Grid Bottleneck Broke the Coal Valuation Model: Korea's $897M Receivable

PF underwriting assumed baseload runs. Korea's East Coast corridor broke that assumption.

DEEP DIVE

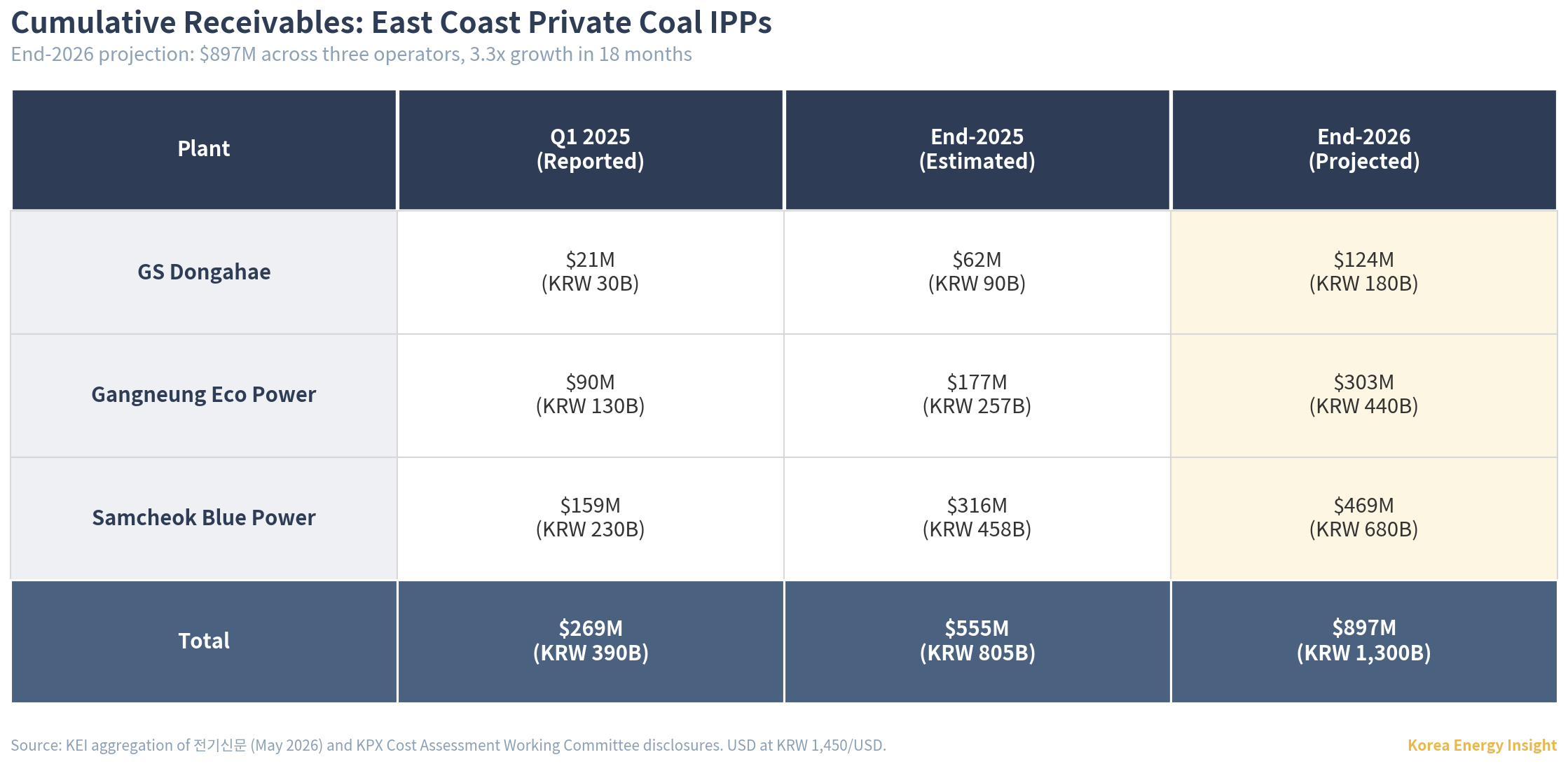

Three East Coast private coal IPPs — GS Dongahae Power, Gangneung Eco Power, and Samcheok Blue Power — are projected to close 2026 with combined accumulated receivables of about $897 million (KRW 1.3 trillion; all USD conversions at approximately KRW 1,450/USD). The figures come from 전기신문 reporting on the most recent Cost Assessment Working Committee (비용평가실무협의회) meeting, citing industry sources. These are not legacy plants squeezed by decarbonization but relatively new project-finance assets stranded by delayed transmission.

