Three Doors Are Closing at Once: Korea's Heat Strategy and the End of the LNG-CHP Growth Model

Korea's first heat decarbonization strategy may freeze the very CHP investment it needs to replace.

DEEP DIVE | Image: Wirye CHP plant, surrounded by apartment complexes in Korea’s Wirye new town / Photo by the author

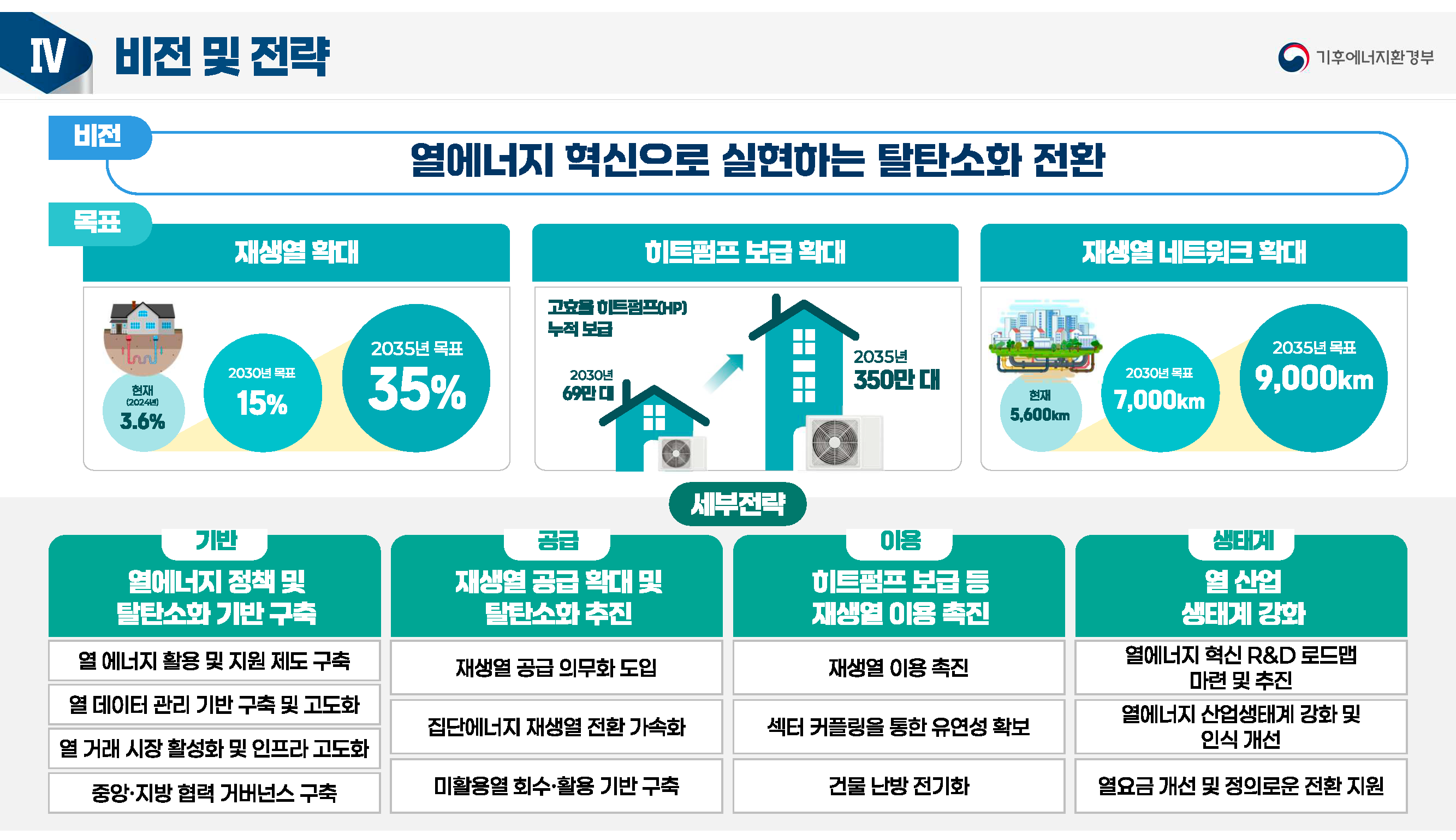

Korea’s Ministry of Climate, Energy and Environment (기후에너지환경부, MCEE) released a “Heat Energy Innovation Strategy” on April 15, targeting renewable heat at 35% of total heat supply by 2035. The current share is 3.6%. That is a nearly tenfold increase in nine years. The strategy also calls for 3.5 million heat pump installations and expanding district heating pipelines from 5,600 km to 9,000 km, backed by a planned Renewable Heat Obligation (RHO) for large-scale heat suppliers.

The headline numbers are ambitious. The commercially consequential details are elsewhere. Three forces embedded in the strategy converge on the same target: Korea’s LNG-fired combined heat and power (CHP) plants, the backbone of district energy. Together, they close the door on new projects, block the primary growth pathway for existing operators, and weaken the economics of new LNG CHP investment.

The asset class most exposed is not Korean district energy as a whole. It is the LNG-fired CHP plant built around predominantly residential new-town heat demand, with limited industrial offtake and few adjacent waste-heat sources. Industrial complex CHP, waste-heat-based operations, and KDHC’s diversified portfolio face a different set of economics.

A Global Direction, a Korean Design Choice

Korea is not alone in pushing heat decarbonization. The EU’s revised Energy Performance of Buildings Directive (EPBD) requires Member States to set out policies with a view to phasing out fossil-fuel boilers by 2040, while ending financial incentives for stand-alone fossil boilers from 2025. Germany has two linked reforms: the Wärmeplanungsgesetz requires municipal heat plans and rising renewable or unavoidable-waste-heat shares in heat networks, while the separate Gebäudeenergiegesetz contains a green-fuel ladder for certain gas and oil heating systems from 2029.

In the US, California targets 6 million heat pump installations by 2030, and New York’s All-Electric Buildings Act sets a 2026/2029 statutory phase-in for fossil-fuel equipment restrictions in new buildings, although implementation has been suspended pending federal appellate review.

