The Fuel Cell Revaluation: Korea's Fuel Cells Are Utility-Scale, The Policy Isn't

Korea builds them at utility scale. The policy framework still calls them distributed.

MARKET SIGNAL | Image: Bloom Energy SOFC / Bloom Energy

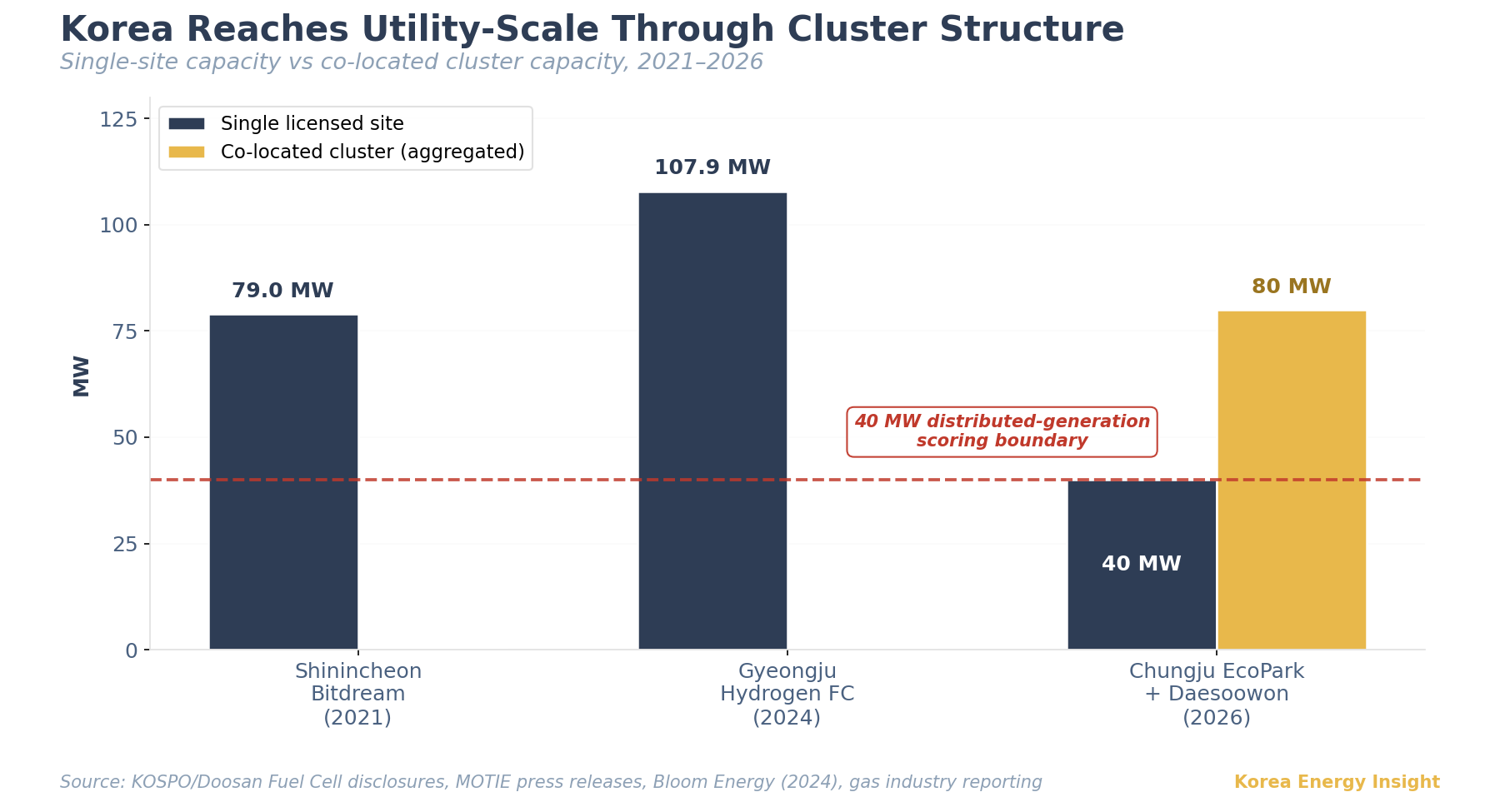

SK Eternix commercialized the 40 MW Daesoowon SOFC plant in Chungju this week. Together with the adjacent 40 MW Chungju EcoPark, the site forms an 80 MW cluster that Bloom Energy described in 2024 as the largest single-site fuel cell installation in the company’s history.

That framing deserves attention beyond a corporate milestone. Korea’s fuel cell fleet has been reaching utility scale for years, while the regulatory framework keeps treating it as distributed energy. The new cluster makes that contradiction harder to ignore.