This is not primarily a coal profitability story. It is a grid-risk allocation story inside a regulated wholesale market — not a formal grid charge, but the economic effect of a grid constraint warehoused as unrecovered regulated revenue on private IPP balance sheets. The proximate cause is utilization. The structural cause is who holds the grid constraint cost.

For Samcheok Blue, the cumulative receivable now exceeds one full year of projected settlement revenue.

Global context

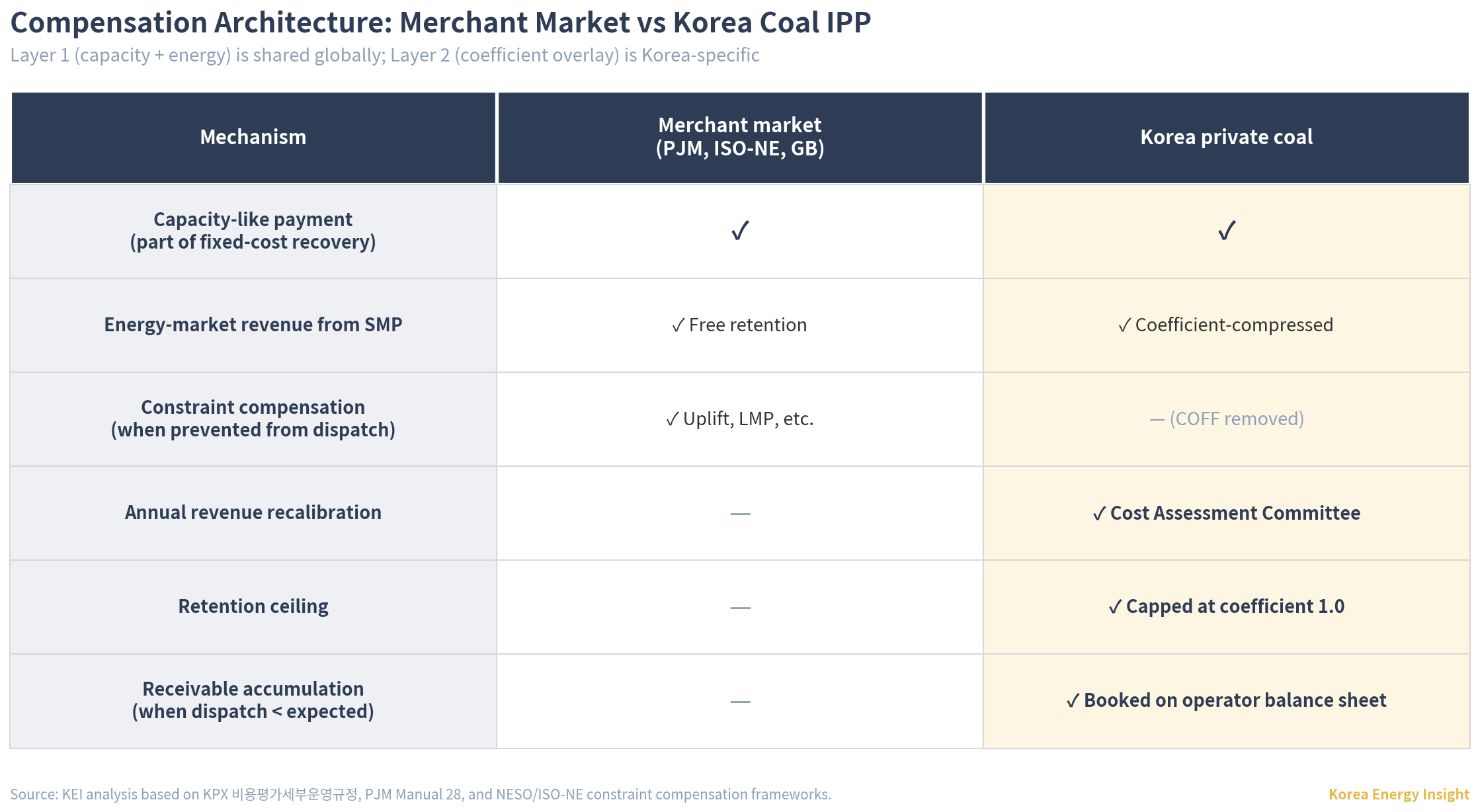

In several comparator markets, transmission constraints are either priced, compensated through operator actions, or made visible through published constraint frameworks. PJM and MISO use uplift payments calibrated against the day-ahead LMP that constrained-off generators would have earned. The UK’s Constraint Management Payments operate on similar logic. Australia’s NEM makes congestion visible through constraint equations and published constraint reporting, though routine network constraints do not automatically translate into generator compensation. Even in regulated cost-of-service markets, fixed cost recovery for utility assets is decoupled from short-term energy market dynamics. The utility’s revenue base is set in the rate case, and energy market volatility affects customer billings rather than asset cash flows.

Korea did not begin as an outlier. The original cost-based pool (CBP), in place from 2001, included a constrained-off payment (COFF) for units scheduled to generate but prevented from doing so by grid or thermal constraint. Within the CBP framework, COFF compensated the operator at SMP minus variable cost for the foregone output, with explicit settlement rules.

Reforms around the real-system-based day-ahead market in the early 2020s reduced the role of COFF, redirecting funds toward reserve-capacity payments for units actively running. The policy rationale was that COFF compensated dispatch producing no system value. The unintended consequence: operators facing prolonged grid constraint no longer have a compensation pathway.

COFF removal closed one compensation pathway. But the receivable mechanism itself — both how it accumulates and whether it can recover — runs on the settlement adjustment coefficient. In Korean private coal economics, the coefficient is the operative variable. KPX’s Cost Assessment Committee sets it each year, and while accumulated receivables can raise it toward 1.0, the ceiling caps further upward adjustment.

