From Grid Cost to Asset Class: Korea's Stability Bill Is About to Become Investable

Korea's grid bottleneck is hiding the real cost of renewables. Relieving it will make the bill visible.

MARKET SIGNAL

On March 26 and 27, 2026, Korea’s System Marginal Price (SMP) hit 0 won/kWh at 1 PM. Wholesale electricity was free. Every synchronous generator running at that hour was losing money on energy alone. But Korea Power Exchange (KPX) could not let them shut down — without their spinning mass, the grid loses the inertia and frequency response that prevent blackouts.

This is the tension at the center of Korea’s power market. The generators that keep the lights on are the same ones being priced out of the energy market. And because Korea is an island grid with zero interconnection, there is no neighbor to borrow stability from. Every megawatt of inertia, every second of frequency response, every megawatt of black-start capacity must be sourced domestically.

The Problem You Can’t See Yet

Korea’s Jeolla region hosts roughly 10 GW of operating renewable capacity, with permits for another 32 GW in the pipeline — a potential total exceeding 40 GW (MOTIE). But most of this output is bottled up behind transmission constraints. The 345 kV lines connecting Jeolla to the Seoul metropolitan load center are saturated. When output exceeds the northbound transfer limit, KPX curtails, and the variability stays trapped inside the regional grid.

The bottleneck is currently doing free work. Because Jeolla’s variability cannot reach the national grid, the system operator does not have to manage it nationally. And because the region has relatively few large industrial loads, the curtailment barely registers in the energy debate.

The Ministry of Climate, Energy and Environment (MCEE), which assumed energy policy jurisdiction from MOTIE in October 2025, is pushing to fix this. The plan includes five 345 kV routes, two subsea HVDC corridors along the west coast, and 36 reinforcements at 154 kV. When those lines open, the renewable variability hidden behind regional constraints will flow into the national grid. The stability bill that was invisible will become visible.

