Korea-Japan's Summit-Backed LNG Cooperation: Buyer Coordination Begins to Reshape LNG Pricing

Spot cargo swaps are already real. The open question is whether they extend into strip and term procurement.

DEEP DIVE | Image: President Lee Jae-myung of Korea and Prime Minister Takaichi Sanae of Japan at the Korea-Japan summit, Andong, May 19, 2026. (Source: Office of the President, Republic of Korea)

Opening

The Korea-Japan summit on May 19 in Andong produced four energy agreements: crude oil and petroleum product swaps, LNG cooperation, the Supply Chain Partnership (SCPA) on critical minerals, and Korea-Japan exploration of cooperation under POWERR Asia. Korean coverage framed the meeting as the latest installment of shuttle diplomacy. Japanese coverage placed it within Tokyo’s revised Free and Open Indo-Pacific strategy — “two pillars” of cooperation anchored in FOIP thinking, in the Japanese foreign ministry’s wording. Both readings are accurate. Neither captures the market consequence: how the agreement could change LNG price formation.

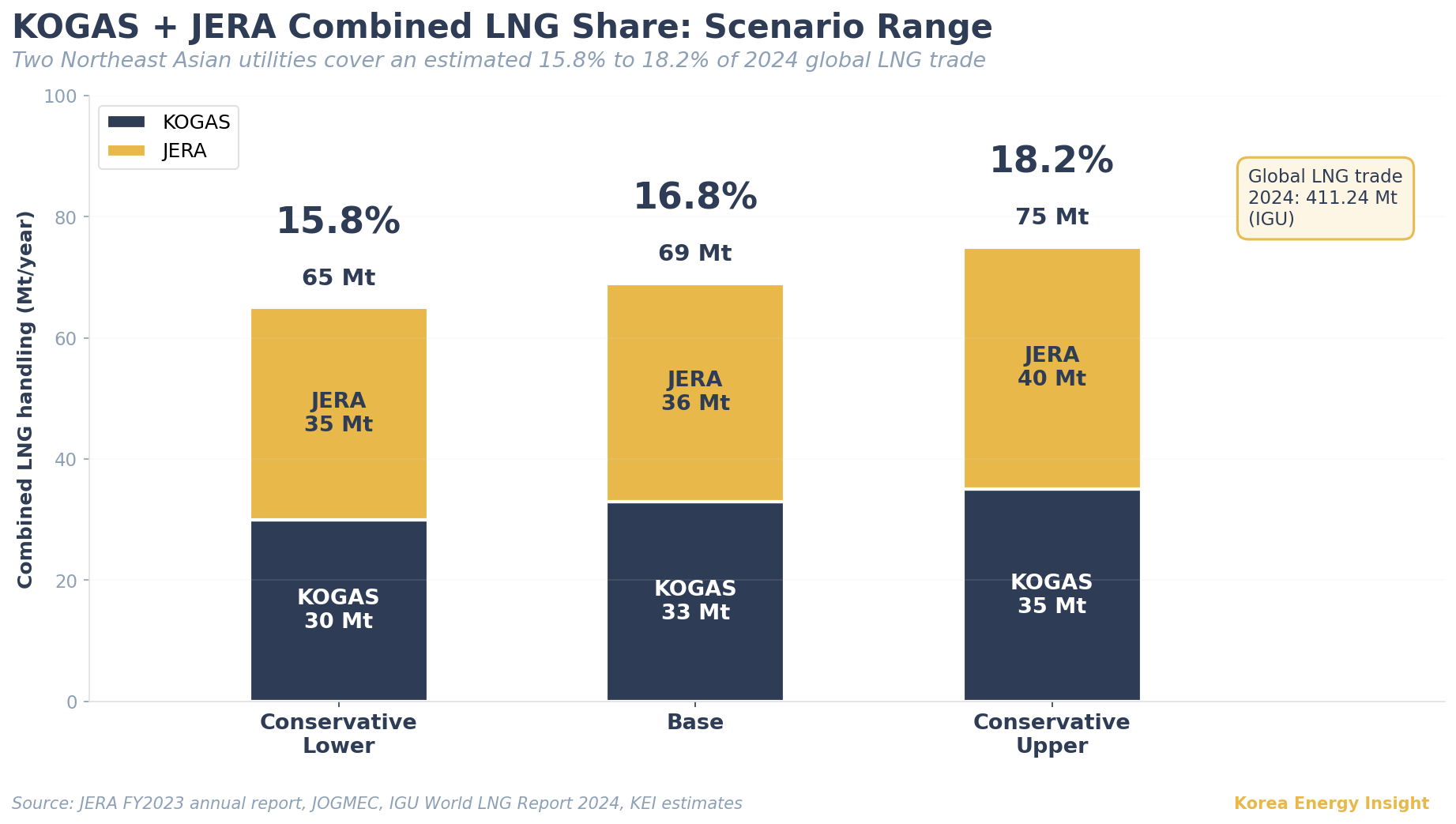

The market impact concentrates in one stream. KOGAS and JERA, the two largest corporate LNG buyers in Northeast Asia and jointly accounting for roughly 15-18% of global LNG trade, have been building operational cooperation since April 2023. The March 2026 Operation Cooperation Agreement, signed with both energy ministers in attendance, names six cooperation areas: operations optimization, supply-demand information exchange, cargo swap expansion, joint procurement consideration, trading cooperation, and supply crisis response. The Andong summit elevated that framework to leaders’ diplomacy. What changes is the price formation environment across spot, strip, and term cargoes. How far that change reaches depends on whether political backing turns into recurring cargo planning. The effect is not global price control. It is a buyer-side coordination layer that could influence spot scarcity premiums, strip cargo discounts, and term-contract optionality across LNG pricing layers. The same procurement channel later feeds into Korean SMP and KEPCO through KOGAS’s wholesale gas price.