In a merchant marginal-pricing market, absent a contract or regulatory clawback, dispatched low-variable-cost units generally retain the clearing-price spread. Korea’s coefficient, an administrative scaling factor calibrated annually to bring revenue toward a regulated target, compresses that retention. The coefficient is calibrated against expected dispatch, not realized dispatch. And there is no separate constraint payment for output lost to grid bottlenecks. The combination is unusual: an administratively-priced wholesale market where the operator bears the gap between forecast and reality, with no merchant upside available to amortize the deviation.

These are two separate problems. The absence of constraint compensation matters only while grid bottlenecks suppress dispatch. The settlement adjustment coefficient compresses upside even after dispatch normalizes. The first is a transmission-timeline issue. The second is a market-design issue that persists regardless of grid completion.

This matters beyond Korea. As more markets approach high renewable penetration with delayed transmission buildout, the question of where integration costs are booked becomes urgent. Korea is increasingly cited as a benchmark for grid-constrained energy transitions. Its answer — book the constraint cost on private balance sheets — is one institutional response among several. Whether that response holds as the integration burden grows is the diagnostic question this article opens.

How the mechanism actually works

Korea’s private coal framework calculates a recognized-cost target. Recognized cost covers fixed costs and the regulated return on those costs. Variable-cost margin — the spread between SMP and a plant’s variable cost — is not part of it. Actual cash recovery toward recognized cost is constrained by the settlement adjustment coefficient (민간정산조정계수) and its 1.0 ceiling. When realized revenue falls short of recognized cost, the gap accumulates as a receivable (미수금).

The coefficient is a regulated settlement overlay set ex ante by the Cost Assessment Committee (비용평가위원회). Each year, the committee forecasts how much the operator should earn in the spot market over the coming year. It then calibrates the coefficient to bring that forecast revenue in line with recognized cost, subject to a hard ceiling of 1.0. The operator’s annual revenue is pre-calibrated to a regulated target, not left to clear at SMP.

By merchant-market standards this is anti-market by construction. In PJM, EU energy markets, or similar pay-as-clear wholesale systems, the clearing price is the price. Merchant pay-as-clear markets do not normally apply a plant-specific settlement coefficient of this kind.

The structural reason traces to Korea’s cost-based pool. LNG frequently sets the marginal price. Coal, with much lower variable cost, would otherwise earn the spread between SMP and its own cost on every dispatched hour. That infra-marginal rent — my reading of the economics rather than official regulatory language — is what the coefficient is built to compress.