The Invisible Bill

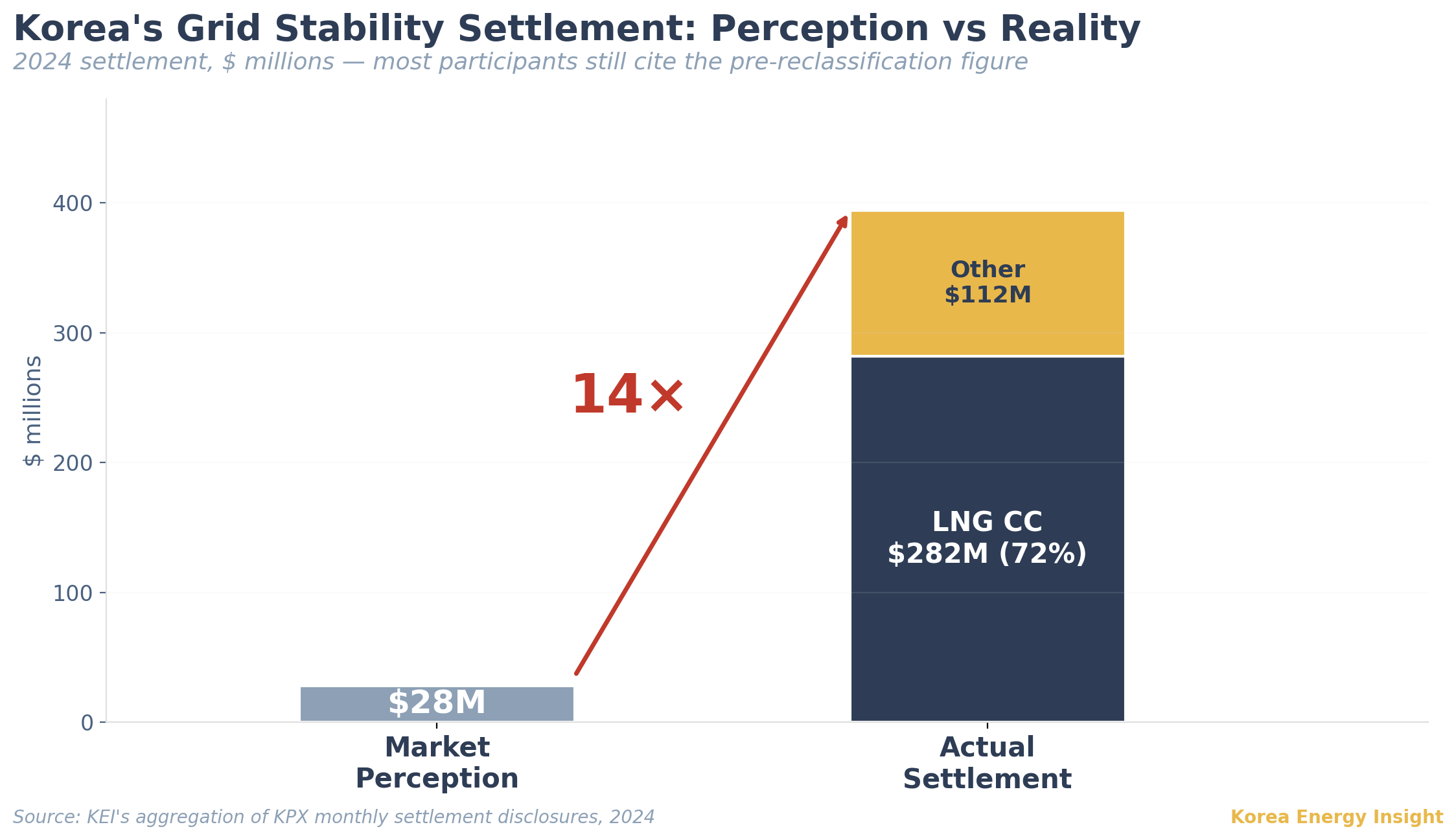

Korea’s ancillary services market settled $394 million (KRW 571.6 billion) in 2024, based on KEI’s aggregation of KPX settlement disclosures. LNG combined-cycle plants captured $282 million of that, 72%. Most market participants still cite the outdated $28 million figure from before the reserve capacity value settlement was reclassified. The real number is 14 times larger — and the bottleneck is still in place.

That $394 million is the current price of grid stability. The 11th Basic Plan for Electricity Supply and Demand targets 77.2 GW of solar and 40.7 GW of wind by 2038. As inverter-based resources displace synchronous machines, the services those machines provided as a byproduct must be procured and paid for separately. Spain’s April 2025 blackout, where 31 GW was lost in three minutes, is still under investigation. But the preliminary finding, loss of voltage control in a high-inverter system (ENTSO-E), reinforces a basic point: as synchronous machines exit, the services they provided do not exit with them. Someone has to pay.