Denmark offers the closest analogy to Korea’s district heating sector. Danish utilities have integrated power-to-heat (P2H) facilities into their CHP operations, using grid electricity to produce heat when wholesale power prices are low. Copenhagen’s system has largely shifted from coal-fired CHP to a mix of biomass, heat pumps, and waste incineration. Danish policy improved the economics of electric heat through electricity-tax and levy reforms, including the elpatronordningen, the reduction of the electrical heating tax, and the phase-out of PSO-related charges. These measures made large heat pumps and electric boilers financially viable for district heating operators.

The Korean strategy shares Denmark’s direction but not its mechanism. Where Denmark offered conversion economics first and mandates second, Korea’s strategy leads with permit conditions. The financial bridge for existing operators is described in the strategy document as a “renewable heat production cost differential subsidy” (재생열 생산 차액 지원). It remains at the “under review” stage with no published subsidy level, contract duration, or eligibility criteria (MCEE, Heat Energy Innovation Strategy, p.13).

The gap is not just in policy sequencing. It is in the physical infrastructure the policy must reshape. A typical new-town district energy CHP plant is a single 400 to 500 MW LNG-fired unit dedicated entirely to residential heating. It distributes medium-temperature hot water through underground pipelines to tens of thousands of apartment units across a new-town development. This configuration is globally unusual.

Even in Northern Europe, where district heating networks are most developed, CHP plants of this scale serve mixed loads that combine residential, commercial, and industrial demand. Where large CHP exists in Denmark or Finland, it is typically integrated with industrial off-takers who provide both heat demand diversity and, increasingly, waste heat for recovery. Korean new-town CHP serves a purely residential load. There is typically no large industrial anchor tenant, no nearby factory producing recoverable waste heat. Economically, these plants exist above all to serve apartment heat demand.

Denmark’s conversion was helped by a different starting point: district heating systems with more diverse heat sources, stronger municipal utility coordination, and policy instruments that improved the economics of electric heat before imposing a full conversion burden. Korean new-town CHP typically lacks many of these advantages.