The asymmetry is the coefficient ceiling. When actual settlement comes in below the committee’s forecast, for example when grid constraints suppress dispatch below projections, the operator receives less than recognized cost. The shortfall accumulates as a receivable.

The receivable is supposed to be recovered through next year’s coefficient, which the committee can set higher to make up the prior gap. But the coefficient is capped at 1.0. When the prior receivable plus the current year’s expected gap would require pushing the coefficient above that cap, the system has no upward room. The unrecovered portion rolls forward indefinitely.

That coefficient was designed for a margin problem. The current problem is volume.

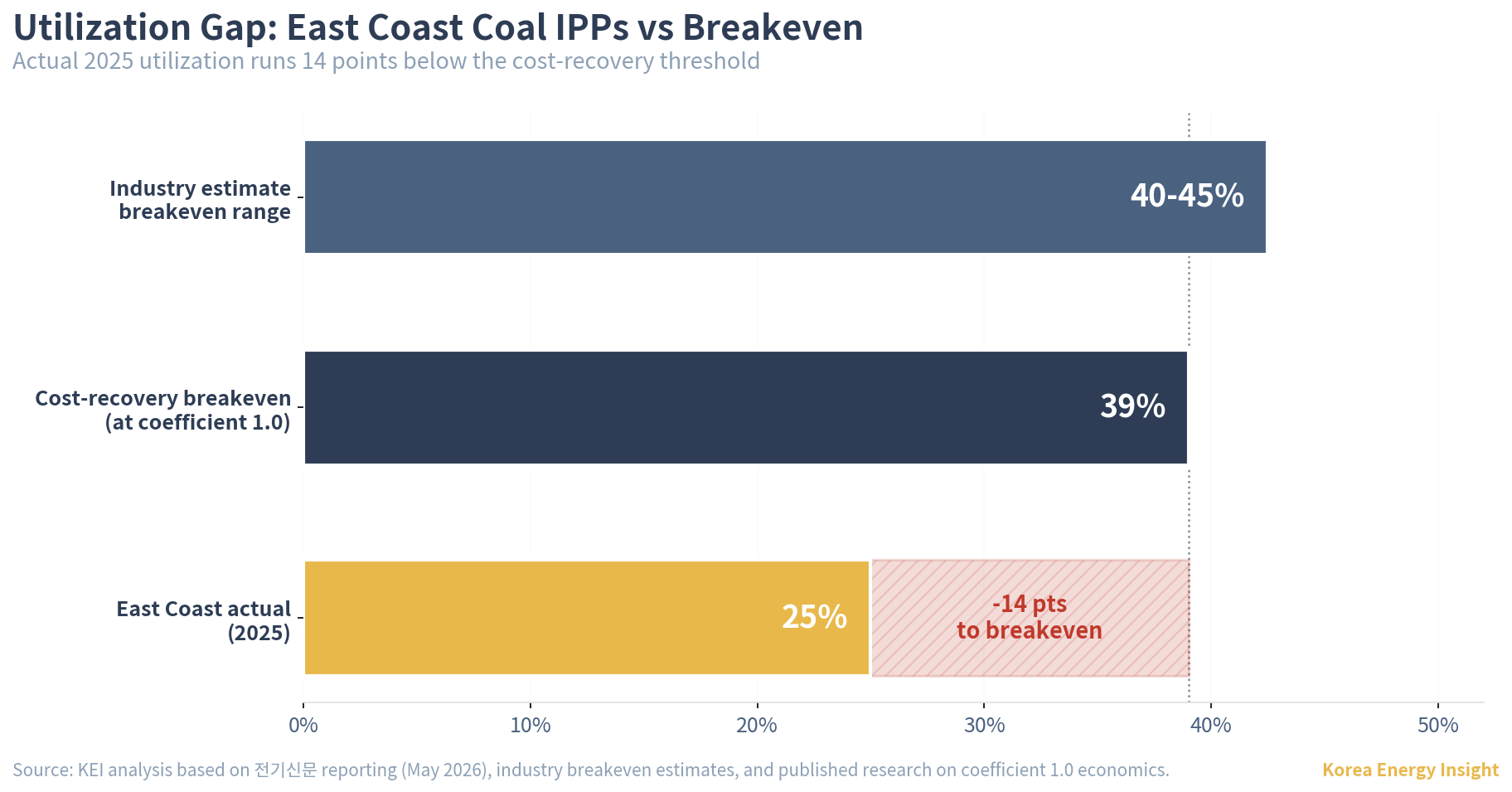

Industry estimates breakeven utilization for these assets at 40–45%. Published research places the threshold near 39% when the coefficient is set at its 1.0 ceiling. Reported actual East Coast private coal utilization, per 전기신문 industry sources, sits around 25%, roughly half of breakeven. The driver is not primarily margin. It is the delayed Donghae-Singapyeong transmission corridor, which can override fuel-cost merit-order economics for East Coast units.

