Korea's 1.8GW Offshore Wind Auction: The Money Will Show Up. The Permits Won't

Korea just opened its largest offshore wind auction. The real question is how many winning bids will ever reach construction.

MARKET SIGNAL

The Headline

On March 30, the Ministry of Climate, Energy and Environment (기후에너지환경부) announced a 1,800MW offshore wind competitive auction for the first half of 2026 — 1,400MW bottom-fixed, 400MW floating. The cap price for bottom-fixed came in at 171.2 won/kWh, down 3% from last year. Floating was set at 175.1 won/kWh, separated from bottom-fixed pricing for the first time. If all awarded capacity moves to construction, the pipeline represents over $8.3 billion (12 trillion won) in investment. Industry and government officials expect bidding competition above 2:1.

That expectation is probably right — but for the wrong reason. The rush toward this auction is not driven by improving offshore wind economics. It is driven in part by the government’s planned phase-out of the current Renewable Portfolio Standard (RPS) framework, with policy materials pointing to end-2026 as the key cutoff for new REC issuance. Once the RPS framework changes, the current template of 20-year fixed-price contracts combining the System Marginal Price (SMP) and Renewable Energy Certificates (RECs) weakens or disappears entirely. Developers are not bidding on wind farms. They are bidding on the last available contract structure.

By industry count, around ten projects with completed environmental impact assessments are waiting to enter. The auction will likely be oversubscribed. The problem starts the day after the awards are announced.

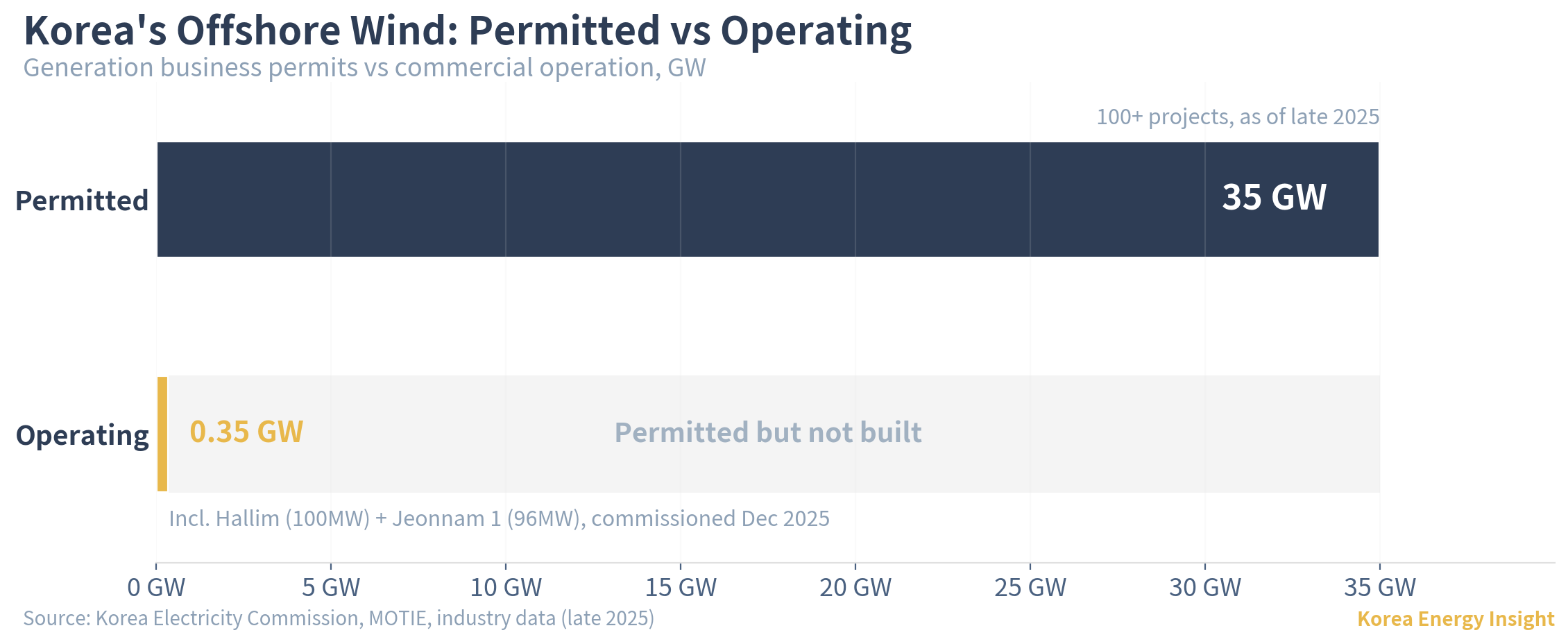

Two Walls Between Permit and Shovel

Korea’s offshore wind pipeline looks impressive on paper. As of late 2025, over 100 projects totaling more than 35GW have received generation business permits (발전사업허가) from the Korea Electricity Commission (전기위원회). Actual installed and operating capacity tells a different story. Including the recently commissioned Hallim (100MW) and Jeonnam 1 (96MW), Korea’s total operating offshore wind stands at roughly 0.35GW. After a decade of permitting, the country has 35GW approved and 0.35GW operating.

The gap is not about capital — Korean and global developers have committed billions to this pipeline. It is about two permit barriers that money alone cannot resolve.