Cooperation That Accumulated, Then Got Political Cover

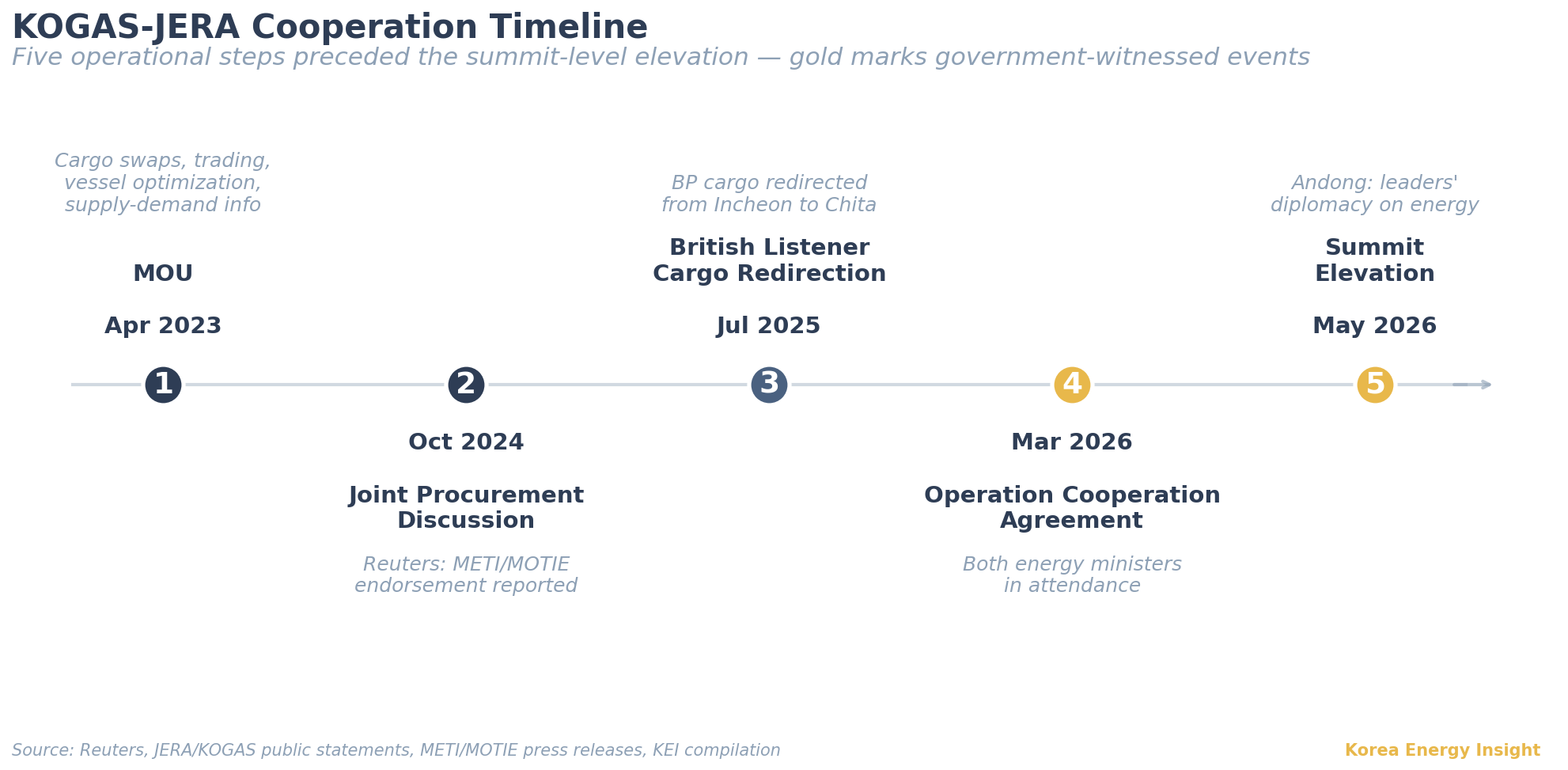

The summit mattered because the operating track already existed. KOGAS-JERA cooperation accumulated across four operational steps before reaching the summit table.

The April 2023 MOU named four cooperation areas: cargo swaps, trading, vessel optimization, and supply-demand information exchange. In October 2024, Reuters reported that joint procurement and cargo swap opportunities were under active discussion, with both METI and Korea’s industry ministry endorsing the framework. In July 2025, the BP-operated British Listener, originally destined for KOGAS’s Incheon terminal, was rerouted to JERA’s Chita terminal. A KOGAS spokesperson publicly confirmed the broader swap operation, though both companies declined to officially confirm this individual cargo as a cooperation milestone. In March 2026, the two companies signed an Operation Cooperation Agreement (referred to by JERA as an MOU on LNG operations cooperation) with both energy ministers in attendance. The May 2026 summit added the fifth step: leaders’ diplomacy. This is the first time bilateral energy cooperation between KOGAS and JERA has been formally elevated to summit-level agenda.

The important point is not that all three layers will move at once. It is that the March agreement gives each layer a different entry point. The agreement does not guarantee movement across all three layers, but it creates a route into each of them. Cargo swaps and supply-demand information sharing operate at the spot level. The trading cooperation language opens a pathway into the strip segment, where portfolio sellers such as Shell, BP, TotalEnergies, and ExxonMobil offer discounts to volume buyers, and where coordinated tendering could produce the fastest observable price effect. Joint procurement consideration creates an option at the term-contract layer, where Qatari NFE and US second-wave SPAs are now being negotiated. Whether the cooperation actually realizes across all three layers, or stops at the operational coordination stage, is the open question. What started as operational hedging between two utilities has become a framework that touches every channel through which LNG prices form in Northeast Asia.