When line capacity is insufficient, the unit is constrained off the grid (계통제약). There is no separate regulatory compensation for output lost to that constraint. Even at coefficient 1.0, the cap with no clawback whatsoever, the math does not turn positive. The compensation framework assumes a level of dispatch that grid constraints have repeatedly prevented.

The 2024 rule change removed the time value

The Cost Assessment Committee’s October 25, 2024 amendment changed how prior-year receivables are handled in each year’s coefficient calculation. The relevant KPX rule text, as amended through the private-coal coefficient chapter, specifies that existing accumulated receivables are prioritized for recovery before any current-year cost recovery is applied. Industry sources read the amendment as turning the receivable into an interest-free, open-ended balance. The published KPX rule history confirms the private-coal coefficient amendment, but the interest-treatment characterization is industry-reported rather than directly quoted from the rule text.

The amendment also defined the recovery path. The Committee sets each year’s coefficient to include receivable amortization in the target, raising the coefficient closer to 1.0 than it would be without the backlog. The operator’s additional retention is directed to clearing the accumulated balance rather than to profit — future upside is mortgaged against current backlog. The 1.0 ceiling binds. When expected settlement is too low for the coefficient to reach recognized-cost-plus-amortization even at 1.0, the receivable cannot be reduced that year.

Economically, the change makes the receivable look less like an interest-bearing regulatory asset and more like an open-ended recovery claim, with amortization contingent on grid completion. That completion is more uncertain than the published timeline suggests.

