Korea's Only Auction-Backed Floating Wind Project Just Collapsed: Why Equinor's Retreat Isn't the Reason

The auction created a price. It did not create a balance-sheet anchor.

MARKET SIGNAL

The auction created a price. It did not create a balance-sheet anchor.

On May 22, Equinor announced it would halt Bandibuli, its 750 MW floating offshore wind project off Ulsan, valued at up to $4.1 billion (KRW 6 trillion; all USD conversions at approximately KRW 1,450/USD). Bandibuli was the only floating project to clear Korea’s government auction, not the only one in the pipeline. That distinction matters: what failed was not an early-stage plan but the one floating project that had already secured a 20-year support award.

The easy read blames Equinor’s global retreat. The company had exited Vietnam, Spain, and Portugal, faced major disruption when its 810 MW Empire Wind 1 build in the US was suspended and later restarted, and was triaging capital across a costlier offshore wind portfolio. All true. But that explains why Equinor was a weaker sponsor. It does not explain why Korea’s offtake structure could not produce a bankable counterparty.

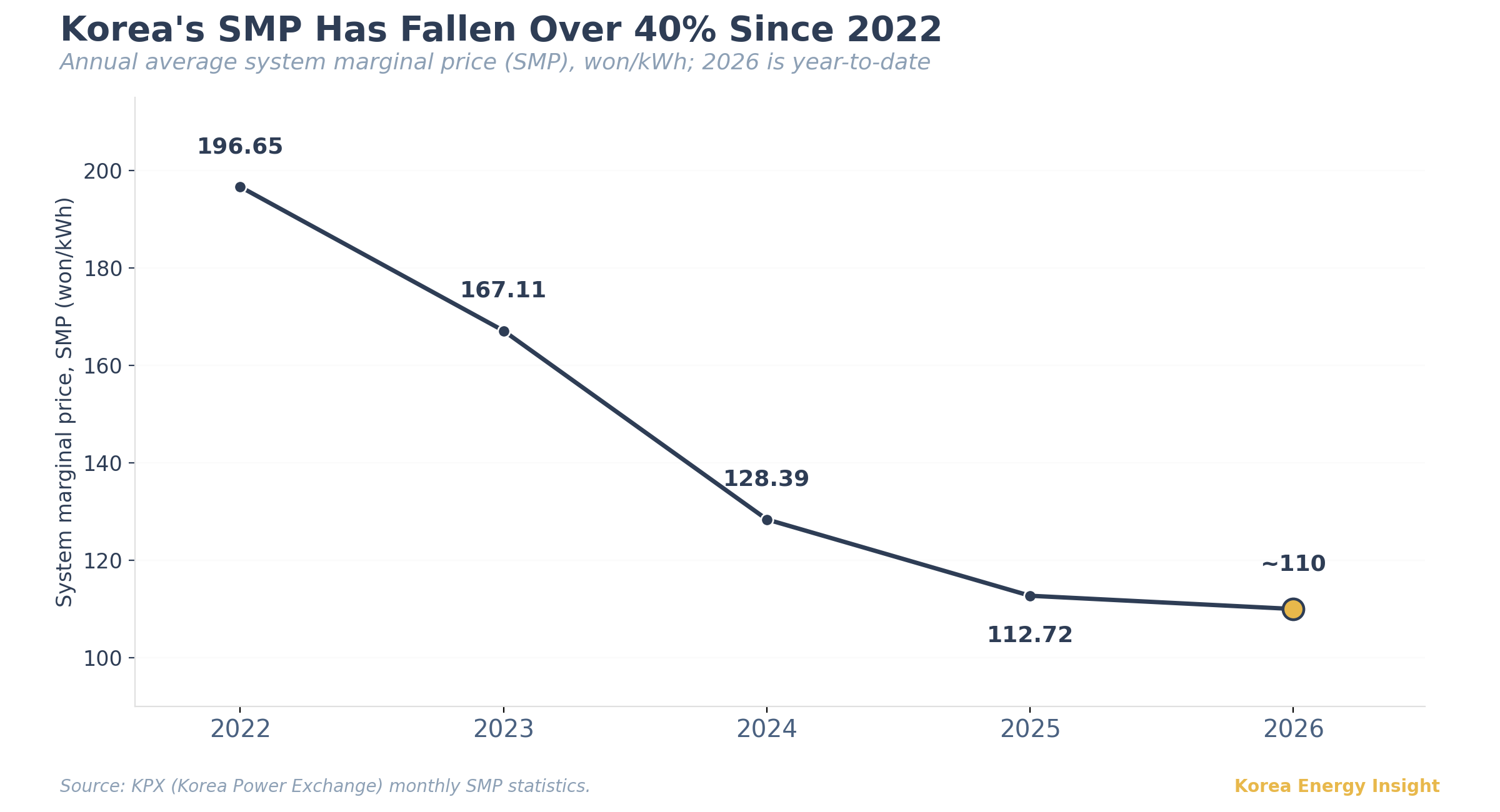

Commercially, the project had already failed at the Renewable Energy Certificate (REC) contract stage. For floating wind, that stage is the project. Korea’s fixed-price contract sets a single price covering both the system marginal price (SMP) and the REC, so a higher winning price means a higher per-REC price.