Korea’s quiet leadership

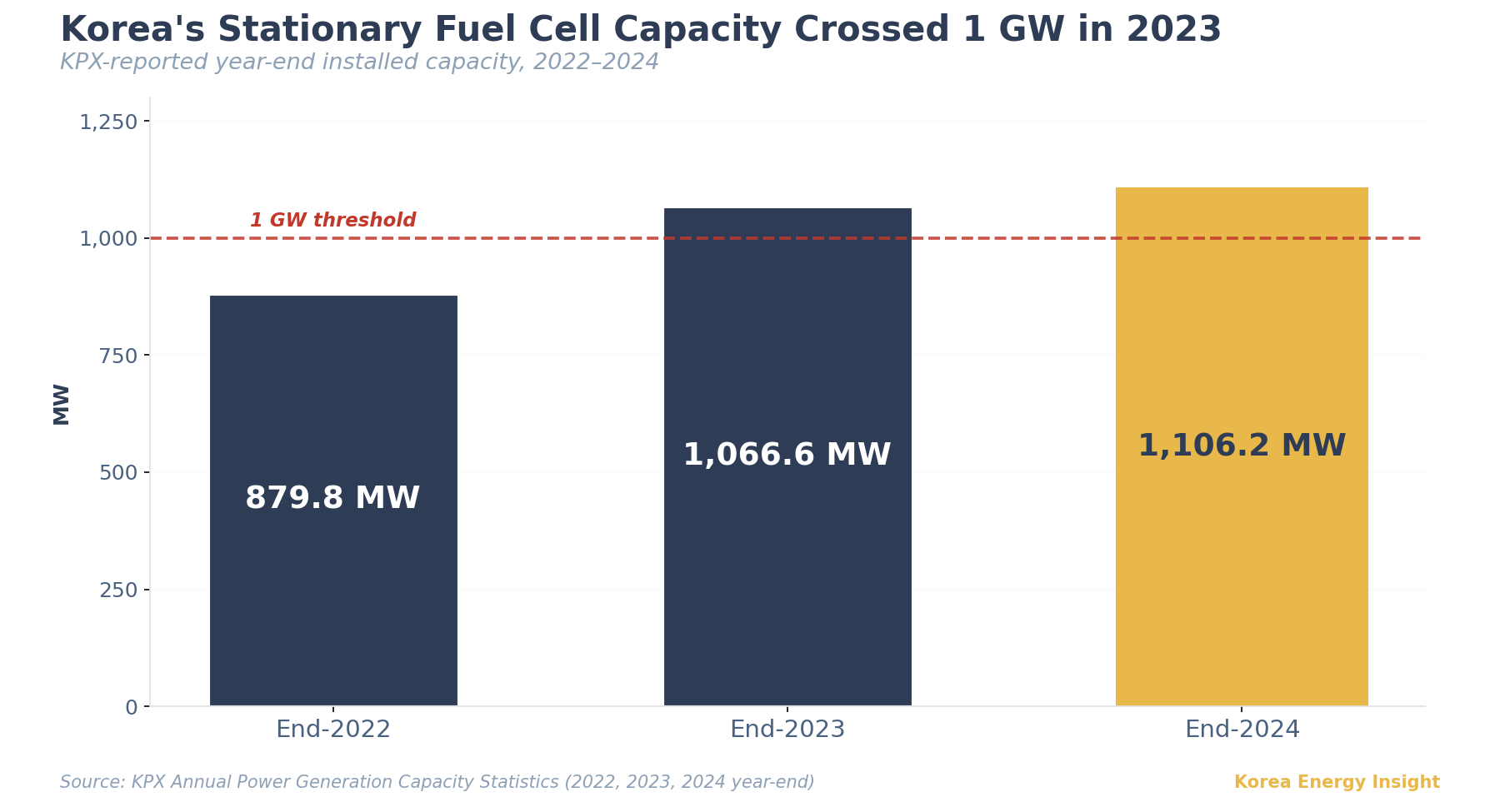

South Korea and the United States remain the two leading markets for stationary fuel cells. The IEA AFC TCP Annual Report 2024 expects the two countries to account for nearly 80% of global stationary fuel-cell MW additions in 2024, though no current public country-by-country breakdown specifically for systems above 200 kW is available. Korea has the world’s deepest utility-scale operating base for stationary fuel cells, anchored by PAFC (Doosan Fuel Cell) and increasingly SOFC through the SK-Bloom channel. MCFC, once a meaningful share of Korean fleet through POSCO Energy’s FuelCell Energy partnership, has effectively exited the market after the supply chain collapsed and O&M became unsupportable. PEMFC strength sits on the mobility side through Hyundai Motor rather than utility-scale stationary deployment. KPX statistics put Korea’s officially reported fuel-cell generating capacity at 879.8 MW at end-2022, 1,066.6 MW at end-2023, and 1,106.2 MW at end-2024.