Two delays compounding: line and substation

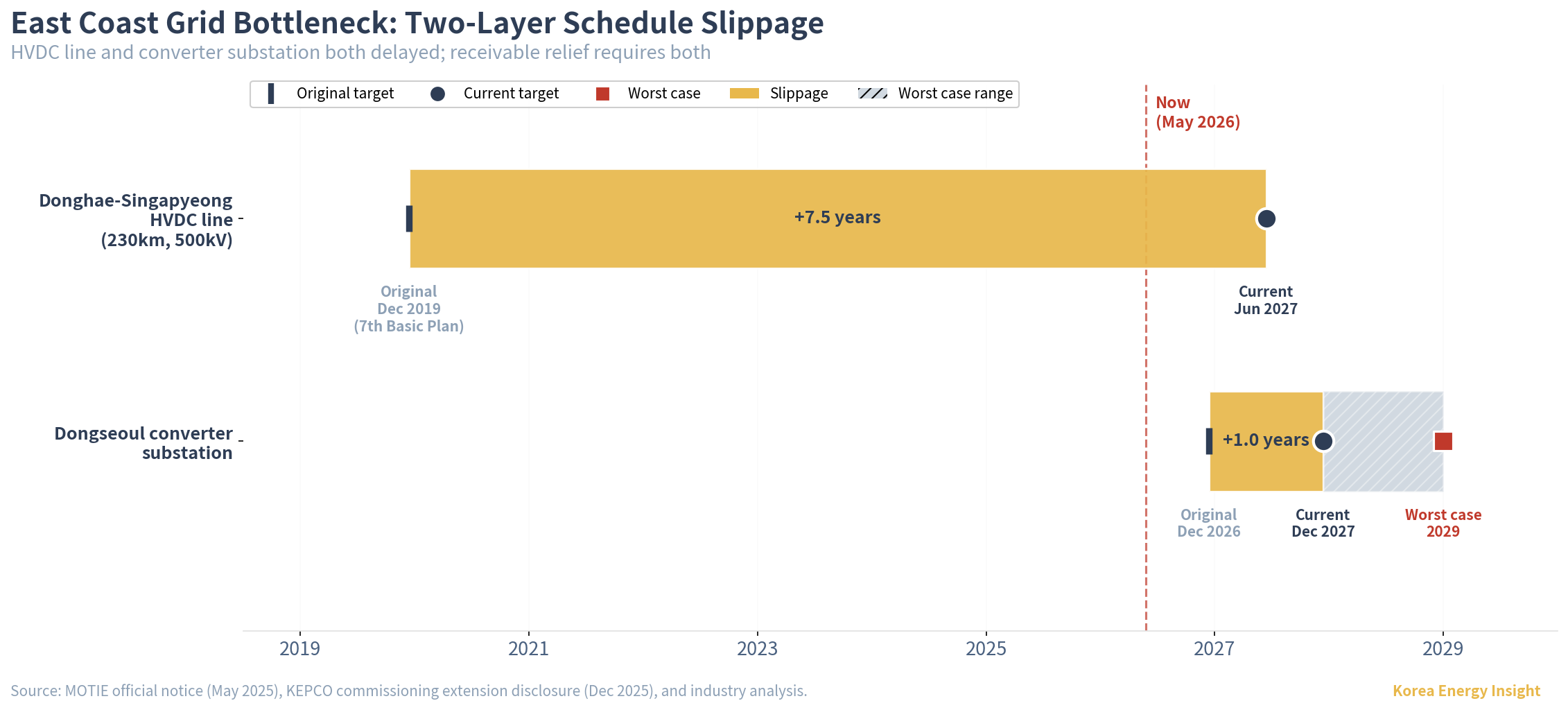

The published June 2027 date should be treated as a section-level schedule for the Donghae-Singapyeong HVDC project, not as a guaranteed full-system relief date. That target itself has already been revised from earlier component-level targets of June 2025 and June 2026 — the line is years behind original schedule and remains uncertain. Even if the revised line target holds, power cannot reach the metropolitan grid without the converter substation at the other end of the corridor.

The Dongseoul converter substation in Hanam city, Gyeonggi province, translates HVDC into AC for the metropolitan network. Without it, line completion does not translate into the intended metropolitan transfer capacity, regardless of when the line reaches mechanical completion.

The substation has been blocked at the local permitting level for over a year. Hanam city denied all four construction permits in August 2024, citing electromagnetic-field concerns, urban planning, and missing community consent procedures. The Gyeonggi Province administrative adjudication commission ruled the denial improper in December 2024. Hanam continued to delay through 2025, granting only conditional visual-design approval in August 2025 after KEPCO had run its application through a third iteration.

The relief mechanism is the National Grid Infrastructure Expansion Special Act (국가기간 전력망 확충 특별법), enacted in March 2025 and effective from September 2025. In November 2025, the government designated Dongseoul substation among 99 national grid projects under the Act, moving it into a central approval and permit-deeming framework. Even with that designation, KEPCO has formally extended substation commissioning from December 2026 to December 2027.

Industry analysis points to 2029 as the worst case if local opposition continues to find procedural friction. The original 2015 7th Basic Plan target was 2019. Under the worst-case scenario, the corridor runs a full decade behind original schedule.

Comparable Korean transmission projects suggest treating any published timeline, for either the line or the substation, as a planning aspiration rather than a binding milestone. The Miryang 765kV line and the 345kV Buk-Dangjin–Sintangjeong line both ran years past initial schedule. The last of those took 21 years to complete, 13 years behind plan.

The receivable amortization path described above requires both delays to clear. Until the line is operational and the substation can receive its output, East Coast dispatch cannot recover toward the coefficient calibration’s expected level. The coefficient cannot reach recognized-cost-plus-amortization at the 1.0 ceiling. Any reduction in the receivable would be tactical; structural amortization requires both bottlenecks to clear.

Implications

The structure produces three implications, ranked by what they challenge in conventional valuation.

First and most distinctive: these assets carry cost-of-service intent but merchant-style dispatch exposure. Their compensation operates in two layers, only one of which is global standard. The first layer is shared with PJM, ISO-NE, and GB: capacity payments cover part of fixed costs, with baseload and mid-merit units recovering the rest from inframarginal rent. The second layer is Korean-specific: the settlement adjustment coefficient compresses inframarginal rent administratively.

When SMP runs at $200/MWh and coal variable cost is $50, PJM grants the full $150 spread per dispatched hour. Korea grants only (coefficient × $150). The coefficient is calibrated each year to bring expected revenue to the regulated target, normally trimming margin downward. In years of margin shortfall it rises further, but cannot exceed 1.0. Shortfall beyond that cap accumulates as a receivable.