The First Door: New Project Permits

Under the Heat Energy Innovation Strategy, three conditions would apply to new district energy permits. First, CHP turbines must be capable of hydrogen co-firing or full hydrogen combustion, and applicants must submit a hydrogen transition execution plan at the permit stage. Second, new CHP projects must incorporate renewable heat sources as baseload, with LNG capacity minimized. Third, since the 11th Basic Plan for Electricity Supply and Demand (제11차 전력수급기본계획), district energy CHP seeking to build or expand capacity must bid through the capacity market before receiving a permit.

Each condition has precedents in Korean policy. The hydrogen-ready turbine requirement extends a pattern I wrote about in March: Korea’s climate change impact assessment now requires LNG developers to present concrete hydrogen procurement plans as a permit condition. As I noted then, the barrier is three-layered, covering fuel supply, combustion technology, and delivery infrastructure. Korea has no dedicated hydrogen pipeline network. For inland CHP sites, there is no physical delivery pathway.

The renewable heat baseload mandate adds a geographic constraint. Because Korean new-town CHP is sited inside residential developments, surrounded by apartment complexes, it has few renewable heat sources within pipeline distance. Unlike industrial complex CHP, which can tap waste heat from co-located factories, new-town CHP has nothing to tap. Waste incineration facilities are usually located on city outskirts, requiring long-distance heat pipelines that the strategy envisions but has not yet funded. The strategy acknowledges this gap, noting that waste heat “is mainly generated on the outskirts of cities (incineration plants, etc.) and requires long-distance transport to demand centers (urban areas)” (MCEE, p.15).

Even where a renewable heat source does exist within reach, connecting it requires district heating pipelines that typically cost KRW 1 to 3 billion ($690,000 to $2.1 million) per kilometer depending on pipe diameter, road restoration, and urban constraints. Pipeline losses add another layer. Based on operator-level Korean district heating data I have reviewed over the past decade, summer network losses (as a share of heat sent into the network) in new-town systems before full occupancy can exceed 50%. Even after demand fills in, mature systems often show summer average losses of around 30%. This makes long-distance renewable or waste-heat connections difficult to underwrite unless the connected load is large, dense, and stable.