The timing matters because LNG supply is becoming more flexible at the same time buyers are starting to coordinate. The IEA expects roughly 300 billion cubic meters of new LNG capacity to enter the market over the next five years, with around 75% contracted on flexible terms: resaleable, divertable, and increasingly indexed to Henry Hub rather than oil. TTF-Asian spot correlation reached its highest level on record in 2025. Supply-side flexibility is rising. The Korea-Japan move adds demand-side coordination at the same moment. Together, they could reduce the marginal role of unscheduled spot purchases in LNG price formation.

The Buyer Power Math

JERA reports annual LNG handling of roughly 35-40 million tons, with FY2023 at 36 Mt. KOGAS’s 2024 total LNG imports are not directly disclosed in publicly accessible reports. Applying JOGMEC’s estimate of a 78.8% KOGAS share to IGU’s reported 47.01 Mt of Korean imports yields a point estimate near 37 Mt. Accounting for direct importer growth, a conservative band of 30-35 Mt is appropriate.

Across scenarios, the combined share lands between 15.8% (JERA 35 Mt + KOGAS 30 Mt) and 18.2% (JERA 40 Mt + KOGAS 35 Mt). The base case is approximately 16.8%.

Market share alone does not make the cooperation market-moving. The decisive variable is concentration in spot demand. Northeast Asian spot LNG demand — cargoes not under long-term contract — is concentrated among the same two buyers, who account for a material share of regional spot purchases. This is the segment where price discovery happens. JKM, the Platts-assessed marker, reflects spot transaction prices in this market. When KOGAS and JERA coordinate their spot exposure, JKM’s formation conditions shift.

Cargo unit economics make this concrete. Korean utility KOSPO’s 2025 spot tender cargoes ranged from 3.0 to 3.7 TBtu each. Reallocating just two or three cargoes during a tight winter or supply-disrupted week can defuse a shortfall that would otherwise force premium spot purchases. The January-February 2024 cold snaps in Northeast Asia drove JKM above $13/MMBtu before easing. The March 2026 Hormuz disruption pushed JKM to $25.39/MMBtu, with April 2026 averaging $17.92. Both KOGAS and JERA were active spot buyers in these episodes. With coordinated inventory and cargo management, the same shortfalls would be partially resolved through internal reallocation rather than competitive bidding.

How This Reshapes JKM Formation

KOGAS-JERA cooperation does not set JKM directly. It changes the conditions under which JKM forms. Four transmission channels matter.

First, spot tender frequency could fall if coordination becomes routine rather than event-driven. When two large buyers go to the spot market separately to cover short positions, they bid against each other and against smaller players. Fewer simultaneous tenders would reduce visible prompt demand pressure. The more important effect is lower upside bidding pressure during tight windows.

Second, the scarcity premium is where the first measurable compression would appear. The gap between average JKM and peak JKM is the first place where the effect should show. Cargo reallocation between Incheon and Chita does not affect quiet-market price levels. It affects what JKM does when one buyer faces a sudden shortfall in a tight market. With internal cargo flexibility, the premium that would have appeared in spot bids is partially absorbed inside the cooperation. Winter and crisis-window spikes become shorter and shallower.

Third, strip and term contract leverage strengthens only if coordination moves from cargo swaps into supplier-facing negotiation. The strip segment, where portfolio sellers package quarterly and semi-annual cargoes, is where coordination produces the fastest observable unit-price effect: volume aggregation translates directly into seller discounts without the multi-year commitment of an SPA. Term contract leverage matters separately. Qatari NFE marketing and the US second wave — Plaquemines Phase 2, Rio Grande, Port Arthur, CP2 — are negotiating long-term contracts now. Two coordinated buyers can improve their bargaining position on destination flexibility, resale rights, and indexation terms that neither could negotiate as effectively alone. Suppliers facing a coordinated buyer block may see pressure appear first in indexation slopes and tolling fees rather than in headline LNG prices. The first observable test will be the next Qatari NFE long-term contract, or a coordinated strip approach to a portfolio seller, whichever surfaces first.