Upside is bounded by fixed costs plus the regulated return on those costs. The receivable is eventually recoverable, but deferred recovery materially damages IRR. PF underwriting understands this recovery mechanism.

What the model gets wrong is the dispatch assumption. Standard PF models assume baseload thermal runs at full output outside planned outages, applying variable-cost margins and the coefficient against that runtime. Grid constraint breaks the dispatch assumption. Both the coefficient calibration and the receivable mechanism rely on it.

Two consequences follow. The asset has underperformed beyond what PF underwriting could reasonably price ex ante, producing an unexpected drag on the original investment thesis. And operator self-help — efficiency gains, cost discipline, refinancing — cannot close the gap. The binding constraint is external. Recovery requires the grid program to deliver, not the operator to optimize.

Second: Korean thermal project-finance assets carry grid-execution risk that other markets allocate to the system operator through constrained-off compensation. Sponsor due diligence, EPC risk allocation, and refinancing assumptions all shift when this risk sits on the sponsor’s balance sheet rather than the operator’s. Few comparable Asian thermal IPPs carry grid-buildout risk at this scale.

Third: for foreign PE evaluating Korean energy infrastructure, the real exposure is to Korean grid execution and KEPCO regulatory discretion, not to the underlying generator. Modeling the full grid is not feasible in standard valuation work. What is feasible is verifying the transmission line capacity and substation context that connect the asset. Coastal coal demonstrates that this verification was insufficient at underwriting. That check sits on a different axis of due diligence than asset-level analysis.

A series-level pattern sits on top of these. Korea’s market design lets the state utility absorb fuel-price shocks (Issue #2, on the Hormuz LNG transmission mechanism). The same architecture works on the private coal side, just with grid constraint as the shock instead of fuel price.

The difference is funding access. KEPCO issues bonds against an implicit sovereign backstop. The project-finance SPCs behind the three IPPs do not have that backing, even where a state-owned GENCO holds minority equity (KOSEP owns 29% of Gangneung Eco). The bottleneck suppressing East Coast coal dispatch is not mechanically identical to the bottleneck that traps renewable curtailment cost inside Jeolla (Issue #12), but both belong to the same pattern: the system cost of delayed grid investment is held outside transparent network pricing and pushed into private or quasi-private balance sheets.

What to watch

The base case is receivables continuing to accumulate through at least 2027, more likely 2028. Samcheok Blue Power’s public bond curve provides the most visible reference point for how Korean credit markets price stranded-grid risk, though 2025 issuance was absorbed orderly through oversubscription.

Three indicators determine when the base case shifts.

Credit spreads on private coal IPP bonds vs KEPCO comparables. Material widening means the bond market is pricing the receivable as permanent rather than amortizable. This pushes IPP refinancing costs up and recalibrates Korean energy PF spreads industry-wide. Pressure surfaces first in 2026 maturities.

Extended outages at East Coast nuclear units. The Donghae-Singapyeong corridor shares capacity between the Hanul/Shin-Hanul reactor fleet (8.7GW combined) and the three private coal IPPs, with nuclear effectively taking priority in dispatch and corridor allocation. An unplanned outage exceeding 90 days at any reactor temporarily lifts coal utilization above the 25% reference and slows receivable accumulation. Shin-Hanul 2 was offline from March to August 2025 (five months, reactor coolant leak), the most recent test of the mechanism. The effect is bounded: a short-cycle cash flow adjustment, not a structural fix. Shin-Hanul 3 and 4 (due 2032-2033, 1.4GW each) will tighten the corridor further once commissioned, removing this relief channel.

Dongseoul converter substation commissioning. Any formal extension beyond December 2027 moves the worst-case 2029 scenario to base case. The recovery case shifts from near-term normalization to a 2030s duration trade. The valuation implication is direct: present-value discount of expected recovery moves materially, and the three IPPs become long-duration distressed assets rather than near-term recovery plays.

The substation is the most consequential of the three. Until it enters operation, the coefficient calibration cannot meet recognized-cost-plus-amortization at any setting, and any reduction in the receivable is tactical rather than structural.

If this analysis is useful for your team’s Korea coverage, forward it to a colleague.