Why the Best Grid Assets Lose Money

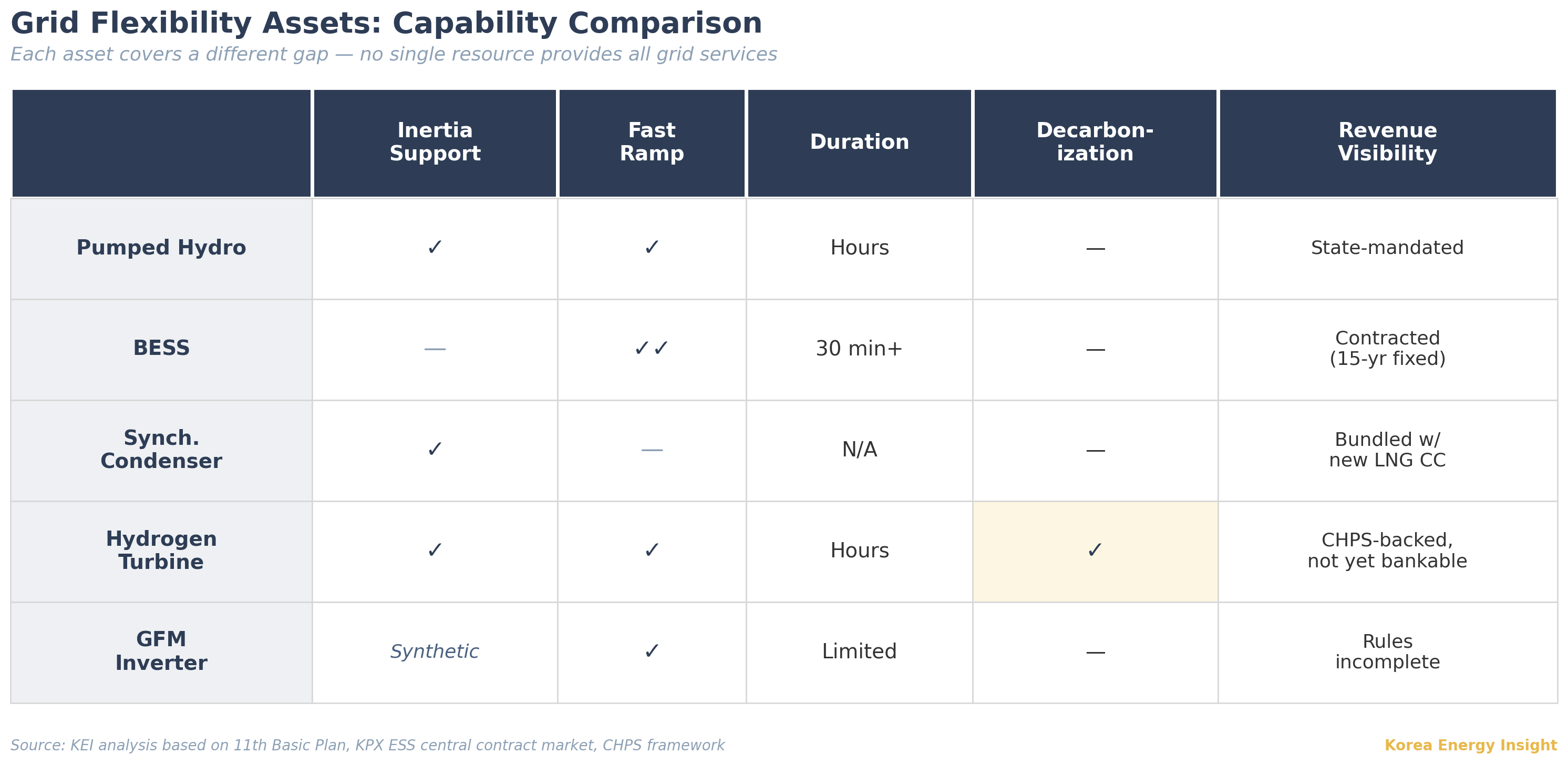

Battery storage and pumped hydro respond faster than any other grid resource available in Korea. BESS responds in under 200 milliseconds. Pumped hydro reaches full power from standstill in under two minutes and can hold it for hours. Both are essential for absorbing variability.

Neither makes money on its own.

KEPCO invested roughly $410 million (KRW 600 billion) in 376 MW of frequency regulation ESS (FR-ESS) between 2014 and 2017. The program was suspended after the cost-benefit ratio fell to 1.09, compounded by serial battery fires (E2News, 2020). In a 2016 dual-generator trip, the FR-ESS exhausted its stored energy within 10 minutes and contributed nothing to the second fault (E2News, 2017).