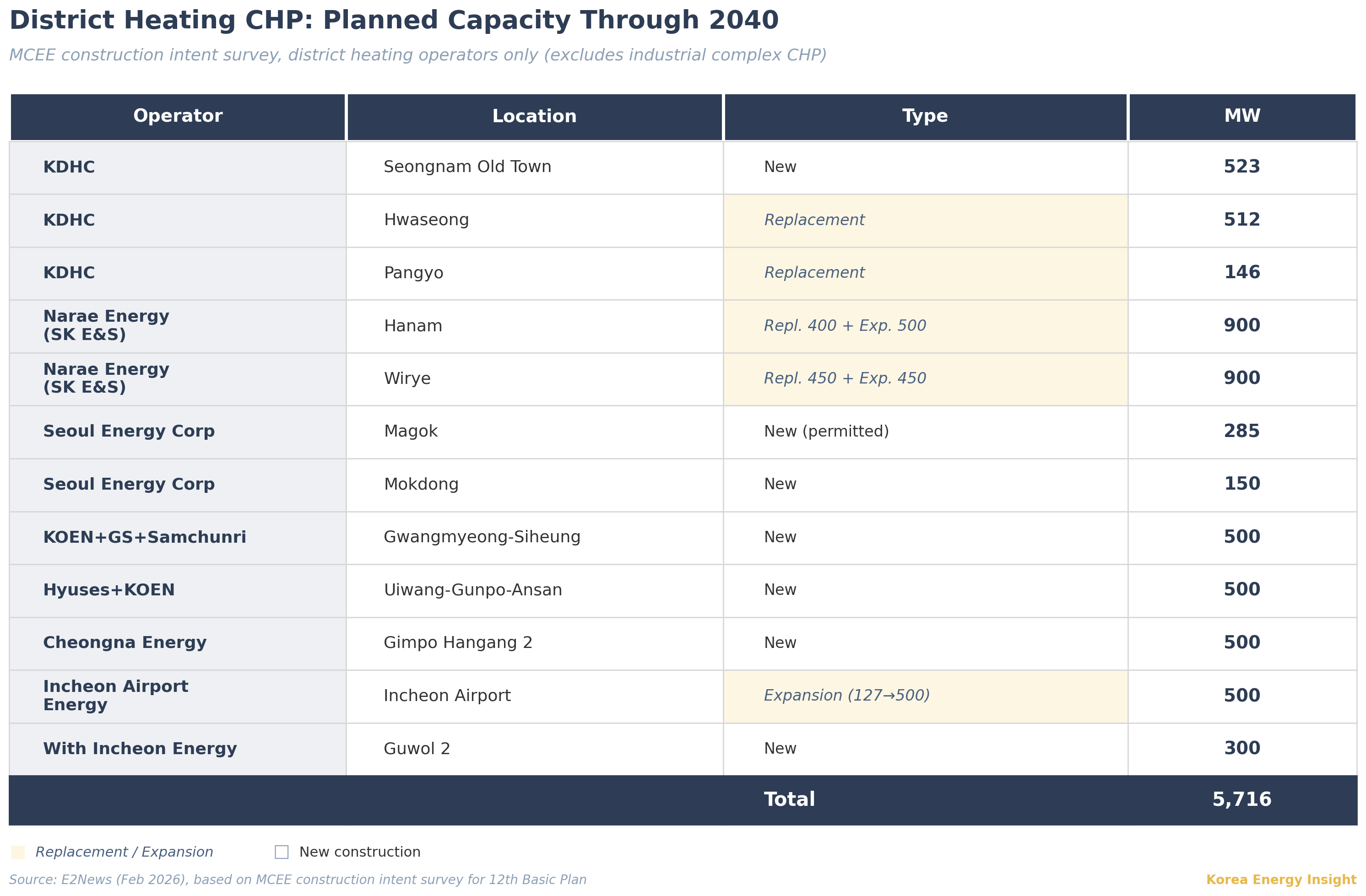

The capacity market bidding requirement adds a further cost. Winning the bid comes at a price. The 2024 pilot auction selected 0.9 GW of new district energy CHP. Industry participants estimate that successful bidders were awarded capacity payments more than 10% below the reference capacity price (RCP) that existing generators receive. Fixed-cost recovery shrinks before the first turbine is installed.

For a new-town district energy project to clear all three conditions simultaneously, it would need a proximate renewable heat source, a hydrogen-ready turbine design backed by a credible fuel procurement plan, and a successful capacity market bid. In practice, the number of sites where these requirements converge is very small.

The Second Door: The Growth Model That No Longer Works

New district energy permits have always been rare. A new supply zone only emerges when the government designates a large-scale new town, and that kind of development happens perhaps once a decade. The Ministry of Land is required under the District Energy Act to consult with MCEE during the planning stage, and MCEE has recognized district energy supply viability in most cases. Outside of these windows, the only alternative is to win contracts with redeveloped apartment complexes near existing heat sources, but that demand is limited.

So the realistic growth pathway for most existing operators has been to expand capacity when replacing aging CHP units. When an old unit reaches end of life, the operator replaces it with a larger, more efficient turbine, growing generation and heat supply within the same licensed zone. The driver is rising heat demand from apartment redevelopment projects inside and around the original new-town districts.

GS Power’s Anyang CHP modernization is the leading example: the company replaced its legacy units with two GE 7HA.02 gas turbines rated at roughly 500 MW each, raising total site capacity to approximately 960 MW.

More recently, Daejeon Cogeneration (대전열병합발전) received Korea Electricity Commission approval in February 2025 to replace its 113 MW LNG/LPG-fired steam turbine with a 495 MW LNG combined cycle unit. The company supplies both an industrial complex and public housing districts. The investment is $620 million (약 9,000억원; all USD conversions at approximately KRW 1,450/USD). The stated rationale was growing residential heat demand and the upgrade from an aging steam turbine to a modern combined cycle configuration. Other operators had been looking at similar replacement-driven expansion as their primary reinvestment pathway.

