Korea's Fusion Pivot After the EAST/WEST Records: What the 5th Basic Plan Means for Supply-Chain Exposure

Korea's first investable fusion layer is forming in EPC and qualified manufacturing — years before power sales begin.

DEEP DIVE | Image: KSTAR via Korea Institute of Fusion Energy (KFE)

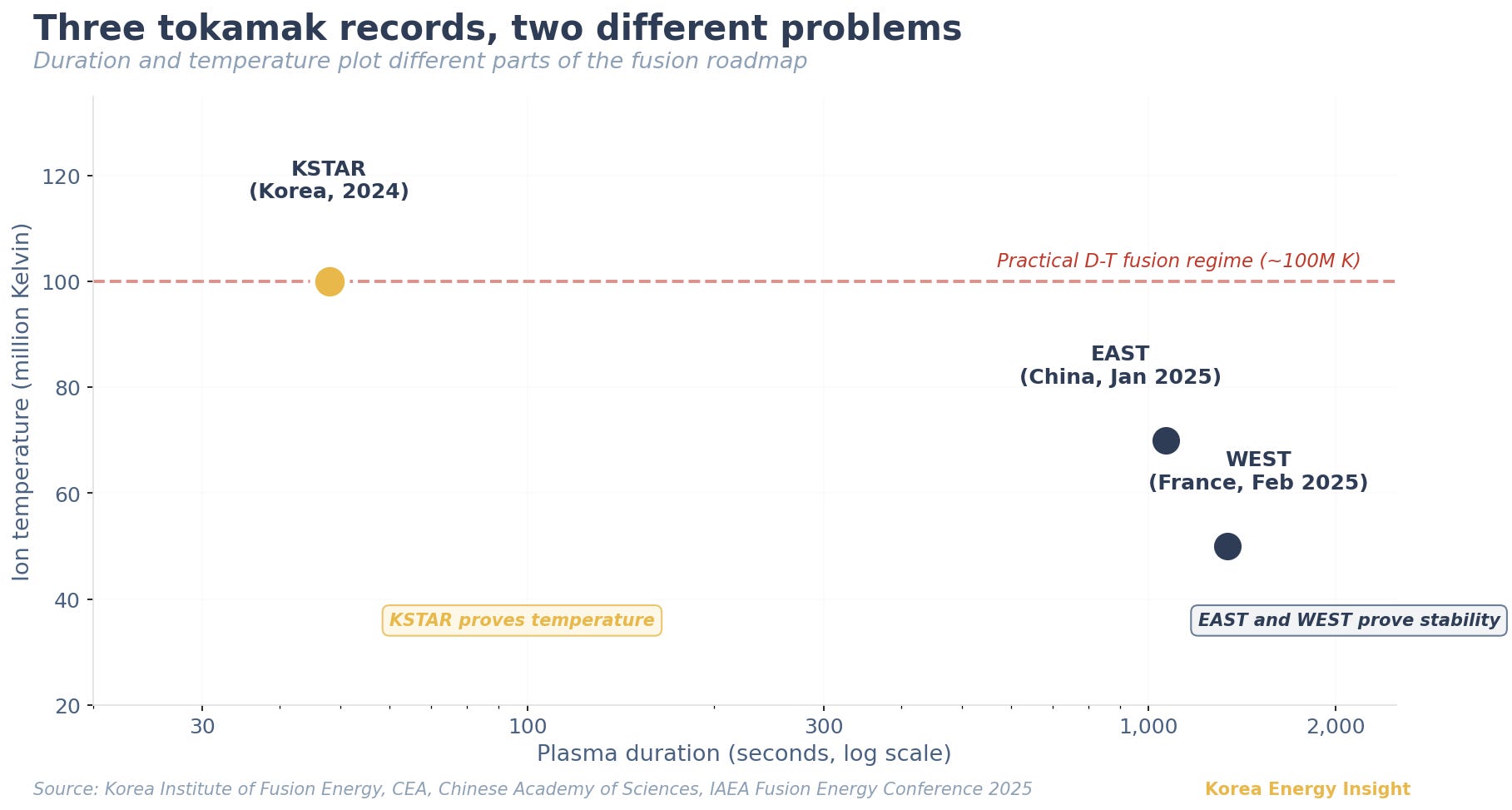

On January 20, 2025, China’s EAST tokamak held a steady-state H-mode plasma for 1,066 seconds. Twenty-three days later, France’s WEST reactor reached 1,337 seconds with an ITER-grade tungsten divertor (CEA; IAEA Fusion Energy Conference 2025). Korea’s KSTAR holds a different record: sustaining ion temperatures above 100 million Kelvin for 48 seconds, a hot-ion performance milestone rather than a duration milestone (Korea Institute of Fusion Energy). The three results sit on the same tokamak roadmap, but they do not measure the same thing. Headlines compared the seconds. The physics did not.

Fusion is, in theory, as close to infinite energy as physics permits. Commercialization is still far off, but concrete movement has begun. And if it ever reaches commercial scale, electricity at near-minimum production cost would flow at almost unlimited volume — in theory, the electricity market itself loses its reason to exist. That is one of the spaces I follow with personal interest.

By May 2026, Korea was planning fusion in a different benchmark environment. The Ministry of Science and ICT (MSIT) launched the planning committee for the 5th Basic Plan for Fusion Energy Development (2027-2031), framing Korea’s target as a 2030s fusion electricity demonstration rather than the previous 2050s technology ambition. Read against EAST and WEST, the plan looks less like a sudden leap forward and more like a repositioning under pressure.

Fusion power is not yet bankable in Korea, but parts of the fusion supply chain may already be dealable. The 5th Basic Plan does not change that fact, but it does indicate which industrial assets are forming first, before electrons reach the grid. The more revealing detail is who leads the industrial alliance. Samsung C&T, the construction and engineering arm of the Samsung group, chairs the Fusion Innovation Alliance — Korea’s 91-member industry-academia-research grouping for fusion.