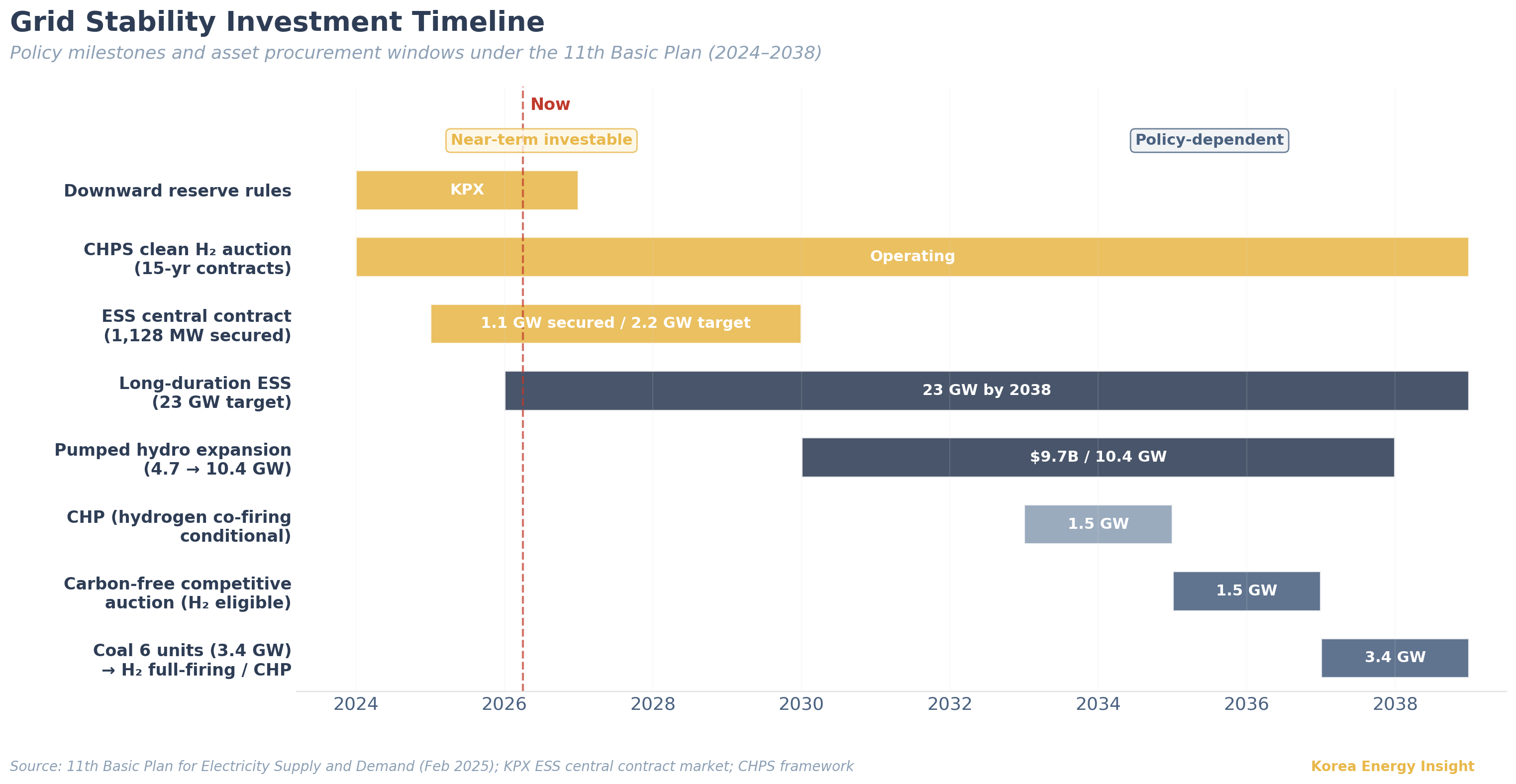

Pumped hydro operates at a structural loss, sustained only because Korea Hydro & Nuclear Power (KHNP), a state-owned enterprise, absorbs the deficit. The 11th Basic Plan calls for expanding pumped hydro from 4.7 GW to 10.4 GW at $9.7 billion (KRW 14 trillion; all USD conversions at approximately KRW 1,450/USD), plus 23 GW of long-duration ESS by 2038. At current market prices, none of these are commercial investments. They are public infrastructure mandates.

