50,000 GPUs and a Robot Factory: Where's the Power?

The grid won't arrive until 2031. Hyundai's data center targets 2029.

DEEP DIVE | Image: Boston Dynamics Atlas / Boston Dynamics

Hyundai Motor Group signed a $6.2 billion (KRW 9 trillion; all USD conversions at approximately KRW 1,450/USD) investment agreement with the Korean government and Jeonbuk Province on February 27 to build a robot-AI-hydrogen complex in Saemangeum. The headlines were dominated by Boston Dynamics’ Atlas humanoid and GPU clusters. Energy professionals should look at a different line item: the $1.6 billion (KRW 2.3 trillion) in solar and hydrogen infrastructure that will determine whether the rest of the project delivers.

The breakdown tells the story. An AI data center with 50,000 NVIDIA Blackwell GPUs takes $4 billion (KRW 5.8 trillion). A GW-scale solar PV portfolio takes $900 million (KRW 1.3 trillion). A 200MW PEM electrolyzer takes $690 million (KRW 1 trillion). A robot manufacturing cluster — targeting 30,000 units annually, spanning humanoid, logistics, and wearable robots — takes $276 million (KRW 400 billion). An AI hydrogen city takes another $276 million. The energy components account for 25% of total spending but carry most of the enabling risk.

The 지산지소 Model

Hyundai built its pitch around 지산지소 (地産地消) — produce locally, consume locally. Solar PV generates power on-site. That power feeds the data center and the electrolyzer. The electrolyzer produces green hydrogen. The hydrogen fuels trams, buses, and demand-responsive transport within the Saemangeum smart city. The pitch is to keep as much electricity inside the fence as possible (Hyundai Motor Group press release, Feb 27 2026).

This is an attempt at Korea’s first industrial-scale behind-the-meter energy ecosystem. If it works, it bypasses two bottlenecks that have stalled every major Saemangeum investment for half a decade: transmission grid access and wholesale market exposure. The model also addresses Hyundai’s RE100 commitment, providing a procurement path outside the cost-based pool (CBP) where SMP has been trending toward zero during daylight hours — a dynamic KEI covered in Issue #4.

There are larger renewable energy projects in the world. NEOM’s 4GW wind-and-solar complex in Saudi Arabia dwarfs Saemangeum in generation capacity. Australia’s Western Green Energy Hub is targeting 50–70GW. But those are hydrogen export projects. They produce fuel for ships and sell it overseas. They do not run data centers, manufacture robots, or consume their own output on-site. In the other direction, the US behind-the-meter data center boom (Oracle’s 2.3GW Stargate, Crusoe’s 1GW Abilene campus) runs almost entirely on natural gas turbines. I have not found an operating analogue at comparable scale that combines on-site solar, green hydrogen production, AI compute, and advanced manufacturing inside one self-consumption complex. If realized as designed, Saemangeum would be among the first.

The Global Race to Power AI — And Why Korea Can’t Copy It

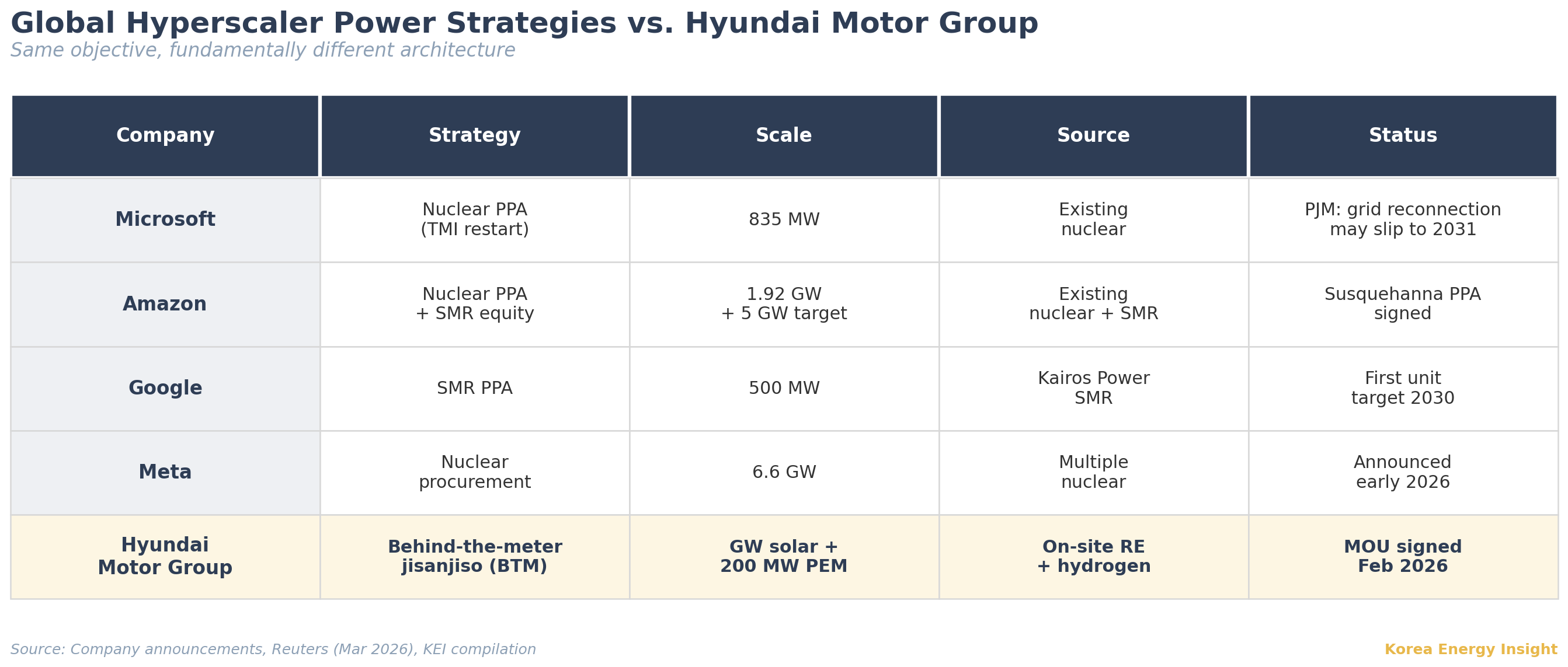

Hyundai’s problem is not unique. Every hyperscale data center operator in the world is scrambling for dedicated, carbon-free baseload power. What differs is the solution set available.

In the United States, the answer has been nuclear PPAs. Microsoft signed a 20-year agreement with Constellation Energy in September 2024 to restart the 835MW Three Mile Island Unit 1 reactor, now renamed the Crane Clean Energy Center. Constellation targets a 2027 plant restart, but PJM indicated in March 2026 that grid reconnection may not be available until 2031 (Reuters, Mar 26 2026). Even in the US, the gap between corporate ambition and grid reality is widening. Amazon, Google, and Meta followed with similar nuclear strategies: Susquehanna (1.92GW), Kairos Power SMRs (500MW), and a 6.6GW procurement plan, respectively. The pattern is consistent: long-term bilateral contracts with nuclear generators, behind-the-meter colocation, or equity stakes in next-generation reactor companies.

Under the current Korean market design, the US hyperscaler nuclear playbook is unavailable to Hyundai. A 2021 amendment to the Electric Utility Act (전기사업법 Article 2, Clause 12-8) created the “renewable energy electricity supply business,” allowing direct bilateral PPAs between renewable generators and consumers outside the wholesale pool. But corporate uptake remains negligible, just 0.04% of total generation as of 2024 (third-party PPA volume as share of total generation; KEI Issue #4). More critically, the law applies only to renewable energy. Nuclear, LNG, and other conventional generators remain locked inside KPX’s single-buyer system. There is no mechanism for a corporate buyer to contract directly for dedicated nuclear baseload. Colocation next to a nuclear plant is legally and practically impossible: Korea Hydro & Nuclear Power (KHNP), a KEPCO subsidiary, operates the entire nuclear fleet; KEPCO holds the T&D monopoly; and no Korean nuclear site has the licensing or physical infrastructure to host a private data center on its perimeter. SMR deployment in Korea is still at the development stage — the i-SMR is targeting export markets first, with domestic deployment years away.

This is the constraint that makes Hyundai’s approach structurally different from what US hyperscalers are doing. Microsoft can contract for existing nuclear baseload. Hyundai cannot. The Korean market offers no mechanism for a corporate buyer to secure dedicated 24/7 carbon-free power from the grid. So Hyundai is building its own power supply from scratch — solar for daytime, hydrogen for storage, fuel cells for dispatch — inside the fence. It is the same objective as Microsoft’s Three Mile Island deal, pursued through an entirely different architecture because the market design leaves no alternative.

The Power Math — And How the Gap Could Close

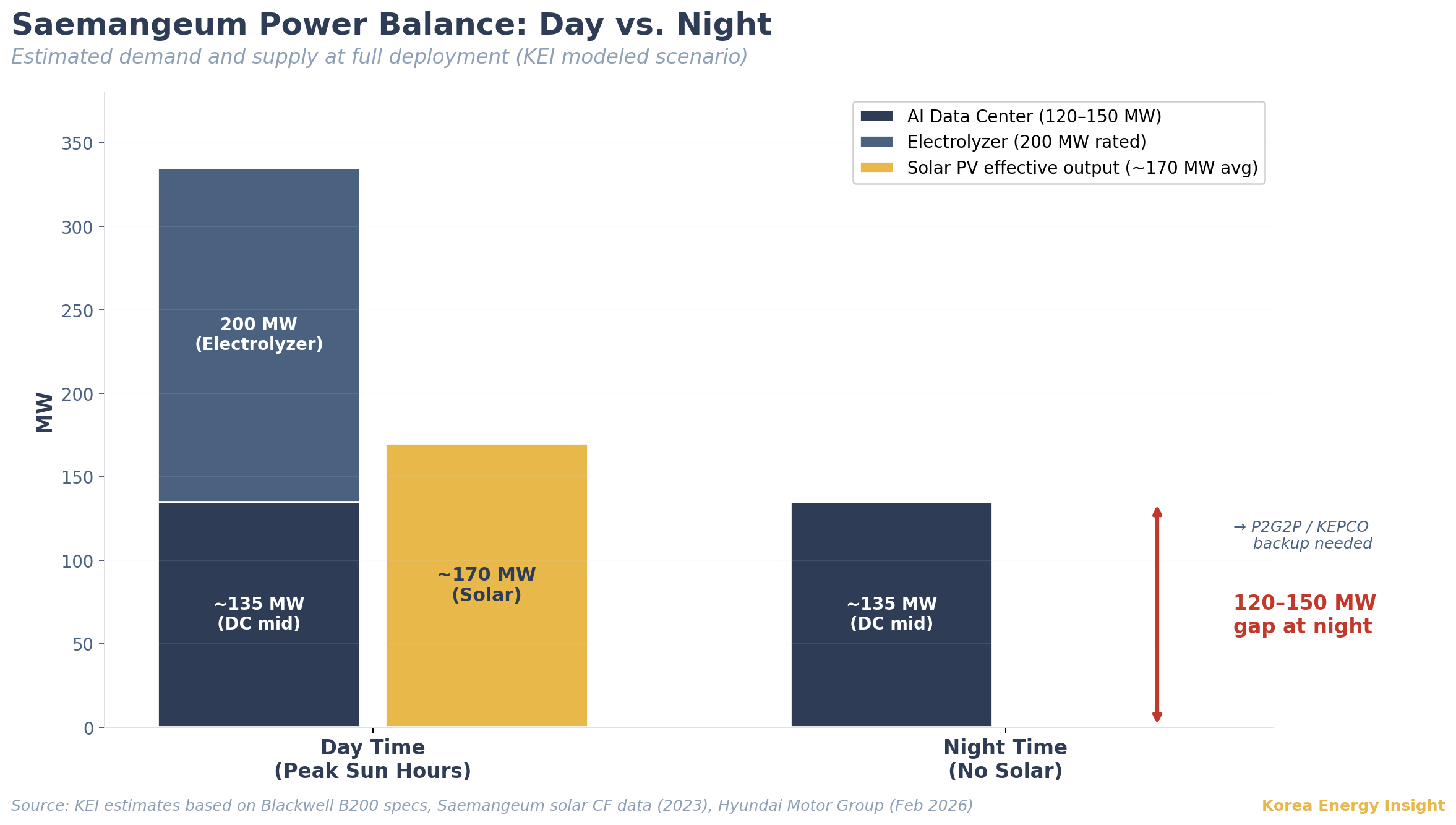

Publicly disclosed: 50,000 NVIDIA Blackwell GPUs. The exact SKU has not been confirmed. If those are B200-class accelerators, each drawing up to 1,000 watts air-cooled or 1,200 watts liquid-cooled, the numbers get large fast. At full deployment, IT load alone would reach 50–60 MW before supporting infrastructure. Add networking, storage, cooling, and facility overhead at a PUE of ~1.3, and modeled total demand approaches 120–150 MW — running 24 hours a day, 365 days a year. The 200MW electrolyzer, when operating at rated capacity, adds another major load. These are KEI estimates based on published GPU specifications, not Hyundai’s disclosed design load.

Saemangeum’s existing 297MW solar PV fleet has demonstrated a capacity factor of approximately 17%, with an average of 4.18 peak sun hours per day — above the national average of 3.72 hours (Saemangeum Development Agency, 2023). A 1GW portfolio at that rate produces an effective average of around 170 MW, but concentrated entirely in daylight hours. At night: zero. During monsoon season: a fraction.

Solar alone cannot serve that load profile. But Hyundai has an asset no other data center developer in Korea possesses: in-house hydrogen fuel cell manufacturing at automotive scale. Hyundai has produced PEM fuel cells since 2013 and remains the world’s largest FCEV manufacturer. The NEXO’s fuel cell stacks have already been reconfigured as stationary generators. In 2021, Hyundai deployed a 1MW system at Korea East-West Power’s Ulsan plant, packaging NEXO-grade modules into two 500kW containers that produce 8,000 MWh annually (한국경제, Jan 2021). The design is modular: output scales linearly by adding containers.

Hyundai has not stated that it will deploy fuel cell power generation at Saemangeum. Publicly, the group has confirmed the electrolyzer and the fuel cell factory. The connection between the two at Saemangeum remains implicit. But the MOU already commits to both an electrolyzer producing green hydrogen and a data center that needs around-the-clock power. Connecting the two through fuel cells is a direct application of technology the group already manufactures and has deployed. If you are already producing hydrogen on-site for mobility and industrial use, routing surplus hydrogen back through fuel cells avoids building a separate storage system from scratch. The hydrogen is already there; the fuel cell converts an existing inventory into dispatchable power. At Saemangeum’s scale and duration requirement — overnight baseload, monsoon-season backup — this long-duration storage logic has a structural advantage that short-duration BESS does not easily match. The cleanest reading is a P2G2P (power-to-gas-to-power) architecture. But that is still an inference from Hyundai’s disclosed asset base, not a publicly confirmed operating plan.

Whether P2G2P works at 120–150 MW scale has not been demonstrated anywhere. KEPCO grid backup will likely still be needed for redundancy. But the availability of this option materially changes the project’s grid dependency compared to SK’s earlier attempt, which had no comparable fallback. What Hyundai has not publicly disclosed is how the data center will actually be powered at night. That is the gap this analysis is reading between the lines to fill.

The backup option goes one step further. If on-site green hydrogen supply falls short — extended monsoon, electrolyzer maintenance, demand surge — the fuel cells can run on hydrogen produced from LNG through a packaged steam methane reformer. LNG-reformed hydrogen does not qualify for RE100 compliance, so it cannot be the default operating mode. But as a contingency fuel source, it means the data center need never be without dispatchable backup. The Saemangeum complex has port access for LNG delivery. For a data center operator, this is the difference between a single point of failure and a layered energy architecture.

In my assessment, the 지산지소 model is not a stopgap while the grid catches up. If Hyundai executes the full solar-hydrogen-fuel cell loop, it may prove to be the more durable architecture, one that works regardless of whether the 345kV lines arrive in 2031 or 2036.

SK Tried This. It Stalled for Five Years.

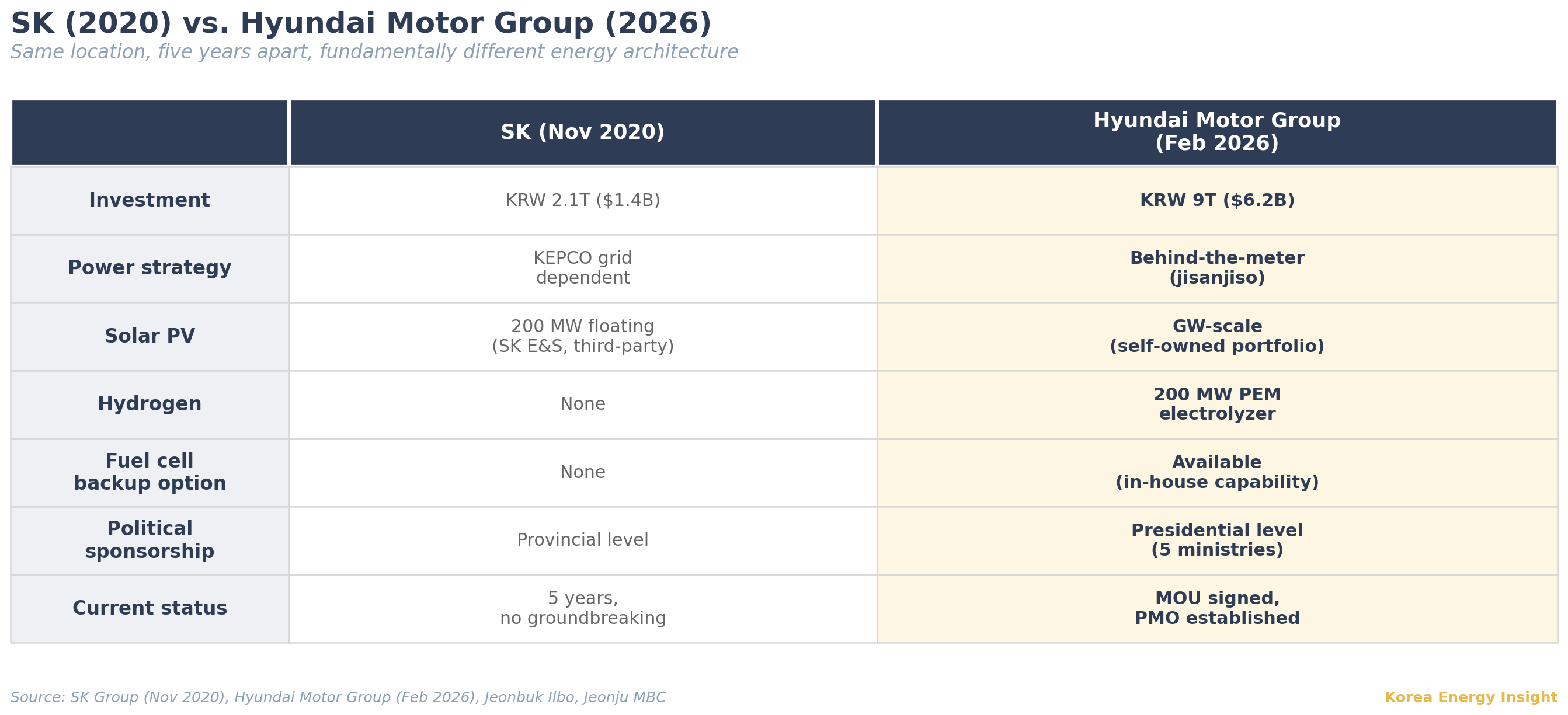

The 지산지소 concept is not new to Saemangeum. In November 2020, SK announced a $1.4 billion (KRW 2.1 trillion) data center in the same industrial complex, paired with 200MW of floating solar PV from SK E&S. The logic was identical: on-site renewable generation, RE100 compliance, hydrogen economy showcase. Chairman Chey Tae-won attended the signing.

Five years later, SK’s data center has not broken ground. The project required a 345kV substation that was never built. KEPCO indicated as early as 2021 that grid reinforcement in Saemangeum would not be available until late 2026 at the earliest (전북일보, Aug 2021). The delays compounded through multiple bottlenecks — grid infrastructure planning, renewable energy project sequencing, inter-agency coordination between the Saemangeum Development Agency and Korea Hydro & Nuclear Power, and permitting timelines that kept slipping. By October 2024, the 23 firms that signed letters of intent for SK’s startup cluster had all withdrawn. Reporting indicated half of SK’s internal team favored abandoning the investment (전북일보, Oct 2024). As of August 2025, the project remained in limbo (Jeonju MBC, Aug 2025).

The lesson: Saemangeum has 409 km² of reclaimed land, strong solar irradiance, and port access. Renewable potential without grid infrastructure is stranded capacity.

What’s Different This Time

Three things separate Hyundai’s project from SK’s stalled predecessor.

Presidential-level political sponsorship. President Lee Jae-myung attended the signing. Five cabinet ministers co-signed. Prime Minister Kim Min-seok launched a dedicated Saemangeum-Jeonbuk TF on March 11. On March 24, Hyundai elevated its internal task force into a permanent Robot-Hydrogen Project Management Office under C-suite executive Seo Kang-hyun (머니투데이, Mar 24 2026). Both sides have placed senior leadership directly in the operational chain.

Operational track record on the ground. Hyundai Engineering has participated in the 99MW solar PV facility at Saemangeum Zone 1 since 2021 (Hyundai Motor Group). The group is not building from zero.

The 지산지소 structure changes the grid dependency equation. Hyundai’s model generates and consumes power within the same complex, and has the option to deploy its own fuel cells as a nighttime supply layer — a technological fallback SK never had. The 345kV bottleneck that stopped SK becomes less binding, though KEPCO grid connection will still matter for redundancy and seasonal backup.

Hyundai’s Hydrogen Supply Chain — From Vehicle to Power Plant

The 200MW electrolyzer is not a standalone bet. PEM fuel cells and PEM electrolyzers are electrochemical mirrors — one converts hydrogen to electricity, the other converts electricity to hydrogen — and they share core components: membrane electrode assemblies, bipolar plates, balance-of-plant. Hyundai is one of very few industrial groups with scale in fuel cells and an emerging domestic manufacturing base in PEM electrolysis.

The Saemangeum electrolyzer is the first phase of Hyundai’s plan to build 1GW of domestic electrolyzer capacity. The equipment comes from Hyundai’s own supply chain. In October 2025, the group broke ground on a $640 million (KRW 930 billion) hydrogen fuel cell and PEM electrolyzer factory in Ulsan, targeting 2027 completion — Korea’s first PEM electrolyzer production facility. The group reports over 90% localization of electrolyzer components, a cost position that pure-play electrolyzer startups cannot match. A 1MW containerized unit has been operating in Gwangju since February 2025, producing over 300 kg of hydrogen daily, and a 5MW plant-scale system is under development (EBN, Oct 30 2025).

PEM electrolysis is faster to ramp and more responsive to variable renewable input than alkaline alternatives, which matters for coupling with intermittent solar. If the Ulsan factory delivers on schedule, Hyundai will have domestically manufactured electrolyzers ready for Saemangeum’s 2029 timeline. If Ulsan slips, the entire hydrogen component of the Saemangeum project shifts right.

So What: Three Things This Changes

For global energy investors, the Saemangeum project matters beyond the headline number.

First, it tests whether Korea’s largest industrial conglomerates will bypass the national grid to secure their own power. Hyundai is not building a solar farm to sell electricity — it is building one to consume it. If the 지산지소 model works, it creates a template for every Korean manufacturer chasing RE100 compliance in a market where corporate renewable PPAs account for just 0.04% of total generation by volume (KEI Issue #4). Samsung, SK, and LG all face the same constraint. Hyundai is attempting to build around it.

Second, it reveals the scale mismatch between Korea’s hydrogen ambitions and its delivery infrastructure. Korea’s total hydrogen transport infrastructure currently handles roughly 44,000 tonnes per year (KEI Issue #8). Hyundai’s single Saemangeum electrolyzer at full capacity would produce approximately 29,000 tonnes annually. The country’s entire clean hydrogen supply chain — pipeline, storage, distribution — is not ready for the volumes that the government’s roadmap assumes. Saemangeum will be an early stress test.

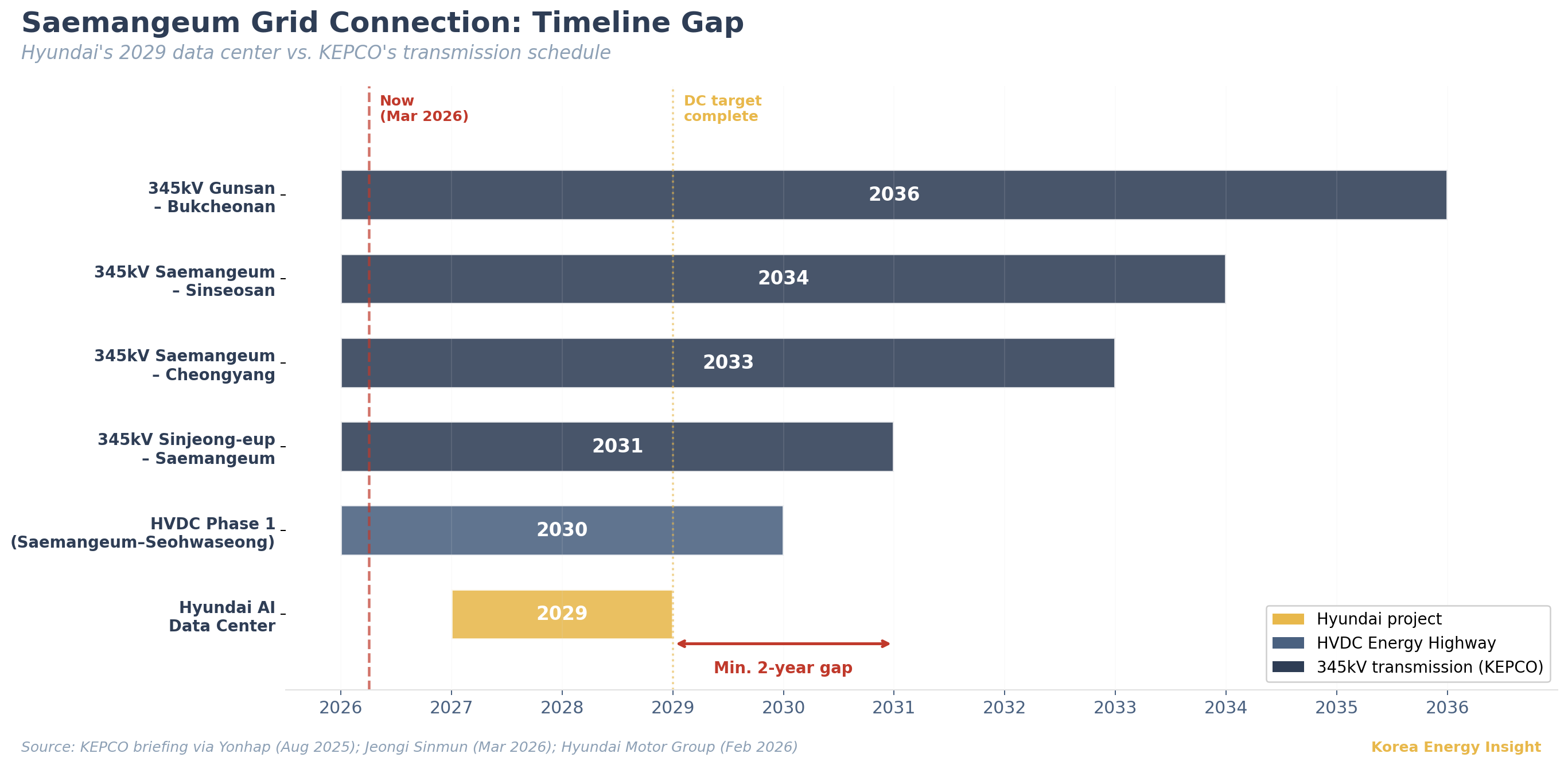

Third, it puts a concrete number on the political economy of Korean industrial policy. The 9 trillion won MOU was signed within Lee Jae-myung’s first year in office, with Jeonbuk, a core political constituency, as the beneficiary. Government support is obvious. The harder question is whether that support turns into steel, cable, permits, and financing on Hyundai’s clock rather than Seoul’s. The government’s planned West Coast Energy Highway is a multi-segment HVDC buildout phased to 2038. The first segment, roughly 220 km from Saemangeum to Seohwaseong, targets 2030 completion (전기신문, Mar 2026). Hyundai’s data center targets 2029. Those timelines need to converge.

The Signal

My base case. Solar and robot facilities proceed on the announced schedule (2027–2029 construction). The data center breaks ground in 2027 but faces a 12–18 month gap before stable power is secured through either the energy highway or a negotiated KEPCO grid connection. Investment disburses at roughly $1.2–1.4 billion per year, manageable within Hyundai’s cash flow but likely requiring policy finance from the Korea Development Bank and National Growth Fund. Full hydrogen production ramps after 2030.

What I’m watching. First, whether KEPCO signs a grid connection agreement for Saemangeum before year-end 2026. This is the step SK never achieved. Second, the West Coast Energy Highway construction timeline — specifically the Saemangeum converter station schedule. KEPCO began subsea cable route design in March 2026, with basic design completion targeted within the year and cable orders in early 2027 (전기신문, Mar 19 2026). Third, Hyundai’s Ulsan PEM electrolyzer factory (2027 target), which controls domestic equipment supply for the 200MW Saemangeum unit. Fourth, the AIDC Special Act, which passed its subcommittee in March 2026. If enacted, it could exempt non-metropolitan AI data centers from grid impact assessments and enable direct PPAs with renewable and LNG generators (전자신문, Mar 24 2026). That would remove a regulatory barrier that has blocked every previous Saemangeum data center attempt.

What would change my mind. The 345kV transmission projects linking Saemangeum to the national grid are currently in pre-construction — KEPCO’s public status page still lists the key lines in the “pre-approval” or “approved, pre-construction” buckets. Planned completion dates, as reported by Yonhap based on KEPCO briefings: Sinjeong-eup to Saemangeum, December 2031. Saemangeum to Cheongyang, December 2033. Saemangeum to Sinseosan, December 2034. Gunsan to Bukcheonan, December 2036 (연합뉴스, Aug 28 2025). Hyundai’s data center is supposed to be running by 2029. The 지산지소 model and the HVDC energy highway are the two paths around this gap. If SK’s stalled data center is formally terminated or relocated, it signals that neither path is working. In the other direction, acceleration of the HVDC converter station construction at Saemangeum or early passage of the AIDC Special Act would substantially de-risk execution.

If this analysis is useful for your team’s Korea strategy, consider forwarding it to a colleague.