The Heat Energy Innovation Strategy would apply the same permit conditions to replacement projects. Under the strategy, any CHP replacement or expansion at an existing district energy site would need to meet the same renewable heat baseload, hydrogen-ready design, and capacity market bidding requirements. CHP plants built for Korea’s first-generation new towns in the early 1990s are already over 30 years old, and some have completed or begun modernization. Plants built for second-generation developments in the 2000s still have remaining design life. Replacement cycles will be spread across a long period rather than concentrated in a single window. The direction is clear: each replacement cycle now triggers conditions that most existing sites cannot satisfy.

For operators who viewed replacement as their primary reinvestment opportunity, the strategy puts the only scalable growth pathway under regulatory and economic stress. New-town district energy is no longer a sector where operators can grow into a transition. The remaining options are to maintain aging assets as long as regulators permit, or to invest in renewable heat conversion on terms the government has not yet defined.

The Third Door: The Heat Cost Math

Korean CHP economics hinge on one thing: getting dispatched. When a CHP plant receives dispatch in the wholesale electricity market, it earns power revenue at SMP and produces heat as a co-product at low marginal cost. The internal cost accounting most operators use is what the CHP engineering literature calls the power loss method. It measures the cost of heat by the electricity output sacrificed when the turbine shifts from full condensing mode to heat extraction mode. As long as the plant is dispatched and selling electricity profitably, this foregone revenue is manageable and heat remains cheap to produce.

The problem arrives when the plant is no longer economically dispatched but still has to run for heat. District heating customers need heat regardless of whether the wholesale market wants the plant’s electricity. When a CHP operates in heat-constrained mode, it generates power that it sells at a loss because its variable cost exceeds SMP. Under internal cost accounting, that electricity-side loss flows directly into heat production cost. Heat cost does not rise gradually. It spikes.

Korea’s annual average SMP fell from 167 won/kWh in 2023 to about 113 won/kWh in 2025. The decline likely reflects a combination of fuel-price normalization after the 2022-23 shock, demand conditions, dispatch mix, and the growing role of low-marginal-cost resources. For CHP, this is not a mechanical loss trigger. A dispatched CHP unit that is not the marginal generator still earns a positive power margin, and thermal storage allows heat production to be shifted across hours.

The problem is subtler. Lower SMP compresses the power-side upside that historically helped justify LNG CHP investment, just as renewable-heat capex, RHO compliance costs, and tariff constraints are rising. SMP decline alone does not break the model. It removes part of the cushion that made the model bankable.

Korean CHP projects have often been underwritten at integrated IRRs in the 8.5 to 9% range. This level clears both internal investment committee approval and project finance bankability thresholds, but with little room to spare. When that cushion thins from both the revenue side and the cost side simultaneously, fewer projects clear the threshold.

The tariff regime compounds the problem. District heating tariffs in Korea are not set by individual operators. Korea District Heating Corporation (한국지역난방공사, KDHC), the market-dominant operator, sets the reference tariff, subject to MCEE approval. Private district energy operators follow this benchmark. But KDHC’s heat production cost reflects a blended mix that includes low-cost waste heat from incineration facilities and other sources, not just CHP. Private operators who rely primarily on LNG CHP are benchmarked against a tariff shaped by a cost base they do not share.

This gap will widen under the RHO. KDHC already uses substantial volumes of waste heat, which likely puts it close to or within early RHO compliance thresholds without significant new investment. If KDHC can meet its obligation from existing operations, RHO compliance costs may not be reflected in the reference tariff. Private operators who must spend to comply will be recovering those costs against a benchmark that does not include them.

An operator running losses on heat cannot independently raise its tariff to recover costs. Industrial complex CHP operators negotiate heat prices directly with their industrial off-takers and have full pricing autonomy. The difference is not marginal. It is the gap between a business that can pass through transition costs and one that cannot.