What the offshore weight changes is volume, not the price of a credit. Far-offshore floating carries a regulatory REC weight the developer cannot choose: one MWh issues one REC at the baseline weight, but 2.5 RECs at a 2.5x weight. That multiplies the revenue a developer earns per MWh — Reuters put the effect at roughly 500,000 won/MWh against the 176,565 won/MWh headline ceiling — but it does not mean the buyer pays 500,000 won for each MWh. The obligor pays per REC, and simply receives more of them. The gap is the weight, not the unit price.

For the obligor, the comparison runs at the credit level, and there floating still loses. The same one REC costs around 177 won under Bandibuli’s 2024 award but about 155 won from a solar fixed-price contract. So an RPS-obligated buyer is asked to pay more for an identical compliance credit, and to do it by absorbing a large, concentrated stream of those credits from a single non-core asset for 20 years. That is the offtake no obligor volunteered to sign.

Korea’s auction does not hand the winner a utility PPA. It grants the right to sign a 20-year REC sale contract with a buyer obligated under Korea’s Renewable Portfolio Standard (RPS). In practice, public generators are the most visible buyers in the competitive REC auctions run by the Korea Energy Agency (KEA), while private obligors can meet much of their obligation through bilateral procurement or self-supply. Those public buyers include the five thermal generation subsidiaries, Korea Hydro & Nuclear Power (KHNP), and the Korea District Heating Corporation (한국지역난방공사, KDHC). A 750 MW floating project did not need a theoretical REC market; it needed one balance-sheet anchor willing to carry the entire weighted-REC exposure. Private obligors have cheaper, more granular ways to meet the same target, so for a project this size the anchor points to a public one.

KHNP was the only publicly visible candidate. It had disclosed Bandibuli as a project under public-enterprise feasibility review, and Korean press reported it was weighing an equity stake of around 20%. The figure cited, roughly KRW 1 trillion ($690 million), was an equity commitment rather than a pro-rata share of the KRW 6 trillion project cost. The review ran through a Korea Development Institute (KDI) process, and it did not finish before the contract deadline. That can be called procedure. But in project finance, procedure is often how a no is expressed. A sponsor that means to anchor a project normally accelerates the approval, asks for a revised deadline, or builds a bridge structure, and none of that surfaced in the public record. For a market read, the absence is the signal.

Policy tried three times. The 2024 auction created a separate floating volume. KEA changed the market rules in August 2025 so a project that missed the REC deadline could seek a substitute-contract extension. After the January 2026 failure, the five-year bidding ban was cut to two. Each intervention preserved Bandibuli’s option value; none produced the balance-sheet counterparty willing to own the weighted REC exposure.

No obligor volunteered because none had to. Solar fixed-price contracts clear near 155 won/kWh, and RPS compliance has long been built around standardized solar and spot REC procurement, not one-off floating concentration risk. The same credit was available cheaper and in granular form, so the anchor seat stayed empty. This is the counterparty problem KEI flagged in its RPS reform analysis, now visible at project scale.

Bandibuli now puts that precedent beyond doubt. The block was never the penalty or the permits. No balance-sheet-constrained public generator would carry a 20-year, above-market weighted REC for a non-core asset, and this time none did. That is the floating version of a signal KEI has tracked since Anma collapsed in April: Korea no longer has only a tariff problem. It has a balance-sheet allocation problem.

Base case

Three floating bids are awaiting the results of the first-half 2026 auction, which closed on May 12: Haeuli 2 (532 MW), Haeuli 3 (560 MW), and East Blue Power (375 MW). They face the same anchor problem. The 2026 auction separated the floating ceiling (175.1 won/kWh) from fixed-bottom (171.2 won), but both still sit above the roughly 155 won solar fixed-price contracts an obligor can source instead. The result will name winners. Whether any winner can also name an RPS-obligated buyer willing to sign the weighted-REC exposure is the real test. If a floating project clears without one, the Bandibuli precedent still controls.

What I'm watching

Whether any 2026 floating winner names an RPS-obligated anchor before signing rather than after. Whether KHNP and Korea Midland Power (KOMIPO), the public generators that reportedly reviewed Bandibuli, repackage the capacity through a domestic-sponsor structure like Sinan-Wooi, where policy capital absorbs the first-mover risk. And whether the approaching RPS sunset pushes obligors to anchor the last 20-year contracts or abandon floating entirely.

What would change my mind

A public generator signing a 20-year floating offtake at the 2026 ceiling. That would mean policy-directed anchoring can override the capital math, and floating's bankability gap is narrower than Bandibuli suggests. Equinor returning as a minority holder under a Korean-led structure would change the read in the same way.

If your team is underwriting Korean offshore wind, forward this to whoever owns the offtake question before the next auction result lands.