The Battery, Unbundled: Hyundai's Bid to Break V2G's Ownership Barrier

The real barrier to V2G was never degradation. It's who owns the battery.

DEEP DIVE | Image: Hyundai Ioniq 5. (Source: Hyundai Motor Company website)

In April 2026, Hyundai Motor Group announced a battery-subscription pilot: lease the battery in an electric vehicle (EV), rather than sell it. The pitch was affordability. The battery is the most expensive part of an EV, so stripping it out and charging a monthly fee cuts the purchase price sharply. But the structure does something the affordability framing misses. It splits who owns the battery from who drives the car. And that split is what made me look again at a problem I had once given up on.

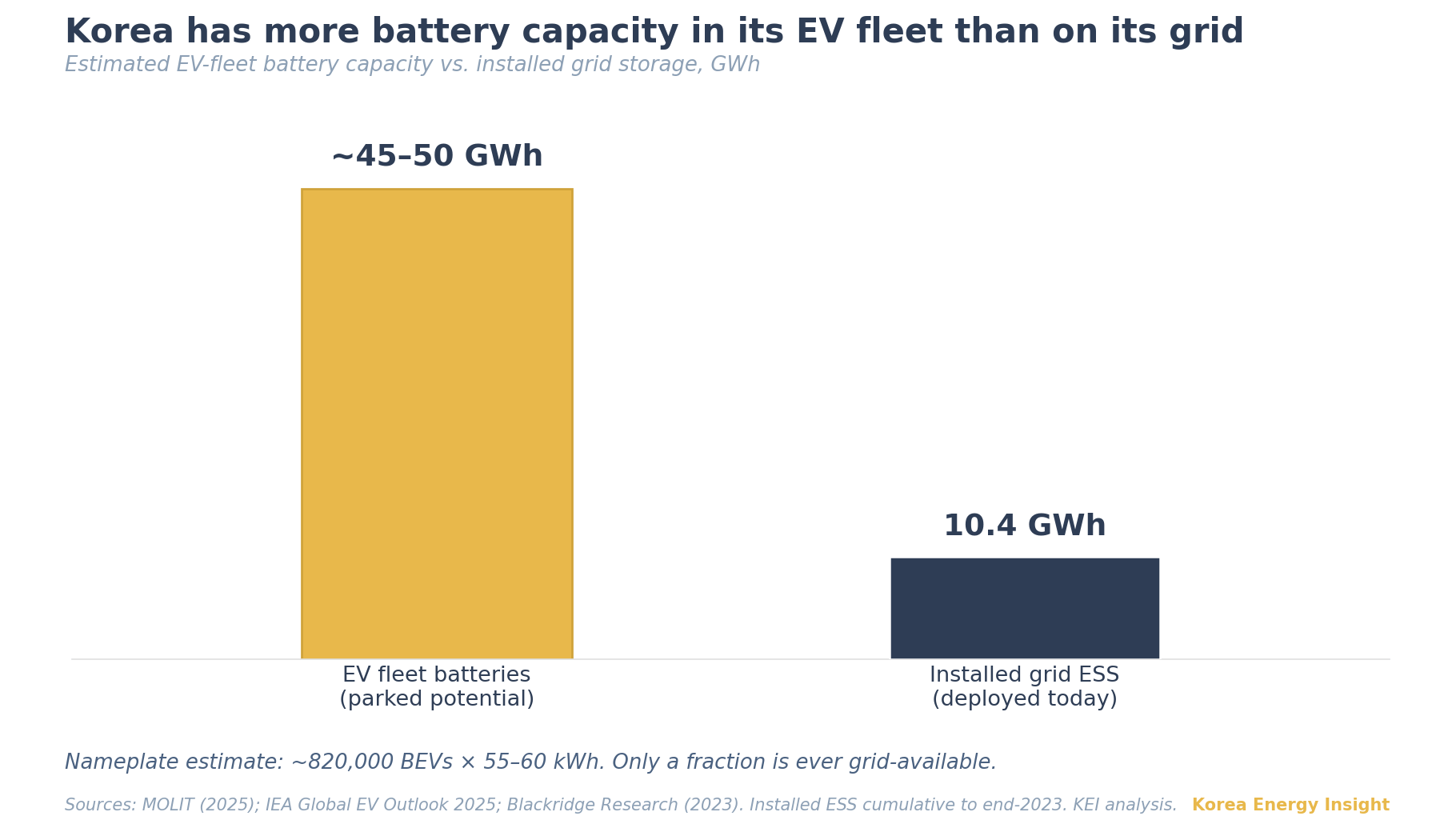

Years ago I worked on bringing EV batteries into Korea’s grid as a flexibility resource, an approach known as vehicle-to-grid (V2G). The effort failed for a reason the engineering models never flagged. The models worried about cycle aging. Owners worried about resale value. The standard pitch — let the grid borrow your battery while you are parked, and earn money for it — assumed owners would weigh revenue against degradation. They did not run that calculation at all. They were protecting the resale value of an asset they intended to sell later, and no payment offer moved them. The battery was a store of value first and a power source second. That single fact, more than any technical limit, kept Korea’s growing EV fleet off the grid.

Global Context

The irony is that the degradation problem is now largely manageable. The International Energy Agency (IEA) reports that battery degradation in well-managed V2G can be limited, and that controlled bidirectional cycling can even reduce capacity loss compared with unmanaged charging (IEA). The engineering objection — that grid duty wears out the pack — is now closer to an outdated assumption than a live constraint.

So why does V2G remain stuck at pilot scale across most markets? A 2026 study in Utilities Policy, coauthored by researchers at the University of Colorado Denver and North Carolina State University, interviewed 42 U.S. V2G stakeholders. The most binding barriers were standardization and interoperability, market development, and infrastructure readiness, with battery degradation a second-tier concern (Utilities Policy). The IEA frames the real friction more precisely: owners need confidence that V2G revenue outweighs any loss in battery value, while manufacturers want to limit warranty exposure. The party that bears the degradation cost is not the party that captures the grid value.

This is an ownership problem wearing a technical disguise. When the person who controls the battery treats it as a personal asset to preserve and captures only a fraction of its grid value, leaving it parked and idle is rational. Korea’s version of this problem is sharper than most, and the reason reveals a structural block that battery economics alone cannot explain.

Korea Situation

Korea’s EV-to-grid story runs into two walls.

The first wall is ownership. The standard policy assumption is that owners will participate once the revenue share is large enough. My own experience in Korea, and that of others in the industry, says otherwise. Owners did not engage with the revenue case at all; they fixed on resale value and stopped there. This rules out the entire “pay them more” approach. You cannot fix a store-of-value instinct with a better payout. The structural fix is to take the depreciating asset off the owner’s balance sheet, so there is no resale value left for them to protect.

The second wall appears even after you consolidate the batteries under a single operator and remove the individual-owner objection. Korean utility operators run their equipment conservatively. A configuration with no operating track record does not get deployed, whatever its economics. Two events hardened this caution. A run of energy storage system (ESS) fires from 2017 — 23 by the end of the government’s investigation — forced tighter safety rules on grid-connected batteries. Then, in August 2024, a parked EV ignited in the underground parking garage of a Cheongna apartment complex in Incheon. Smoke and utility damage affected five buildings, displaced hundreds of residents, and pushed battery risk into public view (Korean fire authorities; local press). Operators who already distrust battery solutions do not volunteer to go first.

Hyundai Motor Group is now moving on both walls at once. Two separate pilots attack the first wall by different routes, while the operating record they generate begins to erode the second. The first pilot is battery subscription. Under a November 2025 regulatory-sandbox special case, the battery can now be registered separately from the car. Hyundai will lease it rather than sell it, starting in the first half of 2026 with five Ioniq 5 corporate taxis. A general-customer pilot is set to follow in the second half (Hyundai Motor Group). The battery is the single most expensive part of an EV. In a 2022 transport-ministry illustration, a Kia Niro EV listed at $31,200 (KRW 45.3 million; conversions throughout at roughly KRW 1,450/USD). The battery alone accounted for about $14,500 (KRW 21 million), close to half the sticker, and stripping it out cut the up-front price to roughly $9,900 (KRW 14.3 million) after subsidy (Korea.kr; MOLIT). Hyundai Glovis, which holds the group’s used-battery rights, runs a parallel taxi program; SR Times reports that batteries returned at the end of service will be reused in ESS or recycled for materials.

The second pilot is V2G itself. In Jeju, enabled by the 2023 Distributed Energy Act and Jeju’s November 2025 designation as a distributed-energy special zone, Hyundai is running a 55-vehicle V2G trial with free bidirectional chargers and free charging (Money Today). The telling detail is the warranty: Electimes reports that Hyundai and Kia are keeping it intact for participants. Read against the first wall, the Jeju design is an admission. By covering the charger, the electricity, and the warranty, Hyundai removes the owner’s entire cost and risk, and the pilot drew more applicants than spots. Owners were never opposed to V2G. They were opposed to bearing its cost.

If removing the owner’s cost is the unlock, China shows where consolidating that ownership leads. NIO built its business on separating the battery from the vehicle. It then turned its swap stations into distributed storage nodes for the grid, providing frequency regulation, peak shaving, and demand response through a virtual power plant (VPP) platform (NIO; CSG Energy Storage). During China’s 2022 summer crunch, 108 NIO stations joined peak-load reduction (CnEVPost). In a December 2025 demonstration near Tianjin, 104 NIO vehicles delivered 1.644 MW on average and 1.741 MW at peak (Tianjin Daily). NIO’s model is swap-based, with batteries pooled in stations rather than left in parked cars, so it sidesteps the bidirectional-charger problem that Hyundai’s fixed-battery model still faces. But the principle holds: once a single entity owns the batteries, they become a dispatchable resource. The track record that stopped Korea a decade ago is exactly what NIO has now built.

Korea’s own policy now points the same direction, with one gap. The First Basic Plan for Renewable Energy, released in May 2026, sets ESS expansion and a distributed-grid transition as priorities, and its distributed-grid measures include a V2G demonstration (First Basic Plan for Renewable Energy). A companion next-generation ESS strategy from the Ministry of Climate, Energy and Environment appeared the same day. It names the second wall directly, making operating track record, public procurement, and safety and certification standards explicit instruments for scaling storage. What neither document addresses is the first wall. Policy treats V2G as a technology to deploy and a track record to build. It stays silent on who owns the battery, which is the part that decides whether any of it scales.

Implications

The sharpest implication is not about V2G at all. It is about second-life storage. Repurposing retired EV batteries into stationary ESS has been held back by both sourcing and economics. Packs arrive with unknown histories, no clean title, and poor data, which makes screening expensive and liability murky (IDTechEx). A subscription fleet inverts the sourcing side. Every returned battery carries a single owner, a complete operating history, and a standardized form factor, because the financier monitored it across its entire first life. That removes the data-and-title barrier that has kept second-life storage at pilot scale. The valuation models that price second-life feedstock have not caught up to the difference a clean ownership chain makes.

But the advantage only goes so far. Second-life packs still perform below new cells and usually have to sell at a discount to compete, while new lithium-iron-phosphate (LFP) costs keep falling. Clean sourcing fixes supply; the economics are a separate fight. The same caution applies to placing second-life batteries in Korea’s ESS central contract market, where payment hinges on sustained availability. Whether degraded packs can hold that standard is an open question, and the contract structure punishes those that cannot.

Beyond second-life, the same fleet has value while still on the road. For aggregators, a subscription fleet is close to an ideal resource. One entity controlling thousands of batteries removes the coordination cost that fragments most VPP portfolios, where operators must contract with many small owners individually. A financier-owned EV fleet is a single counterparty with a single dispatch decision. That is a structurally cleaner aggregation unit than the rooftop solar and behind-the-meter assets Korea’s VPP operators stitch together today.

What to Watch

Whether Hyundai links its subscription and V2G/ESS tracks, which currently run as separate experiments. If the returned-battery pool is formally routed into grid storage, the EV fleet becomes a priced grid asset. If not, those batteries stay unmonetized after vehicle life, and the second-life thesis stays theoretical.

The general-customer subscription rollout planned for the second half of 2026. Taxi pilots test the mechanics; a consumer launch tests whether ordinary buyers accept battery-free ownership at scale. Volume here is the leading indicator for how large the eventual battery pool becomes.

The first commercial deployment a conservative Korean operator signs off on, as opposed to another pilot. That signature, more than any cost curve, marks the point where EV batteries become a real line item in Korea’s flexibility supply.

If this analysis helps your team think through Korea’s storage and EV markets, consider forwarding it to a colleague weighing the same questions.