Heat costs are already rising for structural reasons. If the Heat Energy Innovation Strategy is implemented as written, two additional cost layers land on top. The first is capital expenditure for renewable heat equipment and hydrogen-ready turbine designs. The second is ongoing RHO compliance costs, whether through self-production or certificate purchases. Both require real spending. Neither has a clear pass-through mechanism under the current tariff regime. The strategy adds costs to a business that has already lost the ability to cover the costs it has.

What This Means

The three doors point in the same direction. New permit conditions raise capital requirements: renewable heat baseload equipment, hydrogen co-firing or full combustion capable turbines, and the engineering to integrate both into a single plant. The revenue side is compressing. SMP decline thins the power-side cushion, heat-constrained operation raises heat costs, and the tariff regime locks operators into a benchmark set by a public corporation with a lower cost base. The strategy raises the cost of building. It shrinks the returns that justify building.

The immediate consequence is that new district energy investment in new-town settings is frozen until the subsidy terms are defined. Between the permit conditions and the margin compression, few projects are likely to clear the historical underwriting threshold without defined subsidy terms. Replacement-driven expansion, the only scalable growth model operators had, faces the same conditions. Operators who were planning modernization projects now have to re-run their numbers against requirements that did not exist when those projects were conceived.

The second consequence is that “Korean district energy” is no longer a single asset class. Renewable heat access and tariff autonomy now both favor industrial complex CHP over new-town district heating CHP. Each of these differences was discussed above. What matters in the implications is that they are moving in the same direction at the same time. The two segments are diverging into separate asset classes with different risk profiles and different return structures.

The third consequence reaches beyond existing district energy operators. New LNG combined cycle permits are effectively blocked for standalone power projects. KEPCO’s generation subsidiaries (GENCOs) and other developers have been looking at district energy CHP as an alternative pathway to replace retiring coal capacity. The Heat Energy Innovation Strategy forces these prospective entrants to reassess the economics. The same permit conditions, RHO compliance costs, and tariff constraints that squeeze existing operators apply to anyone entering the sector. For GENCOs evaluating coal-to-CHP conversion as a growth avenue, the profitability assumptions behind those plans need to be re-examined.

What to Watch

RHO initial obligation ratio and timeline. The strategy does not specify a starting percentage. If the ratio starts below 10%, operators have time to source renewable heat or purchase certificates. At 20% or above, combined with the permit conditions and the tariff gap, the cost burden exceeds what most private operators can absorb from day one.

Whether KDHC’s existing waste heat counts toward RHO compliance. If it does, KDHC meets its obligation without new spending, and the reference tariff stays flat. Private operators then carry RHO compliance costs that the benchmark was never designed to recover. The eligibility rules for what qualifies as “renewable heat” under the RHO will determine how unevenly the burden falls.

Cost differential subsidy structure. A 15-year fixed-price availability contract, similar to the ESS central contract market model, could anchor long-term conversion investment. Annual CAPEX grants would accelerate hardware deployment but leave operating cost exposure unresolved. The structure matters more than the headline amount. But there is almost no precedent for direct financial policy support reaching district heating operators in Korea. Outside of GS Power’s PPA arrangement and the full free K-ETS allocation that district heating heat received in earlier phases, government subsidies have rarely flowed to this sector. Whether the promised cost differential subsidy materializes, and in what form, is an open question.

GENCO coal-to-CHP project pipeline decisions. Several KEPCO generation subsidiaries have been pursuing district energy CHP as a coal replacement pathway. Whether they proceed, scale back, or restructure those plans after the strategy’s permit conditions and RHO terms become clear will signal how the broader market reads the economics.

Capacity market auction terms for replacement projects. The 2024 pilot auction applied a 10%+ RCP discount to new CHP entrants. Whether the same discount structure applies to replacement and expansion projects will determine whether modernization remains financially viable at existing sites.

If MCEE publishes the RHO ratio and subsidy terms before the end of 2026, expect the first wave of operator responses by mid-2027. If those details remain undefined into 2027, the more likely outcome is that replacement investment freezes and aging CHP assets run longer than they should.

I will track the RHO design, subsidy structure, and CHP auction terms as they move from strategy to implementation.