Korea Just Passed Its First AI Data Center Law: Easier Permits, Not a Lower Power Bill

The two routes that could lower it — LNG and nuclear — were both cut.

MARKET SIGNAL | Image: SK Telecom’s AI data center booth at Mobile World Congress 2025, Barcelona. (Source: SK Telecom Newsroom)

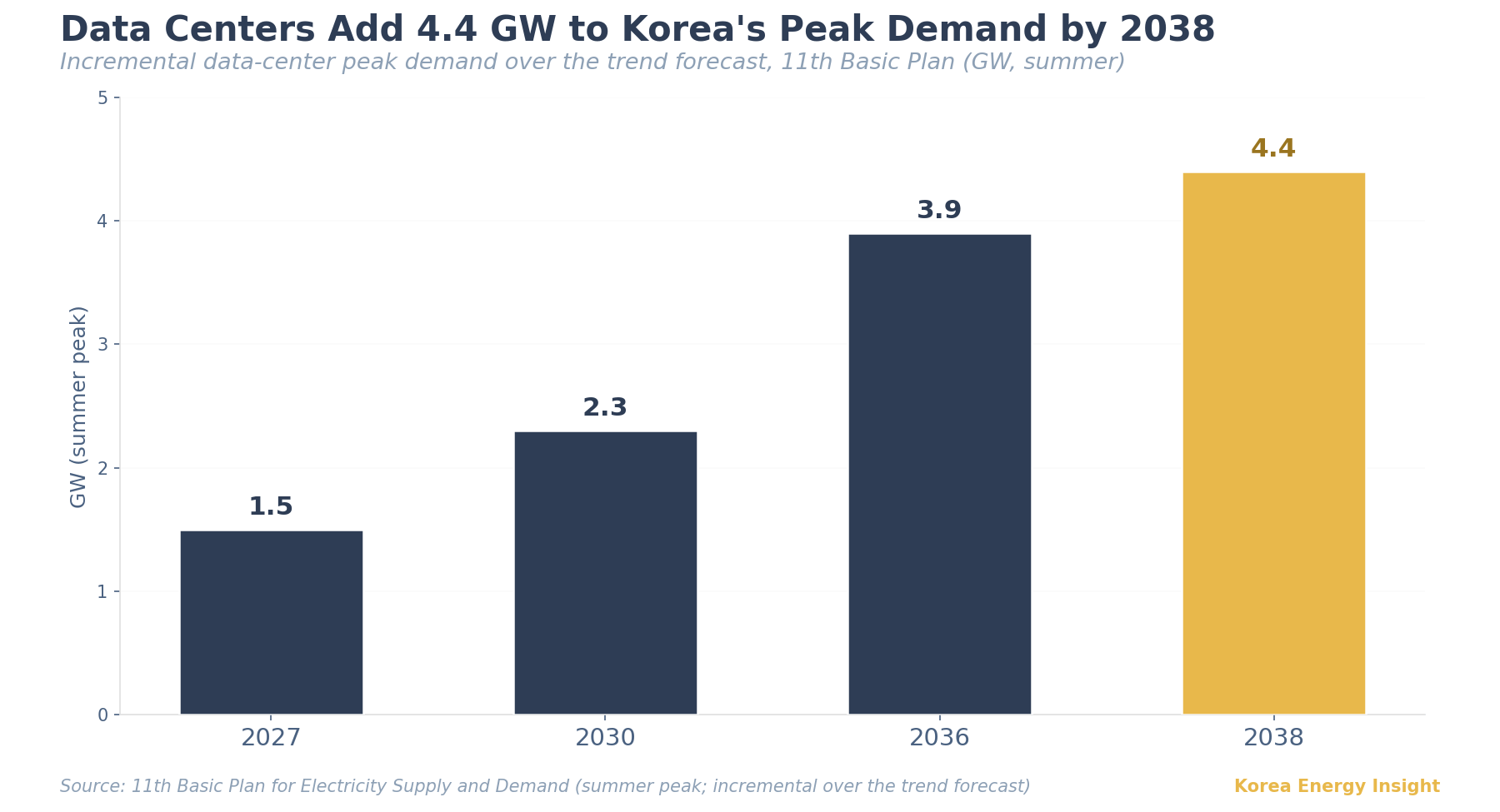

On May 7, Korea’s National Assembly passed the AI Data Center (AIDC) Special Act, the legal centerpiece of the government’s bid to become a top-three AI power. Five days later, the Ministry of Science and ICT (MSIT) and the new Ministry of Climate, Energy and Environment signed an agreement to support data center power supply through the national grid. The 11th Basic Plan for Electricity Supply and Demand, Korea’s binding decadal power roadmap, folds that load into the national forecast: it adds 4.4 GW of data-center peak demand by 2038, roughly three large reactors of new load. The headline is procurement. The mechanism is permitting: the Act shortens the path to grid access, but it does not lower the delivered cost of electricity.

The US frame doesn’t transfer. There, the AI data-center bottleneck is often firm capacity — interconnection queues and local constraints push buyers toward gas turbines, nuclear restarts, and SMRs. Korea’s policy problem is different. The government is trying to move load out of the congested capital region toward surplus supply elsewhere; Honam alone generates roughly 26 GW against about 9 GW of peak demand (KEPCO). Outside the capital region, serving the load physically is not the hard part. The binding number for the projects the law is trying to create is the delivered won per kWh.

The Act’s effective relief sits on the approval side. A one-stop window lets developers bundle the grid-impact assessment, the energy-use plan consultation, and the building permit. A timeout clause then deems those approvals granted if regulators do not reject them within the statutory windows — 150 days for the grid-impact assessment, 90 days for the energy-use consultation. Projects below a set size outside the capital region are exempted from the grid-impact assessment under the Act’s non-capital-region carve-out. For developments that sat in permitting limbo for years, this is a material change.

But the relief lands oddly. The grid-impact exemption is reserved for the non-capital regions, the very places that, thanks to surplus supply, already had the fewest connection problems. Demand, though, concentrates in the capital region: Korea’s industry ministry expects 82% of new data centers there through 2029, where the grid is congested and the exemption does not apply. So the Act’s strongest siting relief goes where it was least needed. That is by design: the policy aim is to push data centers out of the capital region in the first place.

On the electricity bill itself, the Act does not move the recurring cost stack. It can trim some development friction — funding support and priority access to power, water, and road links — but those are not a delivered-won/kWh discount.

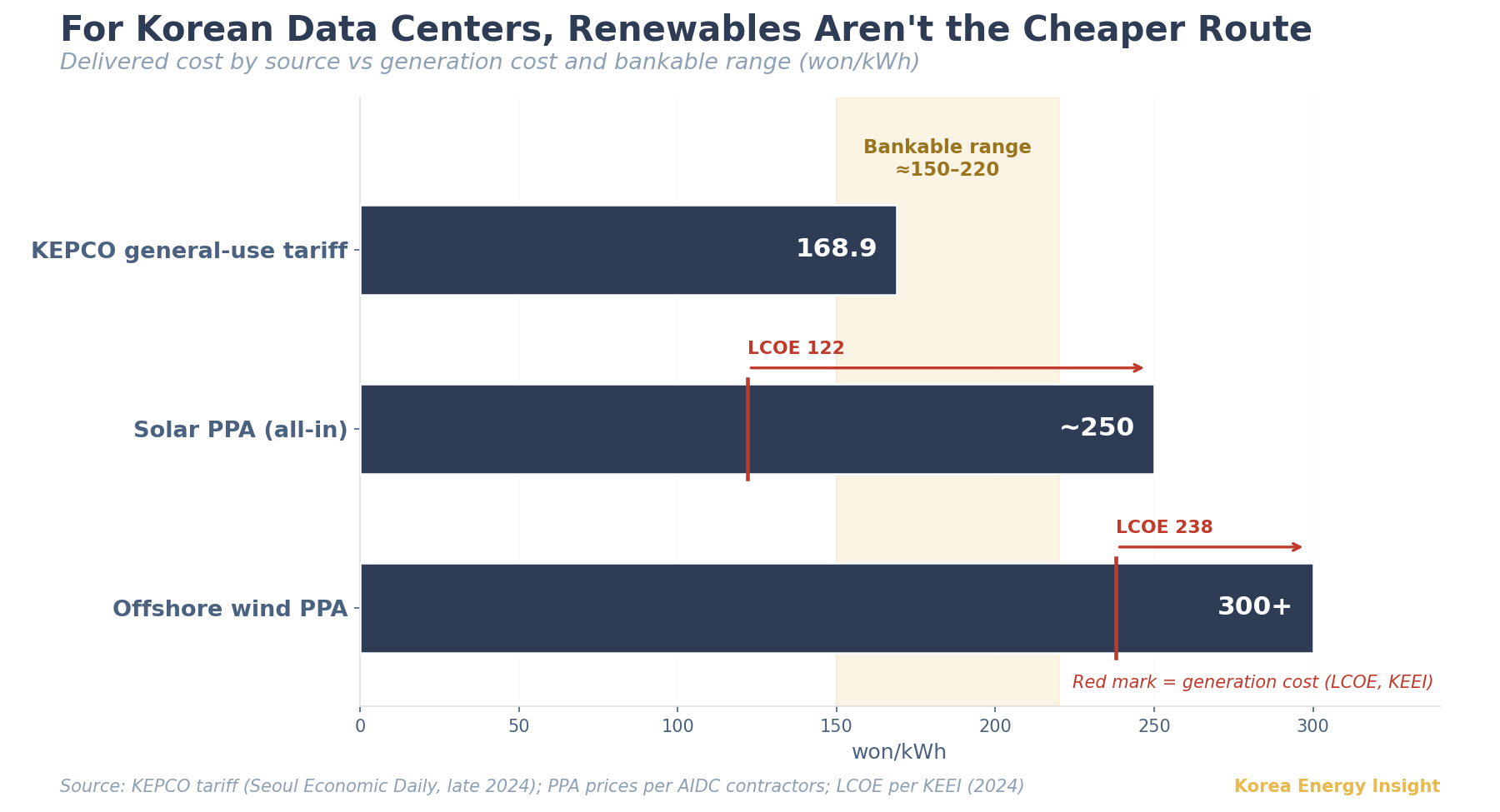

The procurement clause is narrower: renewable generators can sell directly to data-center operators, bypassing the wholesale market. But that right already existed under the 2021 Electricity Business Act, so the clause largely restates it. And renewable supply is no bargain. By AIDC contractors’ estimates, all-in renewable supply runs around 250 won/kWh for solar and above 300 for offshore wind — well over the 150-220 won/kWh band operators describe as bankable. The gap is the negotiation, not the resource: the Korea Energy Economics Institute puts solar’s levelized cost at 122 won/kWh and offshore wind’s at 238, so direct-PPA pricing adds more than 100 won/kWh over generation cost. What remains is the applicable KEPCO tariff: the general-use rate for data centers reached 168.9 won/kWh in late 2024, up about 31% from early 2022.

The missing provisions matter more: nuclear was cut early, LNG struck later.

LNG was raised but struck in the Legislation and Judiciary Committee. The stated reason was the grid burden of tying dedicated gas capacity to one site. The reading underneath — interpretation, not the official line — is stranded-asset risk. The 11th Basic Plan keeps adding gas capacity through coal-to-LNG conversions, yet LNG’s generation share falls from 25.1% in 2030 to about 11% by 2038. Plants expected to run fewer hours each year are weak anchors for twenty-year offtake contracts, and the government appears to be holding that line.

Nuclear was on the table and taken off it. When the science committee passed the bill, the direct-PPA carve-out covered renewables and LNG; SMRs and other nuclear were excluded and deferred to “later discussion.” Commercial nuclear output stays inside the KEPCO/KPX single-buyer market, so the Act opened no channel for a data center to contract reactor output directly, let alone host a private unit. The government does not yet appear ready to accept private nuclear. So even as US hyperscalers sign direct deals with reactor operators and SMR developers, a Korean data center’s only route to nuclear power runs through the KEPCO tariff. For operators, the practical result is simple: the Act can move a project through permits faster, but the tariff still carries the investment case.

Base case. The Act was sent to the government on May 29 and is not yet promulgated; a June cabinet vote and promulgation would put the nine-month commencement clause around early 2027. From there, it shortens non-capital-region permitting, but procurement economics stay where they are. New large clusters that move outside the capital region still underwrite on grid power at the applicable KEPCO tariff, unless the decree creates a new AIDC-specific treatment. The renewable direct-PPA clause sees little real uptake while its all-in cost stays above the bankable band.

What I’m watching.

The enabling decree, due before commencement: whether it gives the renewable PPA bankable terms — network-charge treatment, eligibility thresholds, settlement rules — beyond the 2021 right it currently restates.

The data-center tariff through 2026: every won of increase widens the gap a renewable PPA has to close, and deepens grid dependence.

Any follow-up bill that restores direct LNG procurement or opens a nuclear route.

What would change my mind. If the decree carves out tariff relief, such as a network-charge exemption for AIDC renewable PPAs, the renewable route could pencil out and the cost read softens. Or if a later bill restores direct LNG procurement or opens a nuclear route, the bill-side calculus shifts and grid dependence eases.

This is a siting-and-permitting law, not a power-price one. If your team is modeling Korea’s AI infrastructure buildout, the delivered electricity tariff is the assumption that decides the case. Forward this to whoever owns the tariff line.