The Shinincheon Bitdream Hydrogen Fuel Cell Power Plant in Incheon was commissioned in 2021 at 78.96 MW and was the world’s largest operating fuel-cell power plant at the time of completion, and the 107.9 MW Gyeongju hydrogen fuel cell project is pushing unit size further.

The SOFC side still rests on a deep SK-Bloom commercial architecture, even after SK ecoplant materially reduced its Bloom equity position in 2025. SK Eternix develops and operates domestic sites, while Bloom supplies and services the SOFC platform through a long-running Korea partnership.

Why fuel cells spread so fast

Two policy features did the work. The Renewable Portfolio Standard (RPS) assigned fuel cells a REC weight of 2.0 for over a decade, reduced to 1.9 in July 2021 with bonus weightings for byproduct hydrogen (+0.1) and high efficiency (+0.2). And unlike solar (~14% capacity factor, equivalent to roughly 3.4 hours/day of full-load operation under typical Korean conditions) or wind (~25%), fuel cells run at 90%+ availability, or roughly 21.6 hours/day. Before adjusting for REC weighting, that operating-hours differential alone produces about 6 times the annual electricity output per MW. Once REC weights are layered on (2.0 for fuel cells pre-2021 vs 1.0 for general-site solar PV), the effective REC differential was materially higher.

Generation companies (GenCos) formed SPCs around fuel cell projects at pace. Part of this was financial: capex peaked at roughly KRW 7 billion per MW during the height of fuel cell rollout in the early-to-mid 2020s, a level I observed directly while involved in the development of two 20 MW PAFC projects, and recent public project disclosures imply ~KRW 4–5 billion per MW as costs have moved down. Either level required structured financing. Part of it was organizational: each SPC created staffing positions GenCos could fill internally. By the mid-2020s, the perception inside MOTIE was that fuel cells had drifted from policy-supported new technology into an RPS arbitrage product with a convenient employment side-effect. The LNG-based carbon footprint added another layer of resistance, particularly as the Clean Hydrogen Energy Portfolio Standard (CHPS) moved toward implementation.