Fourth, TTF-JKM linkage redistributes flows. Over 2023-2026, the correlation between Asian LNG spot proxies and European TTF prices reached approximately 0.93, compared to roughly 0.05 with Henry Hub. The dominant link in Northeast Asian LNG pricing today runs through Atlantic-Pacific arbitrage with Europe rather than through US gas supply. If KOGAS-JERA coordination reduces the frequency of extreme Asian spot premiums, the Atlantic-Pacific arbitrage signal changes. Some cargoes that would otherwise chase Asia’s peak premium could remain in, or be redirected toward, Europe, depending on freight, storage, and portfolio positioning.

The headline JKM level may move only modestly in calm conditions. The variability of JKM and the leverage embedded in long-term contracts should shift more visibly. For procurement budgeting, that variability and that leverage matter more than the average.

Implication for Korea: SMP Downside and KEPCO Recovery

The most concrete implication runs through KOGAS’s wholesale gas price to LNG-fired generators. At approximately KRW 1,450/USD and a 6.5 MJ/kWh CCGT heat rate, a $1/MMBtu fuel-cost change translates into roughly KRW 8.9/kWh. A $1.0-1.5/MMBtu improvement would therefore imply roughly KRW 9-13/kWh of variable-cost relief for LNG CCGTs, with SMP impact concentrated in hours when LNG sets the marginal price. This is a sensitivity, not a forecast.

One detail matters for how this transmits. KOGAS’s accumulated receivables — approximately KRW 14 trillion in unrecovered cost — sit on the city gas side of its tariff structure, not the power generation side. The wholesale gas price KOGAS charges to LNG-fired generators adjusts on a quarterly cycle and is not buffered by the city gas receivable backlog. Import cost relief on the power side passes through to SMP without the cross-subsidy drag that complicates city gas tariff adjustments. The directional signal to SMP is cleaner than headline KOGAS financials suggest.

For KEPCO, still recovering from cumulative operating losses of approximately KRW 43 trillion ($30 billion; all USD conversions at approximately KRW 1,450/USD) accumulated through 2022-2023, this matters at the margin. For credit investors, the relevant read-through is not immediate earnings recovery but lower fuel-cost volatility at the margin. The qualifier sits in the timing. Import cost changes typically reach SMP after a 1-2 quarter lag, and the speed of pass-through depends on KOGAS’s wholesale price adjustment cycle and any intervention at the Ministry of Trade, Industry and Resources.

Implication for Korean Direct Importers

The second implication, less visible in market commentary, concerns Korea’s direct LNG importers. SK Innovation E&S is the largest, with an integrated portfolio spanning a 37.5% stake in the Barossa gas field, tolling capacity at Freeport LNG, and downstream gas-fired generation. POSCO International, GS EPS, SK Gas, Boryeong LNG Terminal, and smaller players make up the rest, with the direct import segment as a whole accounting for roughly 30% of Korean LNG imports.

With one exception, none of these companies has a Japanese counterparty matched to them. Japan’s LNG market is consolidated around JERA, Tokyo Gas, and Osaka Gas — utilities structured differently from the trader-importer model Korean direct importers represent. The government-blessed channel runs through KOGAS-JERA. Direct importers sit outside it.

The exception is SK Innovation E&S itself. The company holds the Barossa upstream stake alongside Santos (50%) and JERA (12.5%), and shares operational exposure with JERA at Freeport LNG. SK Innovation E&S already has an asset-level joint exposure with JERA that other Korean direct importers do not. Whether this translates into inclusion in the KOGAS-JERA government umbrella, or runs as a parallel private channel, is one of the key open questions for the next twelve months.

For the rest of the direct importer segment, the risk is not that they immediately pay more for LNG. The risk is that KOGAS gains a government-backed flexibility channel that independent importers cannot replicate. They continue negotiating alone, while suppliers may have less reason to price Korean direct importers as an independent counterweight to KOGAS’s pricing power. Korea’s LNG market is showing signs of a re-utility-ization that runs counter to the 11th Basic Plan’s direct import expansion narrative. In other words, procurement flexibility shifts back toward regulated utility channels rather than merchant importers.

