KEPCO Bond Yields Are Flashing an Early Warning

The 2025 profit buffer is thinner than it looks. The power sector has no backstop.

MARKET SIGNAL

KEPCO (Korea Electric Power Corporation) posted $9 billion (13.5 trillion won) in operating profit in 2025 — a clear recovery from the $32 billion (47.8 trillion won) cumulative operating losses accumulated between 2021 and 2023. The question is no longer whether KEPCO escaped its debt crisis. It is how quickly the Hormuz shock can reverse that recovery.

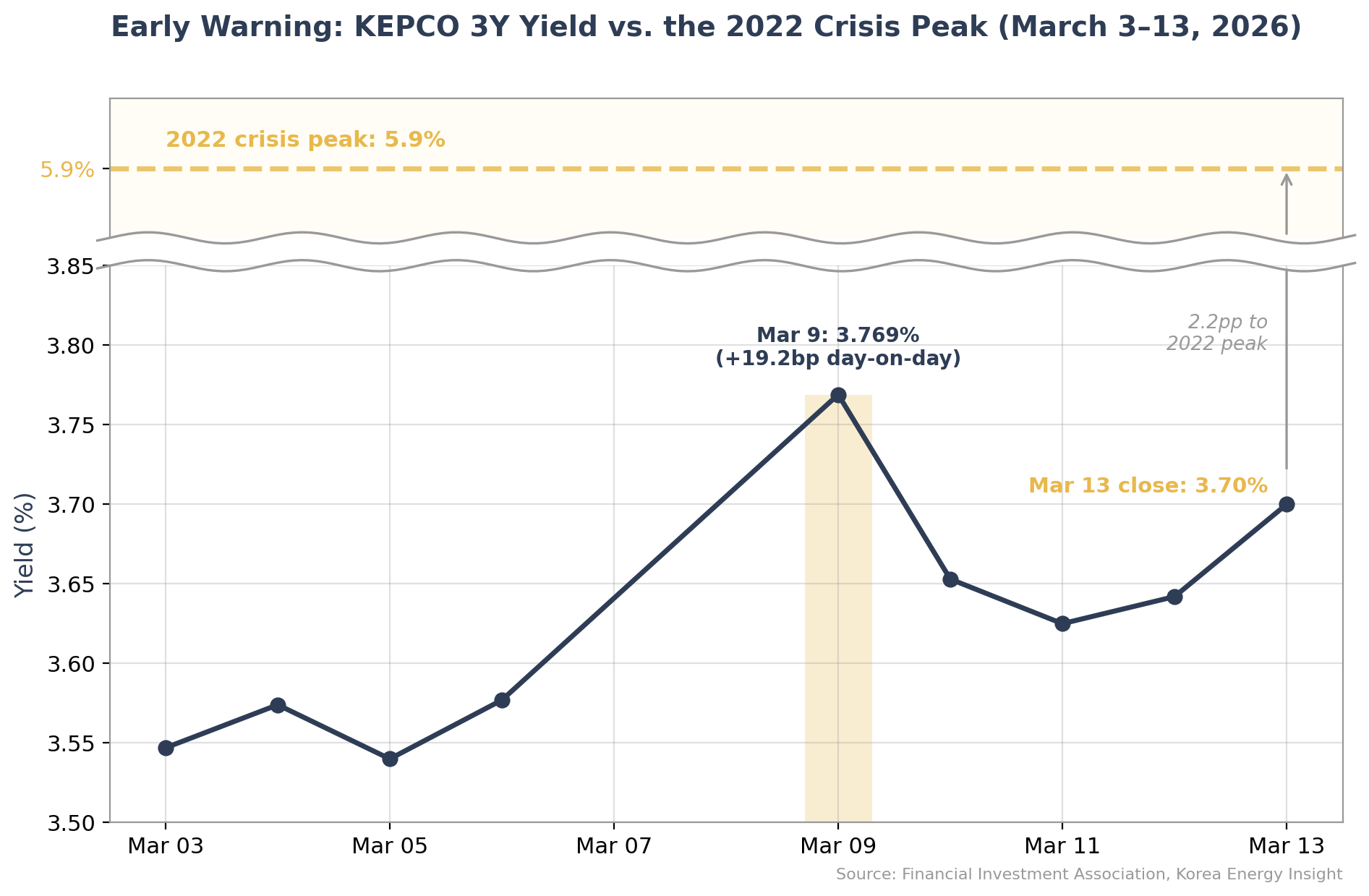

The bond market is not waiting for an answer. KEPCO 3-year bond yields spiked 19.2 basis points on March 9 alone, closing at 3.769% — the sharpest single-day move since the crisis began. From March 3 to 13, yields rose 15.3bp in total and have stayed in the 3.6–3.7% range since. The macro backdrop is different from 2022: US Treasury yields are trending down in Q1 2026 and the Bank of Korea is holding rates steady, rather than hiking aggressively. This is not yet a 2022 rerun. But the structural vulnerability — KEPCO's dependence on bond issuance to fund politically frozen tariff gaps — is unchanged, and participants who lived through that episode are watching closely for the first signs that it could become one.

The transmission mechanism is already visible. Front-month JKM (Japan Korea Marker) futures jumped from $13.37/MMBtu on March 2 to $15.77 on March 3 and have sustained above $16 since. Korea’s daily SMP (System Marginal Price) responded with a lag: 112 won/kWh in the first days after the strait closure, then 116.75 on March 11 and 121.49 on March 12 — roughly 6% above the February average of 108.52 won/kWh. This is the spot market reacting. The larger hit comes later: the majority of Korea’s LNG is purchased under oil-indexed term contracts with a three-to-six-month repricing lag. If Brent sustains above $90 through Q2, the full cost increase feeds into KEPCO’s wholesale purchase bill in Q3 and Q4.

KEPCO’s 2025 profit provides a buffer — but a thinner one than the headline suggests. Q4 2025 operating profit fell 18% year-over-year. Debt stands at $137 billion (205.7 trillion won). Borrowings are $86.5 billion (129.8 trillion won). Annual interest costs alone exceed $2.7 billion (approximately 4 trillion won) — nearly a third of last year’s operating profit. The bond issuance limit — expanded to 5x capital and reserves after the 2022 crisis, with an emergency override to 6x under ministerial approval — sunsets at the end of 2027. Any new loss cycle burns through headroom that cannot be renewed without another legislative act.

Since Korea introduced wholesale market competition in 2001, no administration has immediately passed fuel cost increases through to retail tariffs. That pattern has held through every fuel price spike and every change of government since. On March 13, the government announced an industrial time-of-use tariff restructuring — lower daytime rates, higher nighttime rates, weekend discounts — effective April 16. This is a rebalancing of the existing rate base, not a net increase — unless the fabs run 24 hours a day. For semiconductor manufacturers like Samsung and SK Hynix, nighttime operations cannot be shifted to daytime. The 5.1 won/kWh nighttime increase hits them directly, making the restructuring a de facto rate hike for Korea’s most export-critical industry. But because the restructuring is designed to be revenue-neutral for KEPCO — daytime cuts offset nighttime increases — it does not materially close the gap between wholesale purchase costs and retail tariff revenue.

Beyond the restructuring, tariffs remain frozen. The Q1 fuel cost adjustment remains at +5 won/kWh. The Q2 adjustment has not been announced, but industry reporting points toward another freeze.

Meanwhile, the government’s $67 billion (100 trillion won) stabilization program is a financial market liquidity facility — aimed at bond, equity, and foreign exchange markets. The $6.7 billion (10 trillion won) supply chain stabilization fund is dedicated to crude oil procurement, not LNG or power. As of mid-March, no fiscal measure directly addresses the channel through which higher LNG costs feed into SMP and onto KEPCO’s balance sheet. The power sector has no dedicated backstop. The tariff freeze and the absence of any electricity-specific fiscal response confirm the pattern: the government’s priority is shielding consumers, not protecting KEPCO’s margins.

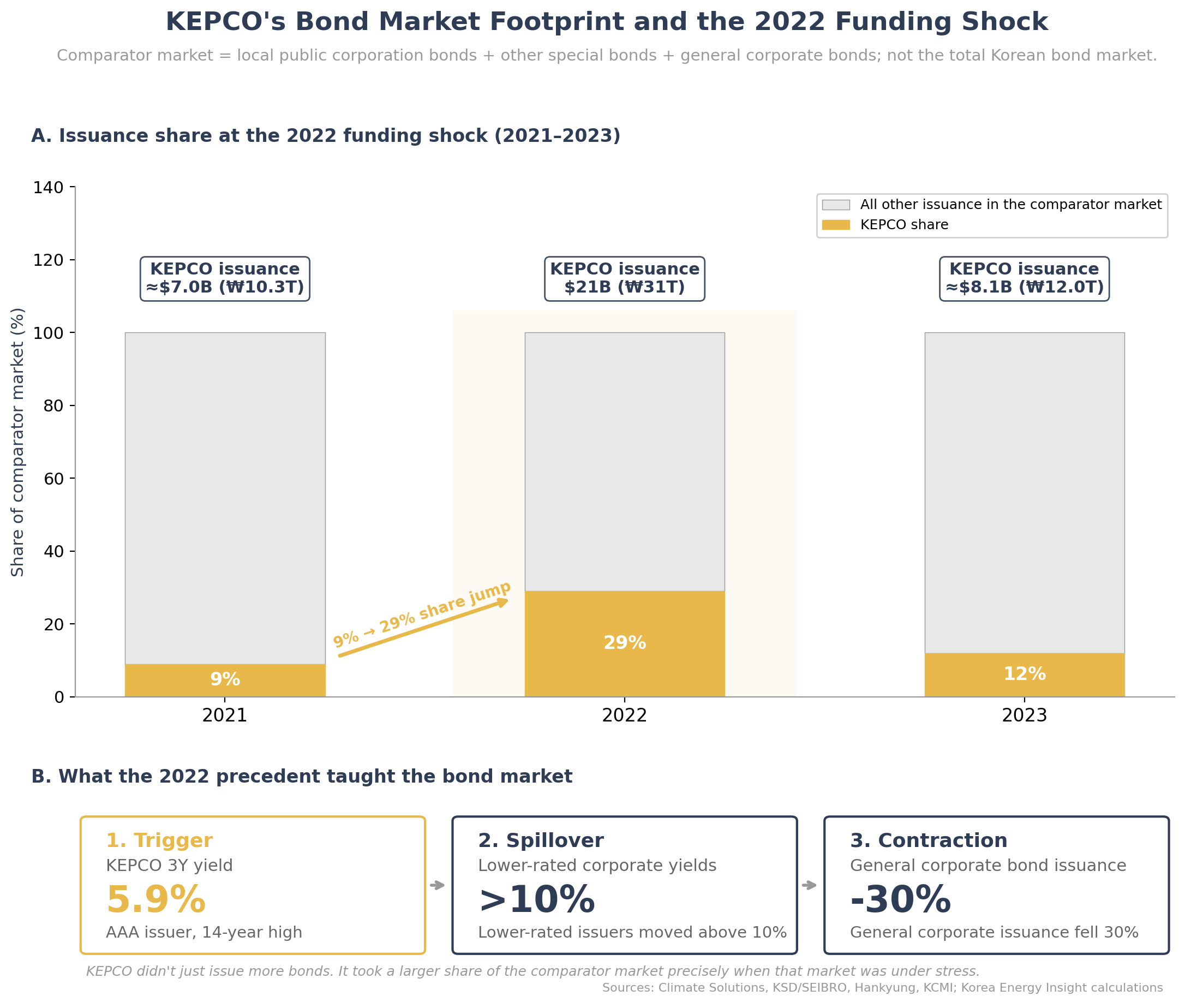

The 2022 precedent is the reason the bond market reacts before KEPCO posts a single quarter of losses. When KEPCO accumulated $32 billion in operating losses between 2021 and 2023, it issued $21 billion (31 trillion won) in bonds in 2022 alone — ttripling its share of Korea's comparator bond market (local public corporation bonds, special bonds, and general corporate bonds) from 9% to 29%. KEPCO yields hit 5.9%, a 14-year high for a AAA issuer. KEPCO was a major amplifier of a credit market already stressed by the Legoland provincial guarantee default and a sharp rate-hiking cycle. The crowding-out effect pushed borrowing costs above 10% for lower-rated corporates. General corporate bond issuance fell 30%. The lesson the market took: KEPCO does not need to default to destabilize Korea's credit market. It just needs to issue.

Base case: KEPCO’s 2025 surplus absorbs the initial shock. But if Brent sustains above $90 through Q2, oil-indexed LNG contracts reprice in Q3–Q4, pushing KEPCO back toward operating losses by late 2026. With tariffs politically frozen, KEPCO resumes net bond issuance. The 2022 crowding-out scenario does not repeat at full scale — KEPCO’s starting position is stronger and the rate environment is different — but credit spreads widen and marginal corporate issuers face higher borrowing costs.

What I’m watching:

KEPCO bond spread vs. AAA corporate benchmark — the 2022 inversion, when KEPCO yields exceeded those of AAA corporates, is the early warning signal

Q2 fuel cost adjustment announcement (expected late March) — another freeze confirms the political constraint is binding

Monthly SMP trajectory — if the March average exceeds 115 won/kWh and April trends higher, the wholesale cost pressure is materializing ahead of the oil-indexed lag

What would change my mind: A rapid Hormuz reopening that brings Brent below $80 before the oil-indexed repricing cycle hits KEPCO’s fuel costs. Alternatively, a surprise Q2 tariff increase of 10+ won/kWh — which would signal the government is willing to absorb the political cost rather than repeat the 2022 debt cycle.

If this analysis is useful for your team’s Korea exposure assessment, consider sharing it with colleagues.