The current mismatch

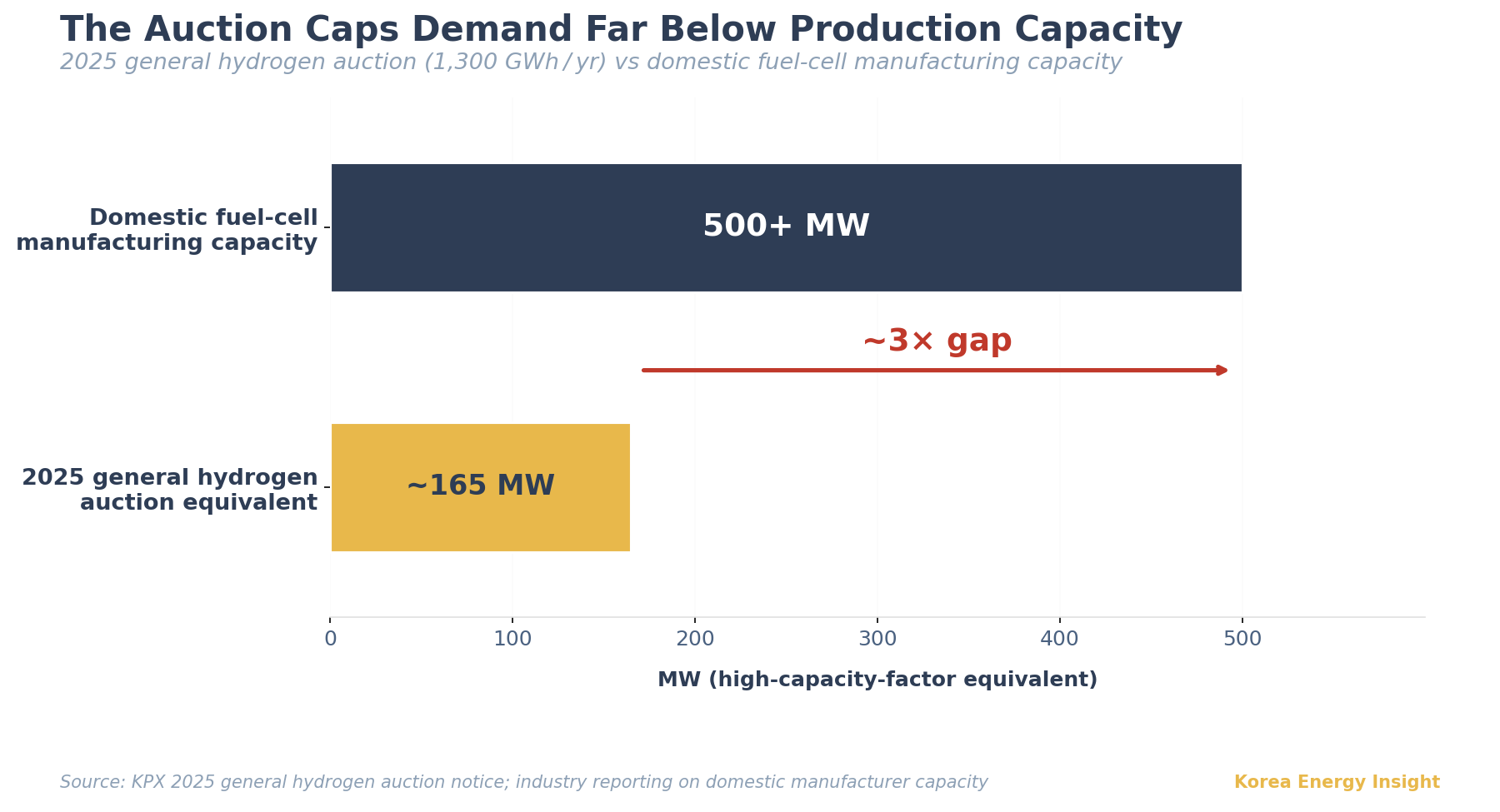

Energy policy authority transferred from MOTIE to the newly established Ministry of Climate, Energy and Environment in October 2025. The new ministry still classifies fuel cells as a distributed energy resource under CHPS, and that classification is enforced through bidding rules. The general hydrogen auction does not impose a hard 40 MW unit cap, but creates an effective 40 MW sizing boundary through distributed-generation scoring. Projects connected to the same substation, and same-owner sites within close proximity, lose distributed-generation points once aggregated capacity exceeds 40 MW. The 2025 general hydrogen auction opened at 1,300 GWh per year, equivalent to less than 200 MW of high-capacity-factor fuel-cell capacity, well below the combined manufacturing capability of Korea’s domestic fuel-cell suppliers.

KPX formally canceled the 2025 clean hydrogen auction on the bid-deadline day, citing replacement by a new notice. Industry reporting linked the move to the new ministry’s reassessment of hydrogen and ammonia co-firing under Korea’s 2040 coal phase-out agenda. As of early 2026, the 2026 general hydrogen auction notice has yet to be issued, with industry reports indicating the ministry is targeting a June notice after April-May consultations and is considering substantial volume reductions or even program termination. A ministry official has been quoted saying that fuel cell-centered hydrogen policy has “low alignment with carbon neutrality” and that “maintaining past volumes will be difficult.” Utility-scale aggregation like the Chungju cluster is allowed but not actively encouraged.

Korea’s fuel cell problem is no longer scale. It is classification.

The adjacent supply gap is what makes that framing harder to defend. Gas turbines are now in global allocation mode: GE Vernova’s combined Gas Power backlog and slot reservations reached 100 GW in Q1 2026, with year-end guidance of 110+ GW, while Siemens Energy has been discussing gas-turbine delivery windows into 2029-2030. Hydrogen turbines are pre-commercial. Korea has essentially no dedicated hydrogen pipeline infrastructure. Against that backdrop, fuel cells are the only natural-gas-fueled dispatchable option already manufactured domestically at scale, already permitted, and already bankable today.

Base case

The Ministry of Climate, Energy and Environment keeps the distributed-generation label in the 12th Basic Plan but adjusts CHPS auction parameters to allow clustered projects like Chungju without procedural friction. Developers extract utility-scale economics from a nominally distributed structure through co-located separately licensed sites. REC pricing under the legacy RPS fleet stabilizes as CHPS absorbs new entrants.

What I’m watching

The next CHPS auction lot size and whether the new ministry introduces a separate utility-scale fuel cell category. Any GenCo-affiliated SPC announcing a 100+ MW single-site development. The 12th Basic Plan’s treatment of fuel cells under firm capacity planning, whether they appear in the firm-capacity line or stay under distributed energy.

What would change my mind

Faster-than-expected hydrogen turbine commercialization or accelerated hydrogen pipeline build-out would weaken the “only dispatchable option” position. Separately, a regulatory move to restrict fuel cell eligibility under CHPS on carbon-emissions grounds, treating LNG-reformed fuel cells closer to LNG combined-cycle than to renewables, would compress the expansion path regardless of supply-side logic.

If this analysis is useful for your team’s Asia strategy, consider sharing it with colleagues evaluating Korean dispatchable power.