The same asymmetry appears at the asset level. Assets connected to the KOGAS-JERA flexibility channel gain optionality; assets outside it rely more heavily on their own contracts, storage, and shipping flexibility. The same logic changes how infrastructure should be underwritten. Not all LNG assets benefit symmetrically. Contract-based regasification terminals see clearer upside from reduced procurement risk premium. Gas-fired generation benefits more selectively, depending on fuel cost pass-through, SMP exposure, and contract structure. Merchant LNG storage, which earns on winter-summer spread and tail premium, could face modest headwinds if coordination actually compresses those premia. Regasification terminals, LNG storage, and the underlying long-term shipping contracts begin to carry option value that the textbook capacity model does not capture. The value is conditional: it becomes real only when cargo redirection, slot sharing, or inventory support is documented.

For PE and infrastructure funds underwriting Northeast Asian LNG assets, the modeling variables shift. Beyond regasification capacity and contractual throughput, four operational questions enter: whether a terminal can accept cargo redirections from partner facilities, how much storage flexibility exists to lend inventory, what scheduling flexibility vessels carry for last-minute destination changes, and what destination flexibility sits in the underlying long-term contracts. This is a secondary repricing alongside the primary transmission to JKM and Korean power markets, but for asset-level underwriting it is the line that the cooperation most directly opens.

Validation Signals

The thesis does not require a full joint procurement pool to be right. It requires evidence that KOGAS and JERA are converting political cover into operational coordination across both spot and term segments. Three signals matter.

First, regular supply-demand coordination. If KOGAS and JERA establish a standing operations committee or regular cargo-planning process, the cooperation has moved beyond event-driven swaps. Cargo visibility, inventory support, and vessel scheduling become operating routine rather than ad hoc crisis management.

Second, documented supplier coordination. Evidence could appear at three levels: a coordinated spot tender, a joint strip package approach to a portfolio seller, or aligned term-contract negotiation language with Qatar or a US second-wave supplier. Any of these would mark the transition from swap framework to buyer block, with the strip case likely to surface first given its shorter commitment horizon.

Third, crisis-window price behavior. The test is not average JKM. It is whether Northeast Asian spot premiums during winter peaks or supply disruptions become shorter and less severe than past patterns would suggest. If forced buying episodes decline visibly, the cooperation is showing up in price formation.

A secondary signal concerns Korean direct importers. Whether SK Innovation E&S, POSCO International, GS EPS, SK Gas, and others can access a comparable flexibility channel — or whether KOGAS becomes the only Korean buyer with a government-backed regional option pool — will signal how Korea’s LNG market structure reorganizes around the cooperation. SK Innovation E&S’s choice carries unusual weight given its existing JERA asset-level exposure.

What the Andong summit added was institutional weight. The framework had been accumulating since April 2023, and the four operational steps that preceded the summit suggest the trajectory will continue. The political weight is the news. The repricing across JKM formation, strip and term contract leverage, and Korean power market transmission is what investors should model, with the caveat that how far each layer actually moves remains an open observation.

What This Article Does Not Claim

KOGAS-JERA cooperation is not a buyer cartel, and it does not directly control JKM. Joint procurement remains framed as “consideration” in the formal agreement text. The political cover gives the cooperation a higher institutional ceiling than before. Whether realization across spot, strip, and term segments actually occurs, and at what pace, is what the next several quarters will reveal. The direction — compressed JKM spikes, stronger buyer leverage in strip and term contracts, and downward pressure on Korean SMP and KEPCO fuel costs — is easier to underwrite than the magnitude. The magnitude depends on how quickly the framework converts political weight into recurring operational practice across each procurement layer. The investment question is therefore not whether KOGAS-JERA controls LNG prices. It is whether summit-backed buyer coordination becomes a recurring variable in Northeast Asian LNG procurement models.

If this analysis is useful for your team’s Asia LNG strategy, consider sharing it with colleagues evaluating Northeast Asian energy assets.