new plant costs to build. They want ancillary settlement priced at the real cost of holding capacity in reserve. LNG combined cycle already earns about 72% of the country’s $394 million pool there (KEI’s aggregation across KPX settlement disclosures, not a single reported category). Even so, operators argue the rate understates what reserve is worth, because it is set administratively rather than cleared in a market. And they want fuller recovery of their renewable-obligation costs. The government’s direction on all three is the reverse: hold the capacity price down as the Basic Plan (전력수급기본계획, Korea’s binding power-supply plan) strands LNG, open ancillary to storage and demand response that compete the rate down, and return obligation costs more slowly.

The generators’ case is not disinterested. The market-economics banner they raise cuts both ways. A settlement priced at true scarcity can over-reward as easily as under-reward. And when actual-cost pricing would run against them, the same operators reach for grid stability to argue against the market they otherwise invoke. The demand to make the numbers realistic is legitimate; so is the self-interest in which way “realistic” resolves.

None of those arguments is guaranteed to lose. But each must now be made to a government-appointed, fiscally disciplined committee with the generators’ own seat removed, the same year the 12th Basic Plan, written by the Ministry of Climate, Energy and Environment (기후에너지환경부, MCEE), redefines how large a role LNG is allowed to play.

What is actually being repriced

The market has read the most important implication backwards. The bull case on Korean LNG combined cycle (including the one this newsletter has made) is that grid services create a revenue floor that energy-margin models miss, as synchronous generation leaves the system and inertia and voltage support grow scarce (KEI Issue #12). That floor is real. But it is an administered floor, set by a committee whose controller wants it lower. The flexibility is needed; the question is whether Korea pays for it through transparent scarcity pricing or through a committee-set minimum that tightens when KEPCO’s balance sheet requires. An investor counting on that upside is really betting on which path the government takes.

Private coal is the nearer-term exposure. The East Coast plants already carry receivables repaid only from the headroom under the settlement coefficient’s 1.0 ceiling, interest-free, while grid-constrained non-dispatch earns no separate compensation (KEI Issue #24). They sit most directly under the committee losing its only generator voice, and their settlement is where a tighter calibration shows first.

What is being repriced is not generation economics but regulatory discretion. For a foreign fund, the real exposure in a Korean thermal asset was never the spark spread; it was KEPCO’s balance sheet and the government’s reach over settlement. This reform widens that reach and narrows the channel to contest it. The models still price the spark spread; the risk has moved to the committee.

What to watch

Whether the Rule Amendment Committee passes the proposal this month, and on what timeline. If it passes without a phased transition, the next round of capacity, ancillary, and obligation-cost calibration happens with no generator input.

The reference capacity price and the capacity-market transition. Whether the next setting moves up toward what a new plant costs or down toward the decarbonization case is the clearest read on which way the government pushes the lever.

The ancillary services market build-out. If reserve and reactive-power services move to competitive pricing, LNG’s administered 72% capture erodes regardless of who sits on the committee.

The 12th Basic Plan’s treatment of LNG, due by year-end. Confirm the decline path and the upside case for capacity and ancillary reform narrows with it; let energy-security pressure win and the constraint loosens.

Bid sophistication (입찰고도화) on the same rule-making track. Its current content is narrower: day-ahead re-bidding rules and reserve products, not free offers. Watch whether it moves toward genuine offer-based pricing, the one change that would hand generators a lever outside the committee.

Bond spreads on the East Coast coal issuers, the market’s running read on how much discretion risk is priced.

If this is useful for your team’s read on Korea market entry, consider forwarding it to colleagues weighing Korean power assets.