The first is military operations clearance (군 작전성 평가). Of 87 permitted offshore wind projects as of August 2024, only 14 have received Ministry of National Defense approval. According to industry and press accounts, most of those cleared only the Air Force’s radar interference review, without a full Navy operational assessment. The Navy conducted a separate impact study in 2025 and the interim finding was blunt: offshore wind could cause “severe adverse effects” on naval operations. Press reports say the Ministry of National Defense has since treated the issue as non-negotiable. The reason runs deeper than inter-ministry politics. Korea remains technically at war with North Korea under a 1953 armistice, and the West Sea is an active front — military authority over coastal zones carries weight that no civilian ministry can override.

The problem is concentrated in that same West Sea, which is also Korea’s most attractive offshore wind site — shallow waters and moderate wave conditions make it ideal for bottom-fixed installation. Yet the Agency for Defense Development (ADD) maintains weapons testing zones there, overlapping what industry estimates at 10GW of planned offshore wind, more than half of the 11th Basic Plan’s 18.3GW wind target for 2030. At least one global developer with a valid permit abandoned its West Sea project entirely and began searching for alternative sites in the EEZ. The military clearance problem was so unexpected that some developers have started building dedicated military-liaison teams from scratch, a function that never existed in Korean renewable energy organizations.

The 2026 auction introduces pre-auction military consultations for ten projects, and the Offshore Wind Special Act (해상풍력특별법), enacted by bipartisan consensus in February 2025 and effective March 26, 2026, creates a Prime Minister-level committee to coordinate 42 permit requirements across ten ministries. But the roughly 104 “transitional projects” permitted before the Act are not automatically folded into the new framework.

The second barrier is fishermen’s compensation (어민 피해보상). Korean coastal waters suitable for offshore wind overlap with active fishing grounds at rates exceeding 90% in some permitted areas. No standardized compensation framework exists. Developers negotiate bilaterally with fishing communities, and the boundary between direct and indirect impact zones is undefined. The pattern repeats across every major project site. In Yeonggwang, the 532MW Anma project moved to permitting with only 13% consent from local fishing vessels, triggering protests that reached the presidential office. Developers offered 20 million won per vessel; fishermen demanded 50 million. In Ulsan, compensation for the 1.125GW KFWind seabed survey reached only 50–60 vessels while 780 fishermen in the local union were excluded. Jeju’s 2.37GW Chuja project collapsed twice — Equinor and then KEPCO subsidiary KOMIPO both withdrew — with annual community benefit demands of $90 million (KRW 130 billion) and Jeju’s grid interconnection constraints cited among the factors.

The Special Act mandates consultative councils with fishing representatives holding at least half of seats for new planned sites. For the 104 pre-existing projects, however, no such structure exists. Fishermen in those areas face the same developers, the same disputes, and the same absence of standardized rules they had before the law was written.

Why This Matters Beyond Wind

Offshore wind is how the current government plans to stop Korea’s renewable build from becoming a solar-only story. Onshore wind offers little relief — most commercially viable sites are already developed or face their own permitting and community resistance constraints. The 11th Basic Plan targets 40.7GW of wind by 2038, most of it offshore. If the permit walls described above prevent that capacity from materializing, the gap does not stay empty. It is likely to tilt further toward solar — because solar has what offshore wind in Korea still lacks: bankability. Solar PV projects have standardized financing structures, a two-decade domestic track record, and predictable permitting timelines. When institutional barriers block one asset class, money moves to the one that closes.

A more solar-concentrated grid is the likely result. That accelerates the intermittency problem Korea is already facing — SMP hit zero for 26 hours between January 2025 and March 2026, all during daytime solar peaks (KEI tabulation of KPX hourly settlement data). More solar without proportional wind means wider daytime surpluses and steeper evening ramps, which in turn increases the required investment in grid-balancing infrastructure: pumped hydro, long-duration ESS, synchronous condensers, and the ancillary service payments to keep them running. Korea’s grid stability bill, $390–400 million (KRW 571.6 billion) in 2024 settlement, grows faster if offshore wind underdelivers. For investors positioning around Korea’s energy transition, a stalled offshore wind pipeline is not just a wind-sector problem. It raises the implied value of every grid-balancing asset on the peninsula.

None of that changes the near-term auction dynamics.

What I’m Watching

Base case: The auction attracts strong competition. RPS sunset pressure guarantees that. But post-award attrition will be high. Bottom-fixed projects with pre-cleared military consultations have the best chance of reaching construction. Floating projects face the compounded risk of immature domestic supply chains, a cap price that industry participants consider below expectations, and the precedent set by Bandibuli, the first project selected in Korea’s floating offshore wind auction in late 2024, which failed to sign an REC purchase contract and stalled.

What I’m watching: Whether any floating project clears the REC contract stage within six months of award — the step where Bandibuli failed. The second-half auction volume and cap price trajectory, which will signal whether the government views the first-half results as a baseline or a ceiling. And the pace of military consultation completions for pre-existing West Sea projects, which will determine whether the 10GW pipeline there is recoverable or effectively stranded.

What would change my mind: If the Prime Minister-level coordination committee resolves a military clearance dispute for a major West Sea project before year-end, it would signal that the institutional machinery created by the Special Act has real enforcement authority — not just coordination power. That has not happened yet.

If this analysis is useful for your team’s offshore wind strategy in Korea, consider sharing it with colleagues.