That is why they become investable.

From Public Mandate to Private Opportunity

KPX’s ESS central contract market proved the template: 15-year fixed-price availability contracts where government bears market risk and private capital provides the asset. Two mainland auctions have secured a combined 1,128 MW: 563 MW in the first round, 565 MW in the second (KEI, “The Storage Pivot,” March 2026). KKR and BlackRock have entered through special purpose company structures. A third auction is expected within 2026.

Korea has seen this pattern before. After the 2011 blackout left 1.6 million households without power, MOTIE relaxed the licensing review for LNG combined-cycle and CHP projects that had previously faced tight scrutiny. Private IPPs and KEPCO subsidiaries added roughly 18 GW of gas-fired capacity over the following years (EPSIS). Crisis produces policy; policy produces the investment cycle.

The near-term investable assets are those with revenue structures already in place: BESS under central contract, pumped hydro under public mandate, and synchronous condensers bundled with new LNG CC under the 11th Basic Plan. Further out, hydrogen-capable gas turbines and grid-forming (GFM) inverters depend on procurement rules still being written, but the policy direction is set. The 11th Basic Plan reserves 1.5 GW for carbon-free competitive auction in 2035–2036, where hydrogen is eligible. The Clean Hydrogen Portfolio Standard (CHPS), launched in 2024 as the world’s first clean hydrogen power auction, already provides 15-year purchase contracts for hydrogen-fired generation. And from 2037, up to 3.4 GW of retiring coal capacity is designated for conversion to hydrogen full-firing or CHP, at the operator’s discretion. The Basic Plan labels this capacity “hydrogen/ammonia,” but Korea is phasing out coal, not retrofitting it. Ammonia co-firing is a transitional measure for plants that remain. The long-term destination is hydrogen turbines replacing coal units outright.

Each of these assets covers a different gap. Pumped hydro provides both inertia and fast ramping, but cannot decarbonize its fuel source. BESS responds fastest but offers no synchronous inertia and is constrained by duration. A hydrogen-fired gas turbine is the only resource that combines synchronous inertia with a fuel pathway to net zero.

Base case

The 11th Basic Plan mandates synchronous condenser capability for new LNG CC and targets 10.4 GW of pumped hydro plus 23 GW of long-duration ESS by 2038. It also signals three reform directions: source-specific capacity procurement starting with a carbon-free capacity market, locational pricing to eventually replace the single national SMP, and a separate ancillary services market. KPX introduced downward reserve rules in 2024. The Jeju pilot market cut renewable curtailment by 94% by separating real-time energy and reserve settlement, and MCEE is preparing mainland extension. A year ago, most of these were proposals, not operational programs. The question is no longer whether intervention comes, but how fast procurement scales.

What I’m watching

The timeline gap between transmission and flexibility. If the Jeolla-Seoul corridors open before ESS and pumped hydro catch up, the stability bill spikes in the transition window. The third ESS central contract auction and the Jeju pilot’s pricing transparency will signal whether procurement is keeping pace.

What would change my mind

The East Asia Super Grid has appeared in multiple Korean government energy roadmaps. Japan is the most plausible interconnection partner. Korea’s 60 Hz is directly compatible with western Japan, and two early-stage HVDC projects exist: Busan-Kyushu (2 GW) and Pohang-Chugoku (2 GW). But Japan’s grid is split by a frequency wall. The converter capacity between its 50 Hz east and 60 Hz west is roughly 3 GW against a 290 GW system (OCCTO). Japan’s renewable surplus sits in the 50 Hz zone Korea cannot directly access: Hokkaido alone has 28.9 GW of renewable capacity against 7.9 GW of local demand (OCCTO). Interconnection links Korea to the half that needs power, not the half with too much. Until Japan resolves its own internal bottleneck, the domestic flexibility buildout remains the primary path.

If this analysis is useful for your team’s Asia energy strategy, consider forwarding it to a colleague.