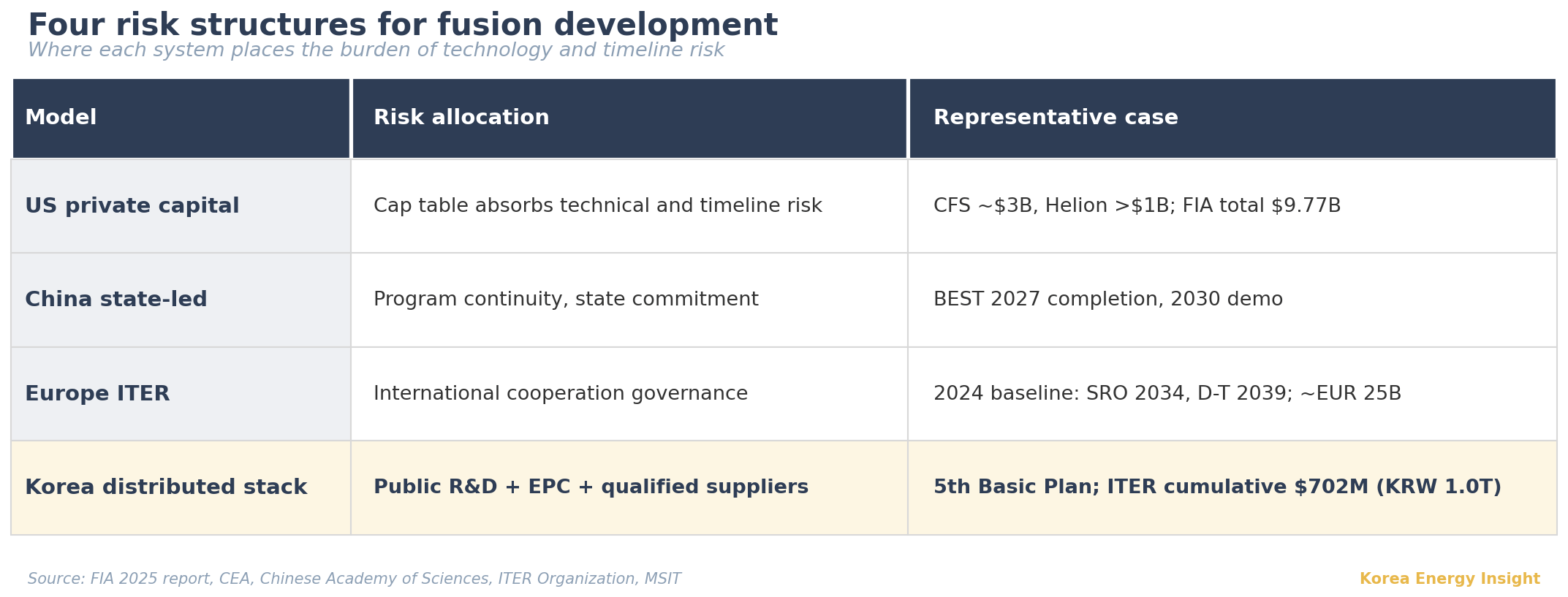

Three models, three risk structures

The US private-capital model has reached scale. The Fusion Industry Association (FIA) counted $9.77 billion in cumulative private investment across 53 firms in its 2025 report. Commonwealth Fusion Systems (CFS) alone has raised approximately $3 billion, including an $863 million Series B2 round in August 2025. Helion Energy has crossed $1 billion in cumulative funding and maintains a 2028 power-supply target to Microsoft. The model places technology milestones and corporate valuation inside the same cap table. Technical risk is absorbed there and translated directly into headcount and timeline risk: 83% of FIA respondents reported follow-on funding difficulty, and General Fusion cut staff by approximately 25% in May 2025 before its January 2026 SPAC merger.

China’s state-led model absorbs risk through programmatic continuity. The Burning Plasma Experimental Superconducting Tokamak (BEST) installed its cryostat base in October 2025, targets 2027 completion, and aims for net energy gain at 20 to 200 MW fusion power with a 2030 electricity demonstration (Chinese Academy of Sciences). Corporate valuations do not enter the calculation. State commitment does.

Europe’s model is built around ITER and absorbs risk through international cooperation governance. The 2024 baseline pushed start of research operation to 2034 and deuterium-tritium operation to 2039 (ITER Organization), with construction cost estimates rising to approximately €25 billion. Schedule slippage in this model reflects governance design rather than execution failure.

Korea is building a fourth structure. Risk is distributed across public R&D budgets, EPC firms, regional government infrastructure investment, and ITER-qualified manufacturing exposure. That distribution determines which kind of investor sees which kind of opportunity.

Korea’s real pivot: from plasma records to buildable infrastructure

KSTAR’s record is often misread in direct comparison. Fusion power requires three conditions met simultaneously: temperature high enough for atomic nuclei to fuse, fuel density high enough for frequent collisions, and stability long enough for the reaction to be useful as a power source. For the deuterium-tritium reaction targeted by most mainstream fusion power concepts, the temperature threshold is approximately 100 million Kelvin. Below that, fusion reactions occur too rarely to produce net energy. Without long plasma stability, a reactor cannot operate as a power plant.

EAST and WEST proved stability. The 1,066-second and 1,337-second records, over 17 and 22 minutes of steady plasma, demonstrated that this tokamak type can hold plasma long enough for a working power plant cycle. The value lies in what had to work for the plasma to remain stable that long: confinement mode control, tungsten first-wall durability (the same material ITER uses), heat exhaust management, and continuous operation of magnetic and heating systems. Several systems that matter for a future power plant were tested under long-duration conditions. But they operated at approximately 70 million and 50 million Kelvin, below the temperature regime needed for practical D-T fusion power. KSTAR proved temperature. Its 48-second record sustained ion temperatures above 100 million Kelvin, the regime generally associated with practical D-T fusion power, but only briefly because the surrounding systems cannot yet hold that environment for long. The two record categories measure different parts of the same problem, and no machine has held both simultaneously.

The “world’s longest” headline has moved to EAST and WEST. But what KSTAR achieved — fusion-grade temperatures — neither EAST nor WEST has matched.

A 56-member committee operates across three working groups within the 5th Basic Plan: demonstration acceleration, ecosystem innovation, and infrastructure advancement (MSIT, May 7, 2026). “KSTAR 2.0” upgrades the existing device. The Korean Innovative Fusion Reactor, a compact demonstration reactor, enters conceptual design in 2026 with a 2.1 billion won ($1.4 million) initial budget. An AI virtual fusion reactor program receives 4.5 billion won ($3.1 million) for 2026. Eight core technologies define the roadmap, four for miniaturization and four for power generation. Fusion-specific regulation will be developed separately from the existing atomic energy framework.

The Fusion Innovation Alliance, 91 industry-academia-research institutions chaired by a Samsung C&T vice president, anchors the industrial layer (MSIT, December 2024). That chairmanship matters because Samsung C&T is built around construction and project execution. The firm builds power plants, refineries, and large infrastructure across Samsung group’s industrial portfolio. The choice signals what Korea wants the 5th Basic Plan to mean industrially: a commitment to physically build demonstration and commercial reactors, and to export that EPC capability to global fusion projects as they reach the construction phase.

Korea’s 2026 fusion R&D budget, at 112.4 billion won ($78 million; all USD conversions at approximately KRW 1,450/USD), is not large by private-market standards. CFS’s August 2025 Series B2 alone was roughly eleven times that amount in won terms. But the comparison misses the structure. Capital is distributed across a 1.5 trillion won (~$1.0 billion) technology and infrastructure program, a 1.2 trillion won ($828 million) Naju “artificial sun” research facility planned for 2027 to 2036, ITER-qualified suppliers, and an EPC-led industrial alliance.

The supply-chain layer is already measurable. Korea’s cumulative ITER procurement reached 223 contracts worth 1.0173 trillion won ($702 million) by February 2026, held by Hyundai Heavy Industries (vacuum vessel sectors, often called “ITER’s heart”), Doosan Enerbility, Korea Hydro & Nuclear Power, and mid-sized specialists (MSIT, February 2026). These contracts are already producing revenue. KENTECH’s superconducting conductor test facility at Naju is now under construction.

Dealable now, bankable later

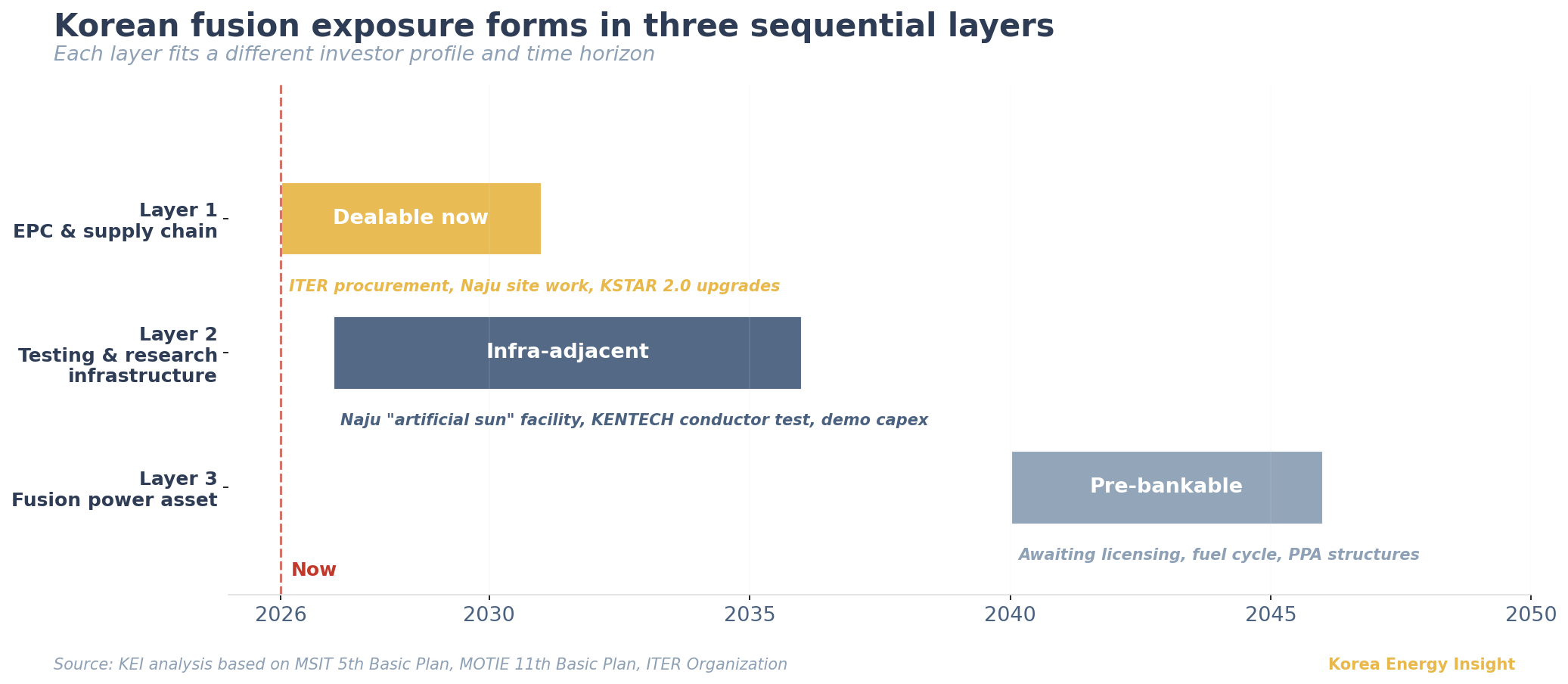

The 5th Basic Plan does not try to produce a Korean equivalent of CFS. Korea’s route runs through a distributed industrial stack — public R&D, EPC, and qualified suppliers — rather than a single venture-backed reactor company. Korean fusion exposure is forming in three sequential layers, each suited to a different investor type.

The first layer, active now through approximately 2031, is the equipment and EPC supply chain: ITER procurement, Naju site work, KSTAR 2.0 upgrades, and qualified Korean industrials in vacuum, superconducting, power-conversion, and remote-handling segments. This layer is dealable. The opportunities lie in the supply chain itself: growth-equity stakes in fusion-capable units, carve-outs from diversified industrials, roll-ups of fragmented mid-sized suppliers, and equity participation in firms with export optionality to global fusion construction projects. For private equity, the cleaner thesis is not betting on which reactor design wins globally. It is backing the qualified suppliers every reactor design will need.

The second layer, forming from 2027 to roughly 2036, is specialized testing and research infrastructure: the Naju facility, KENTECH’s conductor test setup, and demonstration-supporting capex. This is infra-adjacent rather than core infrastructure, since concession structures, operating rights, and availability payments are not yet defined. In practice, it may create project, equipment, and financing opportunities, but not yet the kind of contracted cash-flow asset that infrastructure funds typically underwrite. For infrastructure funds, Korea’s fusion story sits on an infra-adjacent watchlist: public research facilities, specialized manufacturing capex, and the regulatory architecture that would have to exist before fusion power can become project-financeable.

The third layer, the fusion power asset itself, sits beyond 2040 and remains pre-bankable until licensing frameworks, fuel cycle systems, and PPA structures exist. Consistent with this timeline, the current 11th Basic Plan for Electricity Supply and Demand, finalized in February 2025 and running through 2038, does not include fusion in its 2038 power mix. That reflects the plan revision cycle rather than government intent; fusion will likely be incorporated in the 12th or 13th iteration as the project becomes visible. For asset sequencing, the development cycle matters more than the plan cycle.

The government-led nature of Korea’s fusion strategy still leaves room for private capital. Private capital should look away from reactor equity, toward procurement-linked suppliers, EPC capability, and capex-heavy testing infrastructure. Korea’s chosen asset form is a public-private industrial stack that monetizes earliest through equipment and EPC. It differs from both the US venture-backed approach and a single state champion model.

The corporate-structure risk is real. Dawonsys, the ITER power-supply unit subcontractor that won an additional 82 billion won ($57 million) ITER order in June 2025, entered court-supervised rehabilitation in April 2026 over losses in its rolling-stock business unrelated to fusion (Seoul Transportation Corporation; Suwon Bankruptcy Court). The fusion-capable engineering and the failed business sat inside the same corporate wrapper. Fusion exposure through Korean industrials cannot be screened by order wins alone. The relevant question is whether the fusion-capable unit can be isolated from unrelated balance-sheet risk, through carve-out, JV structure, ring-fenced project finance, or direct minority investment at the subsidiary level. Investors underwrite both the fusion capability and the wider company balance sheet that contains it.

What to watch

The Naju “artificial sun” research facility preliminary feasibility result, expected around August 2026, is the first concrete trigger. A pass confirms the 1.2 trillion won infrastructure commitment and opens equipment, EPC, and specialized manufacturing procurement pools through 2036. A delay or rejection shifts the entire demonstration timetable and pushes back the supply-chain anchor for Honam-region energy industrial development. The Naju decision is also the first concrete test of whether the Innovation Alliance’s chair seat at an EPC firm translates into actual construction commitments.

The Fusion Energy Development Promotion Act amendment, particularly the “industry support enhancement” provisions, will signal whether Korea moves toward a separate fusion regulator outside the Nuclear Safety and Security Commission. Comparable separation in the United States (NRC’s 2023 byproduct material decision) and the United Kingdom (Energy Act 2023) created regulatory pathways for private fusion plants. Korea’s choice on the same question shapes when the third layer becomes investable.

The KSTAR 2.0 strategy, listed as a separate document in the 5th Basic Plan and not yet released, will determine which Korean suppliers gain qualification advantages. Specific upgrades to superconducting magnets, divertor systems, heating and current drive, or vacuum components will translate directly into deal flow for the firms holding those competencies.

The K-Moonshot project director appointment in 2026 will determine how the fusion track converts political ambition into technical milestones, and whether the Fusion Innovation Alliance transitions from a consultative body to a project-execution vehicle with formal procurement, JV, or consortium structures. The shift from MoU to actual contracts and project execution is the trigger that activates the supply-chain layer for private capital at scale.

The next ITER cumulative order update, likely late 2026 or early 2027, will be the most direct valuation signal for Korean industrial firms with fusion exposure. The 2026 new order pace started at 21.1 billion won ($14.6 million). Whether that grows or compresses reflects how the global ITER schedule and Korea’s manufacturing competitiveness intersect.

For now, the Korean fusion story is not about when fusion electrons reach the grid. It is about which Korean firms become qualified to build the machines, facilities, and regulated infrastructure that must exist before those electrons can be sold. The first dealable layer is forming now, in EPC, equipment, and qualified manufacturing — well before fusion becomes a bankable power asset.

If this analysis is useful to your team’s view on Korean fusion strategy and supply-chain exposure, consider forwarding to colleagues working on Asia infrastructure